Financial Sector (Collection of Data) (reporting standard) determination No. 8 of 2018

Reporting Standard ARS 118.0 Off-balance Sheet Business

Financial Sector (Collection of Data) Act 2001

I, Alison Bliss, delegate of APRA, under paragraph 13(1)(a) of the Financial Sector (Collection of Data) Act 2001 (the Act) and subsection 33(3) of the Acts Interpretation Act 1901:

(a) REVOKE Financial Sector (Collection of Data) (reporting standard) determination No. 3 of 2008, including Reporting Standard ARS 118.0 Off-balance Sheet Business made under that Determination; and

(b) DETERMINE Reporting Standard ARS 118.0 Off-balance Sheet Business, in the form set out in the Schedule, which applies to the financial sector entities to the extent provided in paragraph 3 of the reporting standard.

Under section 15 of the Act, I DECLARE that the reporting standard shall begin to apply to those financial sector entities, and the revoked reporting standard shall cease to apply, on 1 April 2018.

This instrument commences on 1 April 2018.

Dated: 21 March 2018

[Signed]

Alison Bliss

General Manager

Data Analytics Division

Interpretation

In this Determination:

APRA means the Australian Prudential Regulation Authority.

financial sector entity has the meaning given by section 5 of the Act.

Schedule

Reporting Standard ARS 118.0

Off-balance Sheet Business

Objective of this Reporting Standard

This Reporting Standard is made under section 13 of the Financial Sector (Collection of Data) Act 2001.

This Reporting Standard outlines the overall requirements for the provision of information to APRA relating to an authorised deposit-taking institution’s off-balance sheet exposures. It should be read in conjunction with:

- the versions of Reporting Form ARF 118.0 Off-balance Sheet Business designated for an authorised deposit-taking institution reporting at Level 1 and Level 2, and the associated instructions (all of which are attached and form part of this Reporting Standard); and

- Prudential Standard APS 112 Capital Adequacy: Standardised Approach to Credit Risk or Prudential Standard APS 113 Capital Adequacy: Internal Ratings-based Approach to Credit Risk, as appropriate.

- This Reporting Standard is made under section 13 of the Financial Sector (Collection of Data) Act 2001.

Purpose

2. Data collected in Reporting Form ARF 118.0 Off-balance sheet business (ARF 118.0) is used by APRA for the purpose of prudential supervision, including assessing compliance with Prudential Standard APS 112 Capital Adequacy: Standardised Approach to Credit Risk or Prudential Standard APS 113 Capital Adequacy: Internal Ratings-based Approach to Credit Risk, as appropriate. It may also be used by the Reserve Bank of Australia (RBA) and the Australian Bureau of Statistics (ABS).

Application and commencement

3. This Reporting Standard applies to an authorised deposit-taking institution (ADI) that is included in one of the classes of ADI to which this Reporting Standard applies, as set out in the table below.

Class of ADI | Applicable |

Bank – Advanced or Applicant Advanced | Yes |

Bank – Standardised | Yes |

Branch of a Foreign Bank | Yes |

Building Society | Yes |

Credit Union | Yes |

Provider of Purchased Payment Facilities | No |

Other ADI | Yes |

This Reporting Standard may also apply to the non-operating holding company (NOHC) of an ADI (refer to paragraph 6).

4. This Reporting Standard commences on 1 April 2018.

Information required

5. An ADI to which this Reporting Standard applies that is a bank – advanced or applicant advanced, bank – standardised, building society, credit union, or other ADI must provide APRA with the information required by the version of ARF 118.0 designated for an ADI at Level 1 for each reporting period. An ADI that is a branch of a foreign bank (i.e. is incorporated in an overseas jurisdiction) must provide APRA with the information required by the version of ARF 118.0 designated for an ADI at Level 1 for each reporting period in relation to the Australian branch only.

6. If an ADI to which this Reporting Standard applies that is a bank – advanced or applicant advanced, bank – standardised, building society, credit union, or other ADI, is part of a Level 2 group, the ADI must also provide APRA with the information required by the version of ARF 118.0 designated for an ADI at Level 2 for each reporting period, unless the ADI is a subsidiary of an authorised NOHC. If the ADI is a subsidiary of an authorised NOHC, the ADI’s immediate parent NOHC must provide APRA with the information required by that form for each reporting period. In doing so, the immediate parent NOHC must comply with this Reporting Standard (other than paragraphs 5 and 12) as if it were the relevant ADI.

Forms and method of submission

7. The information required by this Reporting Standard must be given to APRA in electronic format, using the ‘Direct to APRA’ application or by a method notified by APRA, in writing, prior to submission.

Note: the Direct to APRA application software (also known as D2A) may be obtained from APRA.

Reporting periods and due dates

8. Subject to paragraph 9, an ADI to which this Reporting Standard applies must provide the information required by this Reporting Standard in respect of each quarter based on the financial year (within the meaning of the Corporations Act 2001) of the ADI.

9. APRA may, by notice in writing, change the reporting periods, or specified reporting periods, for a particular ADI, to require it to provide the information required by this Reporting Standard more frequently, or less frequently, having regard to:

(a) the particular circumstances of the ADI;

(b) the extent to which the information is required for the purposes of the prudential supervision of the ADI; and

(c) the requirements of the Reserve Bank of Australia or the Australian Bureau of Statistics.

10. The information required by this Reporting Standard must be provided to APRA in accordance with the table below. The right hand column of the table sets out the number of business days after the end of the reporting period to which the information relates, within which information must be submitted to APRA by an ADI in each of the classes set out in the same row in the left hand column.

Class of ADI | Number of business days |

Bank – Advanced or Applicant Advanced | 30 |

Bank – Standardised | 20 |

Branch of a Foreign Bank | 20 |

Building Society | 15 |

Credit Union | 15 |

Provider of Purchased Payment Facilities | Not applicable |

Other ADI | 20 |

11. APRA may grant an ADI an extension of a due date in writing, in which case the new due date for the provision of the information will be the date on the notice of extension.

Quality control

12. All information provided by an ADI under this Reporting Standard (except for the information required under paragraph 6) must be the product of systems, processes and controls that have been reviewed and tested by the external auditor of the ADI as set out in Prudential Standards APS 310 Audit and Related Matters. Relevant standards and guidance statements issued by the Auditing and Assurance Standards Board provide information on the scope and nature of the review and testing required from external auditors. This review and testing must be done on an annual basis or more frequently if necessary to enable the external auditor to form an opinion on the accuracy and reliability of the information provided by an ADI under this Reporting Standard.

13. All information provided by an ADI under this Reporting Standard must be subject to processes and controls developed by the ADI for the internal review and authorisation of that information. These systems, processes and controls are to assure the completeness and reliability of the information provided.

Authorisation

14. When an officer of an ADI submits information under this Reporting Standard using the D2A application, or other method notified by APRA, it will be necessary for the officer to digitally sign the relevant information using a digital certificate acceptable to APRA.

Minor alterations to forms and instructions

15. APRA may make minor variations to:

(a) a form that is part of this Reporting Standard, and the instructions to such a form, to correct technical, programming or logical errors, inconsistencies or anomalies; or

(b) the instructions to a form, to clarify their application to the form

without changing any substantive requirement in the form or instructions.

16. If APRA makes such a variation it must notify in writing each ADI that is required to report under this Reporting Standard.

Interpretation

17. In this Reporting Standard:

AASB has the meaning in section 9 of the Corporations Act 2001.

ADI means an authorised deposit-taking institution within the meaning of the Banking Act 1959.

APRA means the Australian Prudential Regulation Authority established under the Australian Prudential Regulation Authority Act 1998.

Australian-owned bank means a locally incorporated ADI that assumes or uses the word ‘bank’ in relation to its banking business and is not a foreign subsidiary bank.

authorised NOHC has the meaning given in the Banking Act 1959.

bank – advanced or applicant advanced means an Australian-owned bank or a foreign subsidiary bank that has APRA’s approval or is seeking APRA’s approval to use an internal ratings-based approach to credit risk and/or an advanced measurement approach to operational risk for capital adequacy purposes.

bank – standardised means an Australian-owned bank or a foreign subsidiary bank that uses the standardised approaches to credit risk and/or an advanced measurement approach to operational risk for capital adequacy purposes in respect of the whole of its operations.

branch of a foreign bank means a ‘foreign ADI’ as defined in section 5 of the Banking Act 1959.

building society means a locally incorporated ADI that assumes or uses the expression ‘building society’ in relation to its banking business.

business days means ordinary business days, exclusive of Saturdays, Sundays and public holidays.

class of ADI means each of the following:

(i) bank – advanced or applicant advanced;

(ii) bank – standardised;

(iii) branch of a foreign bank;

(iv) building society;

(v) credit union;

(vi) other ADI; and

(vii) provider of purchased payment facilities.

credit union means a locally incorporated ADI that assumes or uses the expression ‘credit union’ in relation to its banking business and, for the purposes of this Reporting Standard, includes Cairns Penny Savings and Loans Limited.

foreign ADI has the meaning in section 5 of the Banking Act 1959.

foreign subsidiary bank means a locally incorporated ADI in which a bank that is not locally incorporated has a stake of more than 15%.

immediate parent NOHC means an authorised NOHC, or a subsidiary of an authorised NOHC, that is an immediate parent NOHC within the meaning of paragraph 21(b) of Prudential Standard APS 110 Capital Adequacy (APS 110).

Level 1 has the meaning in APS 001.

Level 2 has the meaning in APS 001.

locally incorporated means incorporated in Australia or in a State or Territory of Australia, by or under a Commonwealth, State or Territory law.

other ADI means an ADI that is not an Australian-owned bank, a branch of a foreign bank, a building society, a credit union, a foreign subsidiary bank or a provider of purchased payment facilities, but for the purposes of this Reporting Standard does not include Cairns Penny Savings and Loans Limited.

provider of purchased payment facilities means an ADI that is subject to a condition on its authority under section 9 of the Banking Act 1959 confining the banking business that the ADI is authorised to carry on to providing purchased payment facilities.

reporting period means a period mentioned in paragraph 8 or, if applicable, paragraph 9.

stake means a stake determined under the Financial Sector Shareholdings Act 1998, as if the only associates that were taken into account under paragraph (b) of subclause 10(1) of the Schedule to that Act were those set out in paragraphs (h), (j) and (l) of subclause 4(1).

subsidiary has the meaning in section 9 of the Corporations Act 2001.

18. Unless the contrary intention appears, a reference to an Act, Prudential Standard, Reporting Standard, Australian Accounting or Auditing Standard is a reference to the instrument as in force from time to time.

19. APRA may make a determination in writing that an individual ADI of one class of ADI is to be treated, for the purposes of this Reporting Standard, as though it was an ADI of another class of ADI.

Reporting Form ARF 118.0

Off-balance Sheet Business

Instruction Guide

This instruction guide is designed to assist in the completion of Reporting Form ARF 118.0 - Off-balance Sheet Business (ARF 118.0). This form collects information on an authorised deposit-taking institution’s (ADI’s) off-balance sheet business relating to:

(a) derivative activities in the ADI’s trading and banking books; and

(b) liquidity support facilities contracted by the ADI to supplement its liquidity management and the value of any charges granted over the assets of the ADI to secure these contingent liabilities.

The information collected in this form is not used for the calculation of regulatory capital relating to an ADI’s off-balance sheet business.

In completing this form, ADIs should refer to Prudential Standard APS 112 Capital Adequacy: Standardised Approach to Credit Risk (APS 112) or Prudential Standard APS 113 Capital Adequacy: Internal Ratings-based Approach to Credit Risk (APS 113), as appropriate.

General directions and notes

Reporting entity

This form is to be completed at Level 1 and Level 2 by each ADI (subject to the paragraph following the table) that is included in one of the classes of ADI to which this form applies, as set out in the table below:

Class of ADI | Reporting required |

Bank – Advanced or Applicant Advanced | Yes |

Bank – Standardised | Yes |

Branch of a Foreign Bank | Yes |

Building Society | Yes |

Credit Union | Yes |

Provider of Purchased Payment Facilities | No |

Other ADI | Yes |

If an ADI is a subsidiary of an authorised non-operating holding company (NOHC), the report at Level 2 is to be provided by the ADI’s immediate parent NOHC.

Securitisation deconsolidation principle

Except as otherwise specified in these instructions, the following applies:

- Where an ADI (or a member of its Level 2 consolidated group) participates in a securitisation that meets APRA’s operational requirements for regulatory capital relief under Prudential Standard APS 120 Securitisation (APS 120):

(a) special purpose vehicles (SPVs) holding securitised assets may be treated as non-consolidated independent third parties for regulatory reporting purposes, irrespective of whether the SPVs (or their assets) are consolidated for accounting purposes;

(b) the assets, liabilities, revenues and expenses of the relevant SPVs may be excluded from the ADI’s reported amounts in APRA’s regulatory reporting returns; and

(c) the underlying exposures (i.e. the pool) under such a securitisation may be excluded from the calculation of the regulatory capital (refer to APS 120). However, the ADI must still hold regulatory capital for the securitisation exposures that it retains or acquires and such exposures are to be reported in Reporting Form ARF 120.1 Securitisation – Regulatory Capital. The risk-weighted assets (RWA) relating to such securitisation exposures must also be reported in Reporting Form ARF 110.0.1 Capital Adequacy (Level 1) and Reporting Form ARF 110.0.2 Capital Adequacy (Level 2).

2. Where an ADI (or a member of its Level 2 consolidated group) participates in a securitisation that does not meet APRA’s operational requirements for regulatory capital relief under APS 120, or the ADI undertakes a funding-only securitisation or synthetic securitisation such exposures are to be reported as on-balance sheet assets in APRA’s regulatory reporting returns. In addition, these exposures must also be reported as a part of the ADI’s total securitised assets within Reporting Form ARF 120.2 Securitisation – Supplementary Items.

Reporting period and timeframes for lodgement

The form is to be completed as at the last day of the stated reporting period (i.e. the relevant) quarter. The table below sets out the number of business days after the end of the relevant reporting period, within which each class of ADI must submit data to APRA.

Class of ADI | Number of business days |

Bank – Advanced or Applicant Advanced | 30 |

Bank – Standardised | 20 |

Branch of a Foreign Bank | 20 |

Building Society | 15 |

Credit Union | 15 |

Provider of Purchased Payment Facilities | Not applicable |

Other ADI | 20 |

An immediate parent NOHC must submit data to APRA within the same timeframe as its subsidiary ADI.

Unit of measurement

Class of ADI | Units |

Bank – Advanced or Applicant Advanced | Millions of dollars rounded to one decimal place |

Bank – Standardised | Millions of dollars rounded to one decimal place |

Branch of a Foreign Bank | Millions of dollars rounded to one decimal place |

Building Society | Whole dollars with no decimal place |

Credit Union | Whole dollars with no decimal place |

Provider of Purchased Payment Facilities | Not applicable |

Other ADI | Whole dollars with no decimal place |

An immediate parent NOHC must complete this form in AUD and in accordance with the same units as its subsidiary ADI.

Amounts denominated in foreign currency are to be converted to AUD in accordance with AASB 121 The Effects of Changes in Foreign Exchange Rates.

Definitions

In this instruction guide and its corresponding reporting form (ARF 118.0), the following expressions have the defined meanings as set out below:

Principal amount

The principal amount refers to the face value or gross amount of a given off-balance sheet transaction and not the fair value. Absolute values should be reported. Netting, as defined in APS 112, should not be applied.

Fair value

The fair value is the amount for which an asset could be exchanged, or a liability settled, between knowledgeable and willing parties in an arm’s-length transaction. The fair value should be able to be determined through observation of similar transactions, quoted market prices, independent valuations or if there is no readily observable market, through the ability to liquidate the investment or through assessing the net present value of future cash flows.

Record the aggregate fair (or market) value of the derivative exposure/position by summing the absolute fair value of each exposure, for each of the items listed.

For the purposes of valuing derivative exposures, for this form, fair value should represent an estimate of the amount, which could be expected to be received from the disposal of the derivative instrument in an orderly market, ignoring transaction costs. It is not necessarily related to the nominal value of the derivative.

Market value is defined for accounting purposes as a subset of fair value, where fair value means the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm's-length transaction, and is determined as follows:

(i) the quoted market price in an active and liquid market (i.e. market value); or

(ii) when there is infrequent activity in a market, the market is not well established, small volumes are traded relative to the asset or liability to be valued, or a quoted market price is not available – an estimate of a price for the asset or liability in an active and liquid market.

Trading book

An ADI that wishes to operate a trading book must submit a trading book policy statement to APRA for approval that specifies those activities that belong in the trading book (refer to Prudential Standard APS 116 Capital Adequacy: Market Risk for details).

Banking book

The banking book covers all business not included in the trading book.

Specific instructions

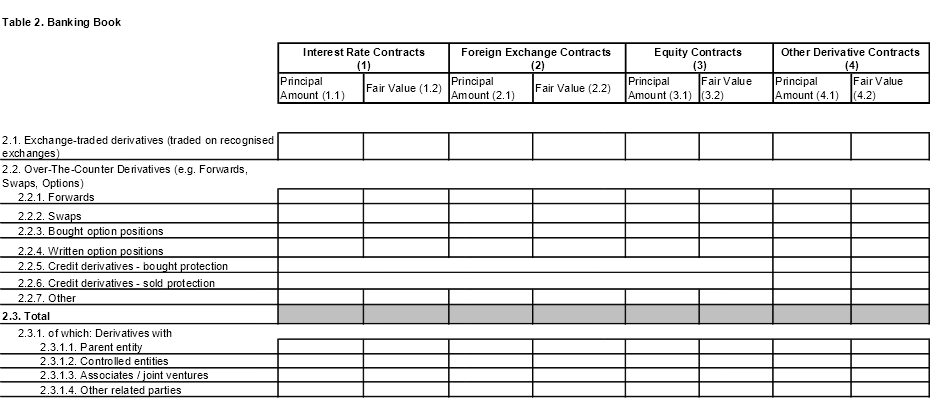

Section A: Statement of Derivative Activity

The statement of derivative activity is collected for information purposes. The information in this section is not directly used for the calculation of an ADI’s credit equivalent amounts for market-related off-balance sheet transactions as it does not allow for the contracts covered by eligible bilateral netting agreements (refer to APS 112 for the definition of eligible bilateral netting agreements). The regulatory capital relating to the ADI’s market-related off-balance sheet transactions is captured in Reporting Form ARF 112.2 Standardised Credit Risk – Off-balance Sheet Exposures or in the relevant ARF 113 Internal Ratings-based Approach to Credit Risk series of forms, depending on the approach an ADI is applying to the calculation of its credit risk regulatory capital.

An ADI should report all derivative activity within its trading and banking books, without taking into account netting, as defined in APS 112. ADIs may consult with APRA where they are unclear as to which category is appropriate for a particular derivative when reporting the principal amount and fair value of that derivative.

While not intended as an exhaustive list, derivative instruments may include the following:

Column 1: Interest rate contracts

Include:

- single currency interest rate swaps;

- basis swaps;

- forward rate agreements;

- interest rate futures;

- interest rate options purchased; and

- any other instruments of a similar nature.

Column 2: Foreign exchange contracts (including contracts involving gold)

Include:

- cross currency swaps (including cross currency interest rate swaps);

- forward foreign exchange contracts;

- currency futures;

- currency options purchased;

- hedge contracts; and

- any other instruments of a similar nature.

Outstanding spot transactions should be treated as forward foreign exchange contracts.

Column 3: Equity contracts

Include:

- swaps;

- forwards;

- futures;

- purchased options/warrants; and

- similar derivative contracts based on individual equities or equity indices.

Column 4: Other derivative contracts

Include:

- swaps;

- forwards;

- purchased options;

- similar derivative contracts based on precious metals such as gold, silver, platinum and palladium;

- energy contracts;

- agricultural contracts;

- base metals (such as aluminium, copper and zinc);

- other non-precious metal commodity contracts; and

- any contracts covering other items, that give rise to credit risk.

This category also includes all credit derivatives in the banking and trading book.

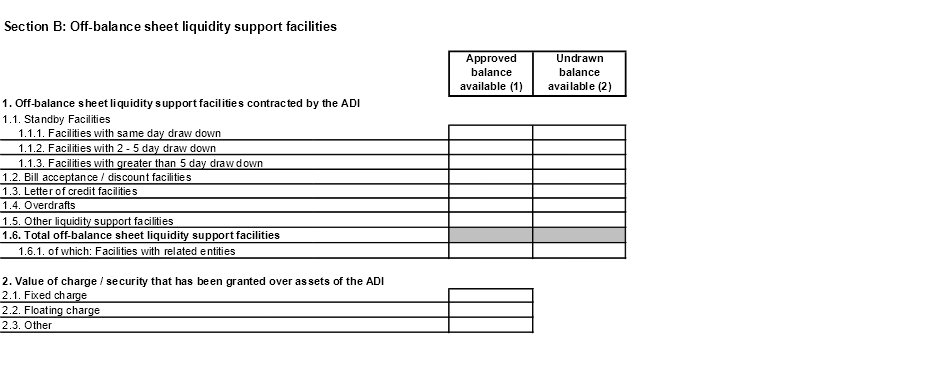

Section B: Off-balance sheet liquidity support facilities

The information collected in this section of the form is not included in the calculation of an ADI’s regulatory capital.

- Off-balance sheet liquidity support facilities contracted by the ADI

This section captures information on liquidity support facilities contracted by the ADI to supplement its liquidity management practices.

Column 1: Approved balance available

Include the total approved balance of the facility.

Column 2: Undrawn balance available

Include the balance of the facility that has not been used or drawn down by the ADI at the reporting date.

1.1 Standby facilities

These facilities are approved and committed to the ADI. Generally, an ADI is required to provide written notice to trigger draw down (access to the funds) on these facilities.

1.1.1 Facilities with same day draw down

Include those standby facilities that can be drawn down (funds accessed) on the same day that notice is given by the ADI of its intention to draw down on the standby facility.

1.1.2 Facilities with 2-5 day draw down

Include those standby facilities that can be drawn down (funds accessed) within two to five days after notice is given by the ADI of its intention to draw down on the standby facility (i.e. a two to five day waiting period).

1.1.3 Facilities with greater than 5 days draw down

Include those standby facilities that can be drawn down (funds accessed) five days after notice is given by the ADI of its intention to draw down on the standby facility (i.e. a five day waiting period).

1.2 Bill acceptance/discount facilities

These are another form of liquidity/funding. The funding is provided to the ADI by a facility that discounts bills (e.g. bank accepted bills). Principal and interest (discount) owing on the bill is repaid or ‘rolled over’ by the ADI on maturity of the bill.

1.3 Letter of credit facilities

This is an irrevocable and unconditional undertaking by an ADI to repay principal and interest of a loan in the event of default.

1.4 Overdrafts

These are accounts that may be overdrawn up to limits agreed to with an ADI.

1.5 Other liquidity support facilities

Include all other off-balance sheet liquidity support facilities contracted for the ADI’s use that are not included in the categories above.

1.6.1 Facilities with related entities

Include liquidity support facilities that are provided to the ADI by its related entities.

2. Value of charge/security that has been granted over assets of the ADI

2.1 Fixed charge

A fixed charge is a form of security provided to the lender relating to a specific asset or assets. A fixed charge will generally limit the ability of the ADI to deal with those assets (i.e. investment securities).

2.2 Floating charge

This is a charge where the creditor’s charge or claim is not lodged over a particular asset, but is fixed on a specific asset (or assets) only if the default occurs. This process is called crystallisation of the charge. A floating charge leaves the debtor free to buy, sell and vary the assets until such time as the charge is crystallised.