- This Reporting Standard is made under section 13 of the Financial Sector (Collection of Data) Act 2001.

2. Information collected by this Reporting Standard is used by APRA for the purposes of assisting APRA to perform its functions including prudential supervision, enabling APRA to publish information given by financial sector entities and assisting the Australian Securities and Investments Commission to perform its functions.

3. This Reporting Standard applies to all life companies authorised under the Life Insurance Act 1995 (Life Act) which write business as per section ‘A. Application’ in the Instructions.

4. This Reporting Standard commences on the day it is registered on the Federal Register of Legislation.

5. A life company to which this Reporting Standard applies must provide APRA with the information required by LRF 750.0 for each reporting period.

6. The information reported to APRA under this Reporting Standard is not required to be given to policy owners pursuant to section 124 of the Life Act. It does not constitute a reporting document for the purposes of section 124 of the Life Act.

7. The information required by this Reporting Standard must be given to APRA in electronic format using the ‘LRF 750.0 reporting form’, or by another method notified by APRA prior to submission.

Note: the ‘LRF 750.0 reporting form’ is obtained from APRA.

8. A Reporting Period is six months in duration.

9. A life company must provide the information required by this Reporting Standard relating to:

(a) the Reporting Period 1 July 2017 to 31 December 2017; and

(b) the Reporting Period 1 January 2018 to 30 June 2018;

by 28 December 2018.

10. A life company must provide the information required by this Reporting Standard relating to:

(a) the Reporting Period 1 July 2018 to 31 December 2018 three months after the end of the relevant Reporting Period; and

(b) the Reporting Period 1 January 2019 to 30 June 2019 two months after the end of the relevant Reporting Period.

11. A life company must provide the information required by this Reporting Standard relating to the Reporting Period 1 July 2019 to 31 December 2019, and each subsequent Reporting Period, within six weeks after the end of the relevant Reporting Period.

12. APRA may grant a life company an extension of a due date in paragraphs 9 through 11, in which case the new due date will be the date on the notice of extension.

13. If, having regard to the particular circumstances of a life company, APRA considers it necessary or desirable to obtain information more or less frequently than set out above, APRA may, by notice in writing, change the Reporting Periods, or specify Reporting Periods, for the particular life company.

14. All information provided by a life company under this Reporting Standard must be subject to systems, processes and controls developed by the life company for the internal review and authorisation of that information. It is the responsibility of the Board and senior management of the life company to ensure that an appropriate set of policies and procedures for the authorisation of data submitted to APRA is in place.

15. An officer, or agent, of a life company submitting information under this Reporting Standard must be authorised in writing to submit information under this Reporting Standard by either:

(a) the Principal Executive Officer of the life company; or

(b) the Chief Financial Officer of the life company.

16. APRA may make minor variations to:

(a) a form that is part of this Reporting Standard, and the instructions to such a form, to correct technical, programming or logical errors, inconsistencies or anomalies; or

(b) the instructions to a form, to clarify the application to the form,

without changing any substantive requirement in the form or instructions.

17. If APRA makes such a variation it must notify each life company that is required to report under this Reporting Standard.

18. Terms that are defined in Prudential Standard LPS 001 Definitions appear in bold the first time they are used in this Reporting Standard.

19. In this Reporting Standard:

Due date means the relevant due date under paragraphs 9 through 11 or, if applicable, the date on a notice of extension given under paragraph 12;

Chief Financial Officer means the chief financial officer of the life company, by whatever name called;

Principal Executive Officer means the principal executive officer of the life company, by whatever name called; and whether or not they are a member of the governing board of the entity; and

Reporting Period means a Reporting Period under paragraph 8 or, if applicable, the date on a notice given under paragraph 13.

20. Unless a contrary intention appears, a reference to an Act, Prudential Standard or Reporting Standard is a reference to the instrument as in force or existing from time to time.

21. Where this Reporting Standard provides for APRA to exercise a power or discretion, it is to be exercised in writing.

The reporting form consists of 8 core data entry tables. These tables are duplicated to cover different combinations of the relevant dimensions, including: Insurance Type, On-sale Status, Advice Type, Cover Type, Product Type, Dispute Type, claim measurement type (i.e. claim numbers, claim sum insured and claim amounts paid), and dispute measurement type (i.e. disputes by number, disputes by sum insured and disputes payment amounts). These dimensions are defined in Sections A through G of the instructions. The “Index” sheet of the reporting form lists all sheets, and identifies which require data input.

The reporting form is available on the APRA website, or upon request to APRA.

STATS: The core table for the 10 policy statistics sheets listed in paragraph 40. These tables cover combinations of the following dimensions: Insurance Type, On-sale Status, Advice Type, Product Type, Cover Type, and Sub-categories for specific Product or Cover Types. The reporting form includes 3 additional policy statistics sheets that provide totals or sub-totals.

CLAIMS: The core table for the 10 claims data sheets listed in paragraph 75. These tables cover combinations of the following dimensions: Insurance Type, On-sale Status, Advice Type, Cover Type, Product Type, claim measurement type, and Sub-categories for specific Product or Cover Types. The reporting form includes 3 additional claims data sheets that provide totals or sub-totals.

CLAIMSDURN: The core table for the 6 claims handling duration sheets listed in paragraph 75. These tables cover combinations of the following dimensions: Insurance Type, On-sale Status, Advice Type, Product Type, Cover Type, and Sub-categories for specific Product or Cover Types. The reporting form includes 3 additional claims handling duration sheets that provide totals or sub-totals.

DISPUTES: The core table for the 6 disputes data sheets listed in paragraph 103. These tables cover combinations of the following dimensions: Insurance Type, On-sale Status, Advice Type, Product Type, Dispute Type, dispute measurement type, Cover Type, and Sub-categories for specific Product or Cover Types. The reporting form includes 3 additional disputes data sheets that provide totals or sub-totals.

DISPUTESDURN: The core table for the 6 disputes processing duration data sheets listed in paragraph 103. These tables cover combinations of the following dimensions: Insurance Type, On-sale Status, Advice Type, Cover Type, Product Type, Dispute Type, dispute measurement type, and Sub-categories for specific Product or Cover Types. The reporting form includes 3 additional disputes processing duration sheets that provide totals or sub-totals.

SUPPLEMENT_REOPENED: The core table for the SUPPLEMENT_REOPENED sheet. This table covers combinations of the following dimensions: Insurance Type, Cover Type and Product Type.

SUPPLEMENT_CCI: The core table for the SUPPLEMENT_CCI sheet. This table covers combinations of the following dimensions: Cover Type, Product Type, claim measurement type, dispute measurement type, CCI insurance by credit type and CCI insurance by benefit frequency.

SUPPLEMENT_DISPUTES: The core table for the SUPPLEMENT_DISPUTE sheet.

Sections A through G below provide the instructions for completing LRF 750.0.

- Any life companies authorised under the Life Act who directly write business for one or more of the following products are required to comply with LRS 750.0:

(a) Individual and Group Insurance products and benefits, whether classed as superannuation or ordinary business, that provide the Cover Types as defined in paragraph 16.

(b) Products providing Funeral Insurance, Consumer Credit Insurance (CCI) and Accident Insurance.

(c) Insurance benefits that are rider benefits on investment account and investment-linked contracts, provided that they offer the Cover Types defined in paragraph 16.

2. Information provided under LRF 750.0 should:

(a) only include Australian business;

(b) only include gross business written directly, i.e. excluding inwards and outwards reinsurance;

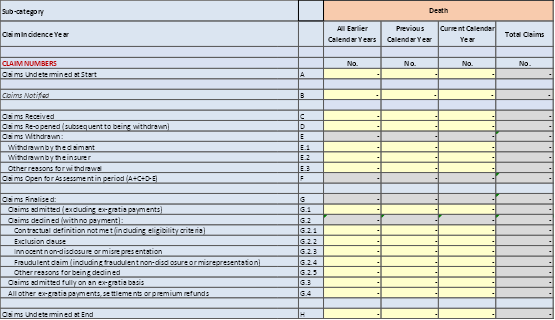

(c) be reported at a total statutory fund level;

(d) include detail on all in-force business of the Product and Cover Types included in the data collection;

(e) include detail at the start of the Reporting Period, at the end of the Reporting Period, as well as defined movements during the Reporting Period;

(f) include detail on all claims that were notified, received or re-opened during the defined Reporting Period, as well as claims that were undetermined at the start of the Reporting Period;

(g) in relation to disability income insurance (DII) business only include the initial reporting and assessment of claims, and exclude any detail about claims already in the course of payment at the start of the Reporting Period; and

(h) include all claims-related disputes that were lodged during the defined Reporting Period, as well as claim-related disputes that were undetermined at the start of the Reporting Period.

3. Claims and disputes should be classified based on their status at the end of the Reporting period. Any developments between the end of the Reporting period and the date of the data submission should not be reflected in the data collection.

4. Select the relevant insurer on the cover sheet of the workbook provided by APRA.

5. As each input cell has data validation, it is not possible to enter links to other cells or workbooks.

6. Before final saving and submission of the workbooks, ensure that:

(a) Any workbook multi-user sharing that may have been utilised is turned off.

(b) The workbooks are not saved as read-only or as a compressed file, and are not password-protected.

(c) Any links to external files are removed.

(d) All balancing item cells are zero.

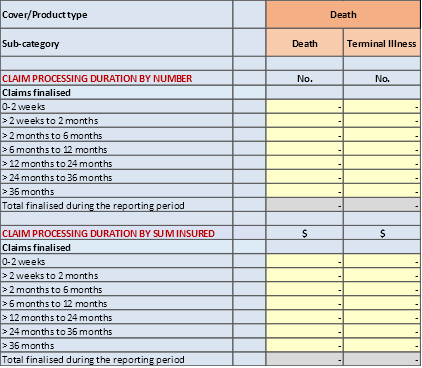

(e) All numbers are reported as whole numbers, including where they are linked for checks to work.

7. Rename the saved workbooks with a file name in the following format:

(a) Format: <Insurer short name>_<end of reporting period (yyyymmdd)>_<version number>.xlsx

(b) Example: ABC Life_20171231_v1.xlsx

8. The workbook provides various sub-totals, measures, checks or cross-checks to review the veracity of inputted data. Insurers should utilise them to check the accuracy of the data provided.

9. ‘Policy Contract’ refers to the life policy as defined by section 9 or 9A of the Life Act. In respect of Individual Insurance business, this contract is between the policyholder (who could also be the Life Insured) and the insurer. In respect of Group Insurance business, this contract is between the trustee (of a superannuation fund) or an employer and the insurer providing insurance for a group of eligible members.

10. ‘Life Insured’ refers to the individual life (or multiple lives in the event of joint life contracts) covered under a Policy Contract. In respect of Group Insurance contracts, Lives Insured are also referred to as members.

11. ‘Policyholder’ is the owner of the Policy Contract. It could be the same as the Life Insured.

12. ‘Class of Business’ refers to the type of business:

(a) Ordinary Business; and

(b) Superannuation Business.

The expressions ‘ordinary business’ and ‘superannuation business’ are defined in the Life Act.

13. ‘Insurance Type’ refers to the type of insurance:

(a) ‘Group Insurance’ business, where an employer or the trustee of a superannuation fund with at least five members purchased a group insurance policy to provide cover for the employees or superannuation fund members and the amount of cover on each life, excluding any voluntary additional cover, is determined by application of a formula. Lives insured are underwritten according to blanket rules that apply to the group and usually provide for automatic acceptance up to prescribed limits; and

(b) ‘Individual Insurance’ business, for insurance cover held outside superannuation or within a retail superannuation fund where each Policyholder selects the amount of death, TPD, trauma and income protection cover they require. Each Life Insured is individually underwritten. It also includes CCI, Accident and Funeral insurance.

It is expected that the distinction between Individual and Group Insurance should be consistent with how insurance business is classified and reported in APRA product groups (as defined in Reporting Standard LRS 001 Reporting Requirements). The Individual Lump Sum Risk (L4) and Individual Disability Income Insurance (L5) product categories should be classified as Individual Insurance business. The Group Lump Sum Risk (L6) and Group Disability Income Insurance (L7) product categories should be classified as Group Insurance business.

14. The following categories are defined for Insurance Type:

(a) Individual Insurance sold outside Superannuation Funds;

(b) Individual Insurance sold inside Superannuation Funds;

(c) Group Insurance sold outside Superannuation Funds; and

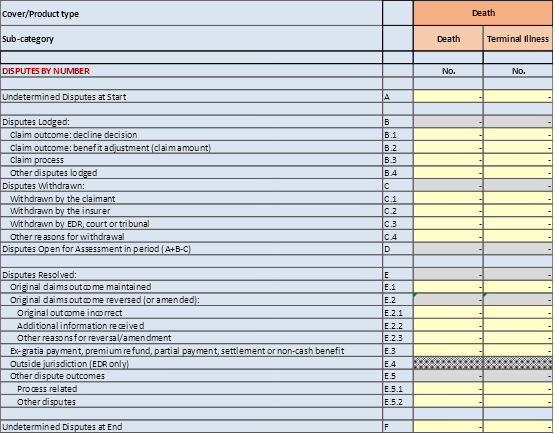

(d) Group Insurance sold inside Superannuation Funds.

15. The categories set out in paragraphs 14(a) to (d) should correspond to Class of Business and APRA product groups as follows:

Category | Class of business | APRA product group |

Individual Insurance outside Super | Australia – Ordinary Business | L4 and L5 |

Individual Insurance inside Super | Australia – Superannuation Business | L4 and L5 |

Group Insurance outside Super | Australia – Ordinary Business | L6 and L7 |

Group Insurance inside Super | Australia – Superannuation Business | L6 and L7 |

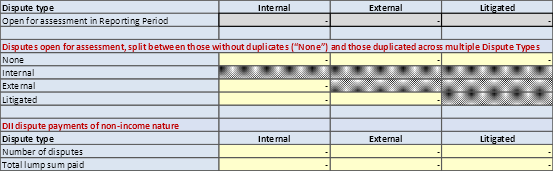

16. ‘Cover Type’ refers to the type of cover provided under a Policy Contract. The following Cover Types are defined:

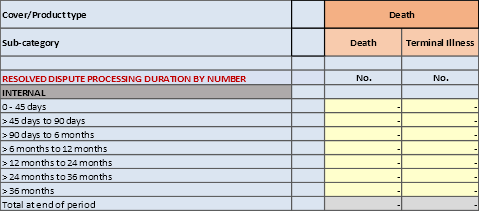

(a) ‘Death’ – cover that provides a lump sum payment in the event of the death of the insured life. This Cover Type can be with or without a Terminal Illness benefit. Where Terminal Illness is included, the death benefit can be paid before death occurs, provided certain predefined conditions are met. Death cover is relevant for both Individual and Group contracts.

(b) Total and Permanent Disability (‘TPD’) – cover that provides a lump sum payment in the event of the insured life being considered totally and permanently disabled in accordance with the policy definition. TPD can be either a death acceleration benefit or standalone. TPD cover is relevant for both Individual and Group contracts.

(c) Disability Income Insurance (‘DII’) – cover that provides for a regular payment for a maximum defined benefit period after a defined waiting period, in the event of the insured life being considered (totally or partially) disabled in accordance with the policy definitions. DII is relevant for both Individual and Group contracts and is commonly referred to as Income Protection (IP) and Group Salary Continuance (GSC) respectively. There are also older versions of this cover known as Total Temporary Disablement (TTD), which should also be included in this group.

(d) ‘Trauma’ – cover that provides a lump sum payment in the event of the occurrence of a predefined illness or traumatic event. Trauma can also be either an acceleration of the death/TPD benefit or standalone. Most trauma contracts also include partial payments for less severe conditions, with continuation of the remaining cover. Trauma cover exists mainly under Individual Insurance, but there are some older Group Insurance products where it is included. Trauma is sometimes referred to as Critical Illness insurance.

17. ‘Product Type’ refers to the type of product or rider benefit that provides any of the following Cover Types:

(a) Consumer Credit Insurance (CCI) – Insurance providing for a lump sum payment of the insured’s outstanding loan or credit card balance (in part or in full) or regular payments limited to the minimum repayments for a period, payable in the event of one or more predefined events occurring. CCI products included should be those written under a Life Insurance licence. This should include products that may be of a General Insurance nature, but where the insurer has been authorised by APRA to write it on a Life Insurance licence under section 12A of the Life Act.

Where an insurer also offers CCI products written on a General Insurance (GI) licence, either its own licence or that of another entity, the detail of these products (including statistics, claims and disputes) should be excluded.

(b) Funeral Insurance – Insurance for paying the expenses of, or incidental to, the funeral, burial or cremation of the person covered under the Policy Contract.

(c) Accident Insurance – Insurance providing for the payment of a lump sum in the event of accidental death or injury of the person covered under the Policy Contract.

18. ‘Sub-categories’ of Product and Cover Types are defined for selected products as follows:

(a) Death cover – distinction is made between the following main sub-categories:

(i) Death – where benefits are payable upon the death of the Life Insured.

(ii) Terminal illness – where death benefits can be accelerated upon the diagnosis of the Life Insured with a terminal illness.

(b) TPD cover – distinction is made between the following main sub-categories of disability definitions:

(i) Any occupation disability definition – where the Life Insured is considered unable to ever again work in any occupation for which they are reasonably suited by education, training or experience.

(ii) Own occupation disability definition – where the Life Insured is considered unable to ever again work in the occupation they were working in prior to the disability.

(iii) Other disability definitions.

(c) DII cover – distinction is made between the following main sub-categories:

(i) Personal – where the Life Insured is reimbursed for a proportion of their regular income, as defined in the underlying Policy Contract. Involuntary unemployment insurance issued under a life insurance licence should be included in this category.

(ii) Business Expense – where the Life Insured is reimbursed for certain regular business expense including rent, utilities, lease costs or depreciation, as defined in the underlying Policy Contract.

(d) CCI insurance by Cover Type – distinction is made between the following main sub-categories:

(i) Death – where a benefit is payable on the death or accidental death of the Life Insured.

(ii) Incapacity – where a benefit is payable when the Life Insured is deemed disabled or suffers an injury, a pre-defined illness or traumatic event, as defined in the underlying Policy Contract.

(iii) Involuntary redundancy – where a benefit is payable upon the Life Insured being made redundant at their place of work, in accordance with the provisions of the underlying Policy Contract.

(e) CCI insurance by credit type – distinction is made between the following main sub-categories:

(i) Loans – where the contract is to cover for the outstanding loan repayments, as defined in the underlying Policy Contract.

(ii) Credit Card – where the contract is to cover for the outstanding credit card repayments, as defined in the underlying Policy Contract.

(f) CCI insurance by benefit frequency – distinction is made between the following main sub-categories:

(i) Lump Sum – where a single amount is payable when the policy conditions are met.

(ii) Monthly Benefit – where a regular monthly benefit is payable when the policy conditions are met.

(g) Accident insurance cover – distinction is made between the following main sub-categories:

(i) Death – where a benefit is paid on the death of the Life Insured as a result of an accident, as defined in the underlying Policy Contract.

(ii) Injury – where a benefit is payable in the event of the Life Insured suffering an injury as a result of an accident, as defined in the underlying Policy Contract.

19. The reporting form does not distinguish between products and Cover Types offered on a stand-alone or an accelerated cover basis.

20. ‘Annual Premium’ refers to the annualised premium payable in respect of the Policy Contract. Annual Premiums reported should be gross of reinsurance and commissions, and before profit share rebates (Group Insurance). Reported premiums should also be inclusive of stamp duty, policy fees, loadings and discounts. For single-premium business, the annual premium should be estimated by spreading the single premium over the contract term. Policy fees should be appropriately apportioned between the relevant Cover/Product Types.

21. ‘Sum Insured’ refers to the contractual benefit payable when the insured event occurs. Insurers should report the full Sum Insured and not apply any reductions that may exist for severity-based Trauma and Accidental Injury benefits or for DII due to partial disability or a workers’ compensation offset. Where reductions to the Sum Insured are made consistent with the Policy Contract, this will be reflected in the Claim Amount Paid (defined in paragraph 51). Sum Insured should be reported gross of reinsurance. Distinction is made between the following types of Sums Insured:

(a) Lump Sum: this is a single amount payable when the policy conditions are met. Sums Insured in respect of Death, TPD and Trauma, as well as Funeral and Accident Insurance are normally of a lump sum nature. TPD benefits paid by instalments should be shown at their full face value. For Trauma contracts that include partial payments for less severe conditions, the Sum Insured is the full nominal Sum Insured and not the severity-based payment amount.

(b) Monthly Insured Benefit: for DII the Sum Insured is the regular monthly (or equivalent monthly) benefit that would be paid if the insured were disabled in accordance with the provisions of the Policy Contract.

(c) CCI benefits should be reported as follows:

(i) Lump sum that is fixed: The fixed benefit should be reported.

(ii) Lump sum equal to the outstanding loan or credit card balance: The latest known balance should be reported.

(iii) Lump sum equal to a portion of the outstanding loan or credit card balance: The calculated benefit based on the latest known balance should be reported.

(iv) Monthly benefit equal to a loan instalment: Monthly benefits should be reported on a capitalised basis, i.e. the monthly benefit multiplied by the number of months that the benefit is expected to be paid. Additional detail in respect of monthly benefits should be provided in the SUPPLEMENT_CCI sheet of the reporting form.

22. ‘New Business’ refers to a new Policy Contract, or a new Policy Benefit under an existing Policy Contract.

(a) New Business should include the following specific circumstances:

(i) Voluntary cover increases that resulted in new covers being created (typically subject to underwriting) or the exercise of embedded options (e.g. additional cover for the birth of a child);

(ii) New Policy Contracts issued that also had a claim during the Reporting Period;

(iii) Policies issued and subsequently lapsed during the cooling off period, all within the Reporting Period; and

(iv) New Policy Contracts created to replace cancelled policies. This only applies to instances that result in new covers.

(b) New Business should exclude the following specific circumstances:

(i) Automated premium and/or Sum Insured increases on existing covers, such as age-related premium increases for a stepped premium product or automatic CPI increases; and

(ii) Reinstatement or cover buybacks.

(c) Paragraphs 22(a) and (b) primarily relate to Individual Insurance contracts. In respect of Group Insurance contracts, it is the commencement of a new Policy Contract that should be reported under New Business, and not the impact of individuals joining the Group Insurance arrangement. Similarly, the effect of benefit changes at a member level should be excluded from New Business.

23. ‘Lapses’ refer to Policy Contracts (or underlying benefits) being discontinued.

(a) Lapses should include the following specific circumstances:

(i) Policies cancelled and replaced by a new Policy Contract;

(ii) Policies cancelled due to the non-payment of premiums;

(iii) Cancellation of the policy during the cooling-off period;

(iv) Partial lapses where there are decreases in Sum Insured or premium on existing covers should be included in the Lapses component of Annual Premium and Sum Insured, but not in Lives Insured and Policy Contracts; and

(v) Any contract that was discontinued during the Reporting Period, other than through a claim and not explicitly covered in the circumstances listed above.

(b) Lapses should exclude the following specific circumstances:

(i) Instances of the contract being discontinued as a result of the Life Insured dying, or another lump sum claim of the types covered by this collection;

(ii) Instances of the Policy Contract or benefit reaching the end of its contractual term, including where this is defined in terms of the age of the Life Insured; and

(iii) Policies later cancelled by the insurer from inception, e.g. in the event of misrepresentation or non-disclosure.

(c) Paragraphs 23(a) and (b) primarily relate to Individual Insurance contracts. In respect of Group Insurance contracts, it is the cancelation of the full contract that should be reported under Lapses and not the impact of individuals leaving the Group Insurance arrangement. Similarly, the effect of benefit changes at a member level should be excluded from Lapses.

24. ‘Disputes’ are defined to only include claims-related disputes. It includes disputes where a claim decision has been made, but the claims outcome is challenged or questioned, as well as disputes related to the claims process.

25. ‘Waiting period’ (usually in respect of TPD or DII) refers to a defined period after the Claim Event (defined in paragraph 42) that must expire before benefit payments will commence.

26. ‘On Sale Status’ refers to whether a product is still open for sale. Distinction is made between:

(a) Open for sale: Products that are open for sale at the time of the data submission.

(b) Closed for sale: Products that are no longer open for sale at the time of the data submission. These are also referred to as legacy products. New business as defined above is still possible.

On Sale Status is only recorded for Individual Insurance.

27. ‘Advice Type’ refers to the method by which the policy was sold and specifically the level of advice provided. This data dimension only applies to Individual Insurance. The following advice categories are defined:

(a) ‘Advised business’ refers to the sale of Individual Insurance, with the provision of personal advice, where personal advice has the same meaning as it does in section 766B(3) of the Corporations Act 2001 (Corporations Act). The reporting form assumes this does not apply to CCI, Funeral or Accident Insurance businesses.

(b) ‘Non-advised business’ refers to the sale of Individual Insurance, without the provision of personal advice. This includes where no advice or general advice is provided. General advice has the same meaning as it does in section 766B(4) of the Corporations Act.

28. ‘Ancillary Benefit’ refers to the payment made by an insurer in addition to the core benefit. Examples of Ancillary Benefits include rehabilitation benefits, family support benefits, bed confinement benefits and transportation benefits.

29. ‘Policy Benefit’ refers to a defined benefit provided under a Policy Contract. It is expected that a Policy Benefit would typically relate to a single Life Insured and Cover Type. Where multiple lives or Cover Types are covered under a single Policy Contract, such cover would be provided under separate Policy Benefits.

Where a Policy Contract has multiple Policy Benefits within the same Cover/Product Type, the policy and claims treatment will depend on the nature of these benefits. Distinction is made between the following categories:

(a) Policy Benefits that can be added together, with the same claim conditions. These Policy Benefits are typically the result of administrative processes, such as a separate benefit created for an annual automated cover increase.

(b) Policy Benefits that can be added together, with potentially different claim conditions. For example, a second death cover benefit under a Policy Contract has a pre-existing condition exclusion that does not apply to the original death cover benefit under the same Policy Contract.

(c) Policy Benefits that cannot be added together and provide for benefits under different claim conditions. The most common example is where a disability benefit is provided with different disability definitions, typically reflected in separate underlying benefits.

Where a Policy Contract has multiple Policy Benefits, refer to paragraph 37 for policy treatment instructions and paragraph 52 for claims treatment instructions.

30. In respect of Policy Data, the detail set out in paragraphs 31 to 39 should be provided.

31. The number of Policy Contracts, as defined in paragraph 9. This detail should be captured in the relevant Cover/Product Type category. Where a single Policy Contract contains multiple Cover Types, it should be counted in each of the Cover/Product Types where benefits are offered. In addition, the total number of unique Policy Contracts across all relevant cover and Product Types should be reported.

32. The number of Lives Insured, as defined in paragraph 10. This detail should be captured in the relevant Cover/Product Type category. Where a single life has multiple Cover Types, it should be counted in each of the Cover/Product Types where benefits are offered. In addition, the total number of unique lives insured across all relevant cover and Product Types should be reported.

33. The amount of Annual Premium, as defined in paragraph 20. This detail should be captured in the relevant Cover/Product Type category. Where a Policy Contract contains more than one Cover or Product Type, the amount of Annual Premium should be reflected separately for each Cover/Product Type. If the insurer does not determine or store separate amounts of premium, the total amount of Annual Premium should be appropriately apportioned between the relevant Cover/Product Types.

34. The amount of Sum Insured, as defined in paragraph 21. This detail should be captured in the relevant Cover/Product Type category. Where a Policy Contract contains more than one Cover/Product Type, the Sum Insured in respect of each Cover/Product Type should be recorded separately.

35. The items listed in paragraphs 31 to 34 should be provided for each of the following:

(a) The number/amount in force at the start of the Reporting Period.

(b) The number/amount that corresponds with New Business (as defined in paragraph 22) during the Reporting Period.

(c) The number/amount that corresponds with Lapses (as defined in paragraph 23) during the Reporting Period. The reporting form will treat entries for this item as an outflow, and it should not be captured with a negative sign.

(d) The number/amount of other movements that reconciles the detail at the start of the reporting period with the detail at the end of the Reporting Period. The reporting form will auto-complete this field, treating it as a balancing item to reconcile the various reported items. Insurers should, however, review the accuracy of this number. This item should include the impact of claims finalised during the Reporting Period.

(e) The number/amount in force at the end of the Reporting Period.

36. The items listed in paragraphs 31 to 35 should be provided for each relevant combination of the following data dimensions:

(a) Insurance Type;

(b) On Sale Status;

(c) Advice Type; and

(d) Cover/Product Type, including relevant sub-categories.

37. Where a single Policy Contract contains multiple Policy Benefits of the same Cover/Product Type, these should be dealt with as follows:

(a) Where multiple Policy Benefits all exist in the same combination of Insurance Type, On Sale Status and Advice Type, the different data items should be reported as follows, taking into account the different Policy Benefit categories defined in paragraph 29:

(i) Policy Contract: One Policy Contract should be recorded under the relevant Cover/Product Type, regardless of the Policy Benefit category.

(ii) Lives Insured: The number of lives covered under the Cover/Product Type should be recorded, regardless of the Policy Benefit category.

(iii) Annual Premium: The total amount of premium charged in respect of the Policy Benefits under the Cover/Product Type should be recorded, regardless of the Policy Benefit category.

(iv) Sum Insured: In respect of Policy Benefits that can be added together (i.e. paragraphs 29(a) and 29(b)), the Sums Insured under the different Policy Benefits should be added together. In respect of Policy Benefits that cannot be added together (i.e. paragraph 29(c)), the Sum Insured of a single Policy Benefit should be reported. In the event of different Sums Insured being payable under different Policy Benefits, the Policy Benefit with the highest Sum Insured should be reported.

(b) Where a Policy Contract contains a Policy Benefit (or Benefits) that exist across more than one combination of Insurance Type, On Sale Status or Advice Type, the different data items should be dealt with as follows:

(i) Policy Contract: One Policy Contract should be recorded in each relevant data dimension combination. The number of unique Policy Contracts should, however, only be recorded once, in the category regarded as the main or dominant data dimension combination.

(ii) Lives Insured: The number of lives covered under the Cover/Product Type should be recorded in each relevant data dimension combination. The number of unique Lives Insured should, however, only be recorded once, in the category regarded as the main or dominant data dimension combination.

(iii) Annual Premium: The total Annual Premium should be split across the different data dimensions that may be relevant to a specific Policy Contract. If the insurer does not determine or store separate amounts of premium, the total amount of Annual Premium should be apportioned between the relevant data dimensions.

(iv) Sum Insured: Detail should be recorded separately for each relevant data dimension.

One specific application of the methodology outlined above is where a single Policy Contract contains benefits both inside and outside Super, typically with TPD cover.

38. Ancillary Benefits that result in an enhancement to the underlying product or cover, as listed in paragraphs 16 to 18, should be included. The inclusion of Ancillary Benefits should, however, not result in multiple Policy Contracts.

39. Additional CCI policy data detail should be recorded in the SUPPLEMENT_CCI sheet of the reporting form. The detail provided should be consistent with what has been reported in the main collection, but providing a further split of data between credit card and loans, as well as between lump sum and monthly benefits. CCI monthly benefits should be reported on a capitalised basis, i.e. the monthly benefit multiplied by the number of months that the benefit is expected to be paid.

40. Paragraphs 31 to 39 correspond with the following sheets in the reporting form:

Sheet Name | Insurance Type | On Sale Status | Advice Type |

STATS_IndOS_Open_Adv | Individual outside Super | Open | Advised |

STATS_IndOS_Closed_Adv | Individual outside Super | Closed | Advised |

STATS_IndOS_Open_NonAdv | Individual outside Super | Open | Non-Advised |

STATS_IndOS_Closed_NonAdv | Individual outside Super | Closed | Non-Advised |

STATS_IndIS_Open_Adv | Individual inside Super | Open | Advised |

STATS_IndIS_Closed_Adv | Individual inside Super | Closed | Advised |

STATS_IndIS_Open_NonAdv | Individual inside Super | Open | Non-Advised |

STATS_IndIS_Closed_NonAdv | Individual inside Super | Closed | Non-Advised |

STATS_GrpOS | Group outside Super | N/A | N/A |

STATS_GrpIS | Group inside Super | N/A | N/A |

SUPPLEMENT_CCI | All CCI business | All | All |

41. In addition to the General Definitions, paragraphs 42 to 52 define a number of items specifically for Claims Data.

42. ‘Claim Event’ refers to the event that resulted in a Death, TPD, DII, Trauma, CCI, Funeral or Accident claim and the ‘Claim Event Date’ refers to the date on which the Claim Event occurred, or is deemed to have occurred. The Claim Event and Claim Event Date for certain Cover Types are defined as:

(a) Death Cover, CCI Death, Funeral or Accidental Death: The Claim Event is death and Claim Event Date the date of death.

(b) Terminal Illness: The Claim Event is the diagnosis of a Terminal Illness and the Claim Event Date the date of diagnosis.

(c) Trauma, CCI Incapacity or Accidental Injury: The Claim Event is one of the defined trauma, incapacity or accident events. The Claim Event Date is the date on which the event occurred or was diagnosed.

(d) TPD and DII: The Claim Event is what caused the condition of disability under either TPD or DII. The Claim Event Date is the date on which the medical diagnosis is made that underpins the disabled status of the claimant.

(e) CCI Redundancy: The Claim Event is the redundancy. The Claim Event Date is the date on which the Life Insured was made redundant while employed at their place of employment.

43. ‘Claim Incidence Year’ refers to the calendar year in which the Claim Event occurred. The data will be collected in respect of the following Claim Incidence Years:

(a) Current calendar year;

(b) Previous calendar year; and

(c) All earlier calendar years.

44. ‘Claim Notified’ refers to the initial contact made by the claimant, their authorised representative (including advisor), their superannuation fund trustee, or relevant other party informing the insurer of the claimant’s intention to lodge a claim. This could take the form of a physical submission (letter, email, etc.) or a telephone call. The ‘Claim Notification Date’ is the date on which the claim was first notified.

45. ‘Claim Received’ refers to the point in time where the first piece of information (not necessarily all information) is received by the insurer to allow it to commence the assessment of a claim. At this stage, the insurer has confirmed there is a policy in force that could potentially cover the indicated Claim Event and has recorded the existence of a claim. The ‘Claim Received Date’ is the date on which the insurer records a claim being received.[4]

46. ‘Claim Re-opened’ refers to instances where a claim has previously been Finalised or Withdrawn, but is re-opened by the insurer during the Reporting Period. It is expected that Re-opened claims would predominantly relate to claims that have been Finalised or Withdrawn during previous Reporting Periods. It is, however, possible (and acceptable) that re-opened claims could also relate to claims that have been Finalised or Withdrawn in the same Reporting Period as the claim being re-opened.

The treatment of re-opened claims distinguishes between claims that have been previously withdrawn versus claims that have been previously finalised:

(a) Only re-opened claims that were previously withdrawn should be included in the main collection, as reflected on the various claims sheets. They are recorded as Claim Re-opened (subsequent to being withdrawn) in the reporting form. Claim Re-opened (subsequent to being withdrawn) should be treated like any other received claim and be classified as Withdrawn, Finalised or Undetermined, as may be the case.

(b) Re-opened claims that were previously finalised should be excluded from the main collection. Instead, these claims together with additional related information should be reported in the SUPPLEMENT_REOPENED sheet of the reporting form. Where a claim is re-opened after a partial benefit has previously been admitted, it should be included in this category.

Where a claim is re-opened in the same Reporting Period as it was originally received, or if it was re-opened more than once during the same Reporting Period, it should be reported only once during the relevant Reporting Period, reflecting the latest outcome or status.

For DII, claims that have been terminated and are re-opened for a possible continuation of benefit payments should be excluded from re-opened claims. It is possible for a new DII claim to be submitted in respect of the same policy and Life Insured, e.g. where a significant period has passed since termination of a previous claim and/or where the cause of the claim is unrelated to that which applied before. Such claims should be considered as a new claim, to be classified as a Received claim and not a re-opened claim.

47. ‘Claim Withdrawn’ refers to the instance where a received claim is withdrawn and closed before being assessed and finalised. Note that a claim should be recorded in the ‘Withdrawn by the claimant’ category if the claimant returned to work prior to the expiry of a waiting period (where applicable).

48. ‘Claim Finalised’ refers to when the insurer has made a final decision on the claim (e.g. whether to admit or decline the claim) and communicated this decision to the claimant. The ‘Claim Finalised Date’ is the date on which the insurer’s claim decision is communicated to the claimant. This is not dependent on payment to the insured having been made. Communication by email, text message, facsimile or telephone is deemed to have occurred on the date it was sent. Communication by postal service is deemed to have occurred three business days after it was sent.

The Claim Finalised Date for DII refers to the date that the claim is admitted, declined or withdrawn and not to the claim termination date (when any regular payments cease because the insured has recovered from disability, the end of the benefit period was reached, or the claimant has died).

Where DII payments have commenced prior to a final claim decision being made (so-called goodwill payments), the claim should not be classified as Finalised. Such claims should only be classified as Finalised once a final claim decision has been made. If that claim decision is to decline the claim, the claim should be recorded as such, regardless of payments already made.

49. ‘Undetermined Claim’ refers to a Received Claim that has not been finalised or withdrawn at the end of the Reporting Period. Classification of a claim as Withdrawn, Finalised or Undetermined should be based on its status at the end of the Reporting Period. Any developments between the end of the Reporting Period and the date of the data submission should be excluded from the reporting form.

50. ‘Claim Sum Insured’ refers to the Sum Insured in respect of the Policy Contract and relevant Cover Type or benefit being claimed for. The full Sum Insured should be reported, ignoring any reduction, even where this is allowed for in the terms of the Policy Contract. The Claim Sum Insured should be gross of reinsurance.

51. ‘Claim Amount Paid’ refers to the actual amount paid gross of reinsurance. For DII, this is the regular monthly payment to the insured life, policyholder or nominated beneficiary. Where the Policy Contract allows for a reduction in the full Sum Insured (e.g. in the case of severity-based Trauma or Accidental Injury benefits, or for DII due to partial disability or a workers’ compensation offset), this field should reflect such a reduction. In the event of varying DII payments during the Reporting Period, the average monthly payment amount should be reported.

Any amounts paid from a superannuation account balance should not be included in the Claim Amount Paid. That is, only the insurance payout component should be included.

52. It is possible that the same Claim Event is considered and assessed for multiple Policy Benefits under the same Cover Type or Product. Referring to the three categories defined in paragraph 29, claims in respect of those categories should be dealt with as follows:

(a) Policy Benefits that can be added together, with the same claim conditions:

(i) A single claim outcome should be reported, with the Claim Sum Insured and Claim Amount Paid calculated as the sum of the underlying Policy Benefits.

(b) Policy Benefits that can be added together, with potentially different claim conditions:

(i) If the claim outcome is the same for all the underlying Policy Benefits, a single claim outcome should be recorded, with the Claim Sum Insured and Claim Amount Paid calculated as the sum of the underlying Policy Benefits.

(ii) If the claim outcome is not the same for all underlying Policy Benefits, separate claim outcomes should be recorded. One claim record should be reported for each claim outcome, with the Claim Sum Insured and Claim Amount Paid calculated as the sum of the underlying Policy Benefits with the given claim outcome.

(c) Policy Benefits that cannot be added together and provide for benefits under different claim conditions:

A single claim outcome should be reported. Specifically:

(i) If the claim was admitted (including an ex-gratia admittance), or any other form of payment made, a single record should be reported in the appropriate category, reflecting the relevant Claim Sum Insured and Claim Amount Paid. The fact that there may have been a decline decision in respect of another Policy Benefit should not be reported.

(ii) If the claim was declined (with no payment) under all Policy Benefits, a single decline decision should be reported. The Sum Insured should be appropriately apportioned among different Policy Benefits.

The most common example is the structuring of TPD benefits with different definitions for disability. The Life Insured could then be assessed under multiple disability definitions, arising from the same claim submission.

53. In respect of Claims Data, the detail set out in paragraphs 54 to 63 should be provided.

54. The total number of claims that are undetermined at the start of the Reporting Period, split by Claim Incidence Year (labelled A on the various claims sheets in the reporting form). It is expected that numbers reported undetermined at the start of the Reporting Period would correspond to numbers reported undetermined at the end of the corresponding Claim Incidence Year in the previous Reporting Period. The classification of Claim Incidence Year should be based on the Claim Event Date of each individual claim received.

55. The total number of Claims Notified during the Reporting Period (labelled B). Where the Claim Event Date is known, the notified claim should be allocated to the relevant Claim Incidence Year. Where the Claim Event Date is not known, the notified claim should be allocated to the most recent Claim Incidence Year.

56. The total number of claims that have been received during the Reporting Period, split by Claim Incidence Year (labelled C).

57. The total number of claims that have been re-opened (subsequent to being withdrawn) during the Reporting Period, split by Claim Incidence Year (labelled D).

58. The total number of claims that have been withdrawn during the Reporting Period, split by Claim Incidence Year (labelled E). Claims withdrawn should be split between the following withdrawal reasons:

(a) ‘Withdrawn by the claimant’ (labelled E.1).

(b) ‘Withdrawn by the insurer’ (labelled E.2).

(c) ‘Other reasons for withdrawal’ (labelled E.3).

59. The total number of claims that have been finalised during the Reporting Period, split by Claim Incidence Year (labelled G). Claims finalised should be split between the following categories:

(a) ‘Claims admitted (excluding ex-gratia payments)’ (labelled G.1). This includes claims where the full benefit that the claimant was entitled to in terms of the Policy Contract was paid (or is payable). Where the Policy Contract makes provision for the payment of a portion of the full Sum Insured (e.g. severity-based Trauma or Accidental Injury benefits, or reductions in income benefits in lieu of other income received by the claimant), and such reductions were applied, the claim should be reflected in this category. No ex-gratia payments should be included here, even where the full benefit was paid.

(b) ‘Claims declined (with no payment)’ (labelled G.2). This includes outcomes where the claim is declined, with no benefit paid (or payable) to the claimant. Claims declined should be split between the categories defined in paragraph 61.

(c) ‘Claims admitted fully on an ex-gratia basis’ (labelled G.3). These are claims that technically do not meet the Policy Contract definition for a claim, but the insurer has decided to pay the claim in full.

(d) ‘All other ex-gratia payments, settlements or premium refunds’ (labelled G.4). These are claims where the full claim has not been admitted, but where the insurer has decided or agreed to make some form of payment, including ex-gratia payments, commercial settlements, and premium refunds or non-cash benefits. Note the treatment of different types of premium refunds as explained in paragraph 72.

60. Total number of claims that are undetermined at the end of the Reporting Period, split by Claim Incidence Year (labelled H).

61. Claims declined (with no payment) should be split between the following categories:

(a) ‘Contractual definition not met (including eligibility criteria)’ (labelled G.2.1). These are instances where the claimant does not meet the requirements of a qualifying claim, as defined in the Policy Contract. Also included here are eligibility criteria, such as being actively at work, a common requirement for Group Insurance contracts.

(b) ‘Exclusion clause’ (labelled G.2.2). These are instances where claims are declined on the grounds of a pre-existing condition exclusion, a limited cover clause, an exclusion imposed during initial underwriting, or any other policy exclusion in the Policy Contract. This includes the exclusion clauses that may be contained in the standard policy wording.

(c) ‘Innocent non-disclosure or misrepresentation’ (labelled G.2.3). Where the claim is declined for reasons of non-disclosure or misrepresentation as contemplated in section 29(1) of the Insurance Contracts Act 1984.

(d) ‘Fraudulent claim (including fraudulent non-disclosure or misrepresentation)’ (labelled G.2.4). Where a claim is declined on the grounds of fraud or fraudulent non-disclosure or misrepresentation as contemplated in sections 56, 29(2)-(3) of the Insurance Contracts Act 1984.

(e) ‘Other reasons for being declined’ (labelled G.2.5). Any other reasons for a claim being declined.

62. Claims incorrectly opened due to an administrative error should be excluded.

63. Ancillary Benefits that result in an enhancement to the underlying product or cover, as listed in paragraphs 16 to 18, should be included. The inclusion of Ancillary Benefits should, however, not result in multiple claims being recorded in respect of a single Claim Event. Where the payment frequency of an Ancillary Benefit differs from that of the main Policy Benefit (e.g. a lump sum Ancillary Benefit on a DII contract, or a recurring Ancillary Benefit on a lump sum contract), the Ancillary Benefit should be excluded.

64. The reporting form will automatically calculate ‘Claims Open for Assessment in period’ (labelled F) as the items reported in accordance with preceding paragraphs 54 plus 56 plus 57 minus 58. In addition, the form will perform a check to confirm reconciliation of the various items of entry. It is expected that F minus G minus H should equal zero.

65. The detail set out in paragraphs 54 to 63 should also be provided for the Sum Insured associated with the claims received (i.e. Claim Sum Insured). Note the following in respect of Trauma, Accident, DII and TPD claims:

(a) The full Sum Insured should be reported here, regardless of whether the insurer made a reduction in accordance with the provisions of the Policy Contract (such as severity-based Trauma or Accidental Injury benefits, DII benefit reductions due to partial disability or a workers’ compensation offset, or TPD benefits spread over multiple years).

(b) In respect of DII claims, the Sum Insured should reflect the monthly benefit under the contract.

66. In respect of claim outcomes where a benefit was paid, the detail set out in paragraphs 54 to 63 should also be provided for the Claim Amount Paid associated with the claims received. The reporting form should only be completed for the entries associated with a claim payment, namely G.1, G.3 and G.4. In addition, the following should be noted:

(a) Where a claim is admitted and, consistent with the provisions of the Policy Contract, the Claim Amount Paid is less than the full Sum Insured, the detail should be recorded in the ‘Claim admitted (excluding ex-gratia payments)’ category.

(b) For DII, the Claim Sum Insured is the regular monthly benefit that would be paid if the insured were totally disabled and no workers’ compensation or other offsets were applied. The Claim Amount Paid should reflect the actual regular monthly benefit payment. In instances where the actual monthly benefit varied over the course of the Reporting Period, an average monthly benefit should be reported.

67. The detail set out in paragraphs 54 to 66 should be provided for each combination of the following data dimensions:

(a) Insurance Type;

(b) On Sale Status;

(c) Advice Type; and

(d) Cover/Product Type, including sub-categories.

68. ‘Claims Processing Durations’ should be reported in respect of Claims Finalised during the Reporting Period, measured as the period between the Claim Received Date and the date the claim is finalised.

In respect of Cover Types that involve a waiting period, the Claims Processing Duration should be measured from the later of:

(a) The Claim Received Date; and

(b) The Claim Event Date plus Waiting Period.

There are a number of specific circumstances worth noting:

(c) Where a claim is finalised prior to the expiration of the Waiting Period, a Claims Processing Duration of zero should be recorded; and

(d) Where a claim is re-opened (subsequent to being withdrawn), the Claims Processing Duration should be measured from the original Claim Received Date and not the Claim Re-opened Date.

69. Claims Processing Durations should be reported by allocating the number of claims into the following ‘claims duration categories’:

(a) 0 to 2 weeks

(b) >2 weeks to 2 months

(c) >2 months to 6 months

(d) >6 months to 12 months

(e) >12 months to 24 months

(f) >24 months to 36 months

(g) >36 months

70. The Claims Processing Duration detail set out in paragraphs 68 and 69 should also be provided in respect of the Claim Sum Insured, as defined in paragraph 50.

71. The Claims Processing Duration detail set out in 68 to 70 should be provided for each combination of the following data dimensions:

(a) Insurance Type;

(b) Advice Type; and

(c) Cover/Product Type.

72. Premium refunds in paragraph 59 should be treated in the following ways:

(a) Where premiums collected after a Claim Event are refunded due to a purely administrative process, it should be excluded from this reporting form.

(b) Where a premium refund is made following the cancellation of a contract or Policy Benefit (for example, in the event of innocent non-disclosure), it should be reported in the ‘All other ex-gratia payments, settlements or premium refunds’ category.

(c) Where a premium refund is a contractual benefit or made on an ex-gratia basis (for example when death occurs as a result of sickness, but cover is for Accidental Death only), it should be reported in the ‘All other ex-gratia payments, settlements or premium refunds’ category.

Premium waiver benefits should be treated like any other Ancillary Benefit.

73. Claims that are re-opened after previously being finalised are excluded from the main collection. Where such claims are re-opened and subsequently finalised in the Reporting Period, the relevant detail should be included in the SUPPLEMENT_REOPENED sheet. Claims should be split across the following dimensions:

(a) Insurance Type;

(b) Cover Type;

(c) Original claims decision (in accordance with the categories set out in paragraph 59);

(d) Updated claims decision (in accordance with the categories set out in paragraph 59); and

(e) Reasons for re-opened claims that are subsequently finalised:

(i) ‘Additional information received’. These are instances where the claim has been re-opened after receiving additional information that could potentially overturn the original decision.

(ii) ‘Review requested / dispute lodged’. These are instances where the claim has been re-opened because the policyholder, their authorised representative or the superannuation fund trustee has requested a review of the original claims decision, or has lodged a dispute.

(iii) ‘Other’. Any claim re-open reasons not covered by one of the preceding categories, including administrative errors.

74. Additional CCI claims detail should be recorded in the SUPPLEMENT_CCI sheet of the reporting form. The detail provided should be consistent with what has been reported in the main collection, but providing a further split of data between credit card and loans, as well as between lump sum and monthly benefits.

75. Paragraphs 54 to 74 correspond with the following sheets in the reporting form:

Claims Data

Sheet Name | Insurance Type | On Sale Status | Advice Type |

CLAIMS_IndOS_Open_Adv | Individual outside Super | Open | Advised |

CLAIMS_IndOS_Closed_Adv | Individual outside Super | Closed | Advised |

CLAIMS_IndOS_Open_NonAdv | Individual outside Super | Open | Non-Advised |

CLAIMS_IndOS_Closed_NonAdv | Individual outside Super | Closed | Non-Advised |

CLAIMS_IndIS_Open_Adv | Individual inside Super | Open | Advised |

CLAIMS_IndIS_Closed_Adv | Individual inside Super | Closed | Advised |

CLAIMS_IndIS_Open_NonAdv | Individual inside Super | Open | Non-Advised |

CLAIMS_IndIS_Closed_NonAdv | Individual inside Super | Closed | Non-Advised |

CLAIMS_GrpOS | Group, outside Super | N/A | N/A |

CLAIMS_GrpIS | Group, inside Super | N/A | N/A |

Claims Duration Data

Sheet Name | Insurance Type | On Sale Status | Advice Type |

CLAIMSDURN_IndOS_Adv | Individual outside Super | All | Advised |

CLAIMSDURN_IndOS_NonAdv | Individual outside Super | All | Non-Advised |

CLAIMSDURN_IndIS_Adv | Individual inside Super | All | Advised |

CLAIMSDURN_IndIS_NonAdv | Individual inside Super | All | Non-Advised |

CLAIMSDURN_GrpOS | Group, outside Super | N/A | N/A |

CLAIMSDURN_GrpIS | Group, inside Super | N/A | N/A |

Supplementary Data

Sheet Name | Insurance Type | On Sale Status | Advice Type |

SUPPLEMENT_REOPENED | All | All | All |

SUPPLEMENT_CCI | All CCI business | All | All |

76. In addition to the General Definitions, paragraphs 77 to 86 define a number of additional items specifically for Disputes Data.

77. ‘Dispute Type’ distinguishes between Internal, External and Litigated Disputes.

78. ‘Internal Dispute’ refers to an instance where the claimant has registered their dissatisfaction with a claims decision or the claims process and requested the insurer to review its decision. This dispute category would also include disputes that may be raised by the trustees of a superannuation fund. Internal Dispute Resolution (‘IDR’) refers to the process followed by the insurer to deal with Internal Disputes that have been registered with the insurer.

79. ‘External Dispute’ refers to an instance where the claimant has registered their dissatisfaction regarding a claims decision or claims process with an external dispute resolution scheme or tribunal. This includes the Financial Ombudsman Service Limited (FOS) and the Superannuation Complaints Tribunal (SCT). External Dispute Resolution (‘EDR’) refers to the process followed by the insurer to deal with External Disputes that have been registered with the FOS, the SCT or similar schemes or tribunals.

80. ‘Litigated Dispute’ refers to an instance where a claimant has initiated legal proceedings against the insurer regarding a claim. This does not include instances where there have been solicitors involved, but no legal proceedings were initiated.

81. ‘Dispute Lodged’ refers to all claims-related disputes, regardless of whether it was raised with the insurer by the claimant (or their representative) or communicated to the insurer by a superannuation fund trustee, an external dispute resolution scheme, tribunal or court of law. Disputes should be classified and recorded as Lodged regardless of whether a decision has been reached and regardless of whether all information required to decide on the dispute has been received.

82. ‘Dispute Lodged Date’ is the earlier of the following dates:

(a) The date the claimant (or their representative) first raises a claims-related dispute with the insurer; and

(b) The date the insurer first receives information about a claims-related dispute from a superannuation fund trustee, external dispute resolution scheme, tribunal or court of law.

83. ‘Dispute Withdrawn’ refers to the instance where a Lodged dispute is withdrawn before being resolved.

84. ‘Dispute Resolved’ refers to the point where the insurer has communicated its final decision about how it will resolve the claims-related dispute to the claimant (or their authorised representative) or the point where FOS, the SCT, a similar scheme or tribunal, or a court of law has made a final determination/judgment that is binding on the insurer. Where a dispute relates to the claims process, it refers to the point where a response is communicated to the claimant or their authorised representative.

85. ‘Dispute Resolved Date’ is:

(a) For IDR, the date the insurer’s final decision or response on the dispute was communicated to the claimant (or their representative); and

(b) For EDR/Litigated disputes, the date the FOS, the SCT, a similar scheme or tribunal, or a court of law makes a final determination/judgment that is binding on the insurer.

Where relevant, this is not dependent on payment to the claimant having been made. Communication by email, text message, facsimile or telephone is deemed to have occurred on the date it was sent. Communication by the postal service is deemed to have occurred three business days after it was sent.

86. ‘Undetermined Dispute’ refers to a dispute that has been lodged, but has not been resolved or withdrawn at the end of the Reporting Period.

87. In respect of Disputes Data, the detail set out in paragraphs 88 to 97 should be provided.

88. The total number of disputes that are undetermined at the start of the Reporting Period (labelled A on the various disputes sheets in the reporting form).

89. The total number of claims-related disputes that have been lodged during the Reporting Period (labelled B). Lodged disputes should be split between the following Dispute Reasons:

(a) ‘Claim outcome: decline decision’ (labelled B.1). These are instances where the claim has been declined and the decline decision is challenged or disputed.

(b) ‘Claim outcome: benefit adjustment (claim amount)’ (labelled B.2). These are instances where a claim has been admitted but the benefit amount is challenged or disputed.

(c) ‘Claim process’ (labelled B.3). These are disputes that are not related to the claim outcome, but to any aspect related to the claim process: delays, requirements etc.

(d) ‘Other disputes lodged’ (labelled B.4). Any claims-related dispute not covered by one of the preceding categories.

Each dispute should only have one dispute reason. Where a dispute has multiple dispute reasons, only the dominant reason should be recorded.

90. The total number of disputes that have been withdrawn during the Reporting Period (labelled C). Disputes withdrawn should be split between the following withdrawal reasons:

(a) ‘Withdrawn by the claimant’ (labelled C.1).

(b) ‘Withdrawn by the insurer’ (labelled C.2).

(c) ‘Withdrawn by EDR, court or tribunal’ (labelled C.3).

(d) ‘Other reasons for withdrawal’ (labelled C.4).

91. The total number of disputes that have been resolved during the Reporting Period (labelled E). Resolved disputes should be split between the following Dispute Outcomes:

(a) ‘Original claims outcome maintained’ (labelled E.1). These are instances where the dispute did not result in any change to the original claim declinature decision, including any benefit that may have been paid.

(b) ‘Original claims outcome reversed (or amended)’ (labelled E.2). These are instances where the original claim declinature decision is reversed to become a ‘claim admitted’ decision, as well as instances in which the insurer has agreed to pay an additional amount equivalent to the amount sought by the claimant. The Dispute Outcomes reported in this category should be split into the sub-categories defined in paragraph 92.

(c) ‘Ex-gratia payment, premium refund, partial payment, settlement or non-cash benefit’ (labelled E.3). These are instances where the original declinature decision is not reversed (as defined in paragraph 91(b)), but an amount of compensation is paid (including any amount that is less than the amount sought by the claimant). This can take the form of an ex-gratia payment, a partial benefit payment, a commercial settlement, a premium refund, or a non-cash benefit.

(d) ‘Outside jurisdiction (EDR only)’ (labelled E.4). This category applies only to EDR disputes and refers to instances where the relevant dispute does not fall within the relevant dispute resolution scheme or tribunal’s jurisdiction in accordance with the scheme or tribunal’s rules.

(e) ‘Other dispute outcomes’ (labelled E.5):

(i) ‘Process related’ (labelled E.5.1). This category applies to all disputes related to the claims process.

(ii) ‘Other disputes’ (labelled E.5.2). Any resolved disputes not covered by the preceding categories should be reported in this category.

92. Resolved disputes where the original claims outcome was reversed (or amended) should be split into the following sub-categories:

(a) ‘Original outcome incorrect’ (labelled E.2.1). These are instances where, after review of all relevant detail and information provided, the insurer, an external dispute resolution scheme, tribunal or court of law decides that the original decision was incorrect.

(b) ‘Additional information received’ (labelled E.2.2). These are instances where the insurer, an external dispute resolution scheme, tribunal or court of law has received additional information and, based on the additional information, decided to reverse (or amend) the original claims decision.

(c) ‘Other reasons for reversal/amendment’ (labelled E.2.3). Any instances not covered by the preceding categories should be reported here.

93. Total number of disputes that are undetermined at the end of the Reporting Period (labelled F).

94. The reporting form will automatically calculate ‘Disputes Open for Assessment in period’ as paragraphs 88 plus 89 minus 90, labelled as D in the form. In addition, the form will perform a check to confirm reconciliation of the various items of entry. It is expected that D minus E minus F should equal zero.

95. Internal, External and Litigated Disputes relating to the same Claim Event (‘duplicate disputes’) should be reported as they exist on the administration systems of the insurer. Where the same dispute exists in multiple Dispute Types (e.g. both as an Internal and External dispute), all should be reported.

To enable a more complete understanding of disputes, additional information on the interaction between different dispute types is requested in the SUPPLEMENT_Disputes sheet of the reporting form. In the relevant table, report the number of all disputes open for assessment in the Reporting Period, split between those without duplicates (“None”) and those duplicated across multiple Dispute Types.

96. ‘Dispute Processing Durations’ should be reported in respect of Disputes Resolved during the Reporting Period, measured as the period between the Dispute Lodged Date and the Dispute Resolved Date.

97. ‘Dispute Processing Durations’ should be reported by allocating the number of disputes (by Policy Benefit count) into the following ‘disputes duration categories’:

(a) 0 to 45 days

(b) >45 days to 90 days

(c) >90 days to 6 months

(d) >6 months to 12 months

(e) >12 months to 24 months

(f) >24 months to 36 months

(g) >36 months

98. The detail set out in paragraphs 88 to 97 should also be provided for the Claim Sum Insured associated with the dispute.

99. The detail set out in paragraphs 88 to 95 should also be provided in respect of the actual payments made following the resolution of a dispute. Where the resolution of a dispute includes the payment of a benefit of any kind, be it the full contractual benefit or a partial payment of any kind, the amount of the payment (or equivalent value if the resolution resulted in a non-cash benefit) should be recorded under ‘Dispute Payment Amounts (Resolved)’ on the dispute sheets in the reporting form. Entries should only be reported in respect of outcome categories where a payment is possible, namely categories with reporting form labels E.2.1, E.2.2, E.2.3 and E.3.

In respect of DII claims, the main collection should only reflect benefits paid in the form of a monthly income (where these occur). Any payments related to the dispute that are not in the form of a monthly income benefit should be reported in the relevant table in the SUPPLEMENT_Disputes sheet of the reporting form.

To calculate the dispute payment amount, the Dispute Outcome ‘Original claims outcome reversed or amended’ includes any compensatory interest payments made under section 57 of the Insurance Contracts Act 1984 for unreasonably delayed claims.

100. The detail set out in paragraphs 88 to 99 should be provided for each combination of the following data dimensions:

(a) Insurance Type;

(b) Advice Type;

(c) Cover/Product Types; and

(d) Dispute Type.

101. Ancillary Benefit that results in an enhancement to the underlying product or cover, as listed in paragraphs 16 to 18, should be included.

102. Additional CCI disputes data detail should be recorded in the SUPPLEMENT_CCI sheet of the reporting form. The detail provided should be consistent with what has been reported in the main collection, but providing a further split of data between credit card and loans, as well as between lump sum and monthly benefits.

103. Paragraphs 88 to 102 correspond with the following sheets in the reporting form:

Disputes Data

Sheet Name | Insurance Type | On Sale Status | Advice Type |

DISPUTES_IndOS_Adv | Individual outside Super | All | Advised |

DISPUTES_IndOS_NonAdv | Individual outside Super | All | Non-Advised |

DISPUTES_IndIS_Adv | Individual inside Super | All | Advised |

DISPUTES_IndIS_NonAdv | Individual inside Super | All | Non-Advised |

DISPUTES_GrpOS | Group outside Super | N/A | N/A |

DISPUTES_GrpIS | Group inside Super | N/A | N/A |

Disputes Duration Data

Sheet Name | Insurance Type | On Sale Status | Advice Type | |

DISPUTESDURN_IndOS_Adv | Individual outside Super | All | Advised |

DISPUTESDURN_IndOS_NonAdv | Individual outside Super | All | Non-Advised |

DISPUTESDURN_IndIS_Adv | Individual inside Super | All | Advised |

DISPUTESDURN_IndIS_NonAdv | Individual inside Super | All | Non-Advised |

DISPUTESDURN_GrpOS | Group outside Super | N/A | N/A |

DISPUTESDURN_GrpIS | Group inside Super | N/A | N/A |

| | | | | |

Supplementary Data

Sheet Name | Insurance Type | On Sale Status | Advice Type |

SUPPLEMENT_CCI | All CCI benefits | All | All |

SUPPLEMENT_Disputes | All Disputes | All | All |