AASB Standard | AASB 2019-2 |

Amendments to Australian Accounting Standards – Implementation of AASB 1059

[AASB 16 and AASB 1059]

AASB Standard | AASB 2019-2 |

Amendments to Australian Accounting Standards – Implementation of AASB 1059

[AASB 16 and AASB 1059]

This Standard is available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: standard@aasb.gov.au

Website: www.aasb.gov.au

Phone: (03) 9617 7600

E-mail: standard@aasb.gov.au

COPYRIGHT

© Commonwealth of Australia 2019

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Requests and enquiries concerning reproduction and rights should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

ISSN 1036-4803

PREFACE

ACCOUNTING STANDARD

AASB 2019-2 AMENDMENTS TO AUSTRALIAN ACCOUNTING STANDARDS – IMPLEMENTATION OF AASB 1059

from paragraph

APPLICATION 2

AMENDMENTS TO AASB 16 5

AMENDMENTS TO AASB 1059 6

COMMENCEMENT OF THE LEGISLATIVE INSTRUMENT 7

BASIS FOR CONCLUSIONS

Australian Accounting Standard AASB 2019-2 Amendments to Australian Accounting Standards – Implementation of AASB 1059 is set out in paragraphs 1 – 7. All the paragraphs have equal authority.

This Standard makes amendments to AASB 16 Leases (February 2016) and AASB 1059 Service Concession Arrangements: Grantors (July 2017).

The AASB received feedback from some public sector stakeholders regarding issues applying the modified retrospective method stated in paragraph C4 of AASB 1059. Stakeholders also commented that, since mandatory application of AASB 1059 has been deferred by one year to annual periods beginning on or after 1 January 2020, it would be possible for some service concession arrangements to be captured by AASB 16 prior to the application of AASB 1059. Stakeholders expressed a view that applying AASB 16 for one year to service concession arrangements could be onerous.

The AASB considered stakeholders’ feedback and decided to amend AASB 16 and AASB 1059 to address these issues. The AASB also decided to make editorial amendments to the application guidance and implementation guidance accompanying AASB 1059.

Main requirements

This Standard makes amendments to AASB 16 and AASB 1059 to:

(a) amend the modified retrospective method set out in paragraph C4 of AASB 1059 as follows:

(i) specify the financial liability should be recognised at fair value at the date of initial application;

(ii) initially measure the Grant of a Right to the Operator (GORTO) liability representing the unearned portion of any revenue arising from the receipt of a service concession asset based on the current replacement cost of the service concession asset at the date of initial application adjusted to reflect the remaining concession period relative to the total period of the arrangement, rather than relative to the remaining economic life of the service concession asset;

(iii) measure a liability representing any third-party unearned revenue arising from the receipt of additional consideration from the operator for access to an existing asset of the grantor that has been reclassified as a service concession asset at the proceeds received, adjusted to reflect the remaining period of the service concession arrangement relative to the total period of the arrangement;

(b) modify AASB 16 to provide a practical expedient to grantors of service concession arrangements so that AASB 16 would not need to be applied to assets that would be recognised as service concession assets under AASB 1059; and

(c) include editorial amendments to the application guidance and implementation guidance accompanying AASB 1059.

Application date

This Standard applies to annual periods beginning on or after 1 January 2020, with earlier application permitted.

The Australian Accounting Standards Board makes Accounting Standard AASB 2019-2 Amendments to Australian Accounting Standards – Implementation of AASB 1059 under section 334 of the Corporations Act 2001.

| Kris Peach |

Dated 18 September 2019 | Chair – AASB |

Amendments to Australian Accounting Standards – Implementation of AASB 1059

1 This Standard amends AASB 16 Leases (February 2016) and AASB 1059 Service Concession Arrangements: Grantors (July 2017) to amend transitional relief relating to service concession arrangements and incorporate editorial amendments.

2 The amendments set out in this Standard apply to entities and financial statements in accordance with the application of AASB 16 and AASB 1059 set out in AASB 1057 Application of Australian Accounting Standards (as amended).

3 This Standard applies to annual periods beginning on or after 1 January 2020. Earlier application of this Standard is permitted.

4 This Standard uses underlining, striking out and other typographical material to identify some of the amendments to a Standard, in order to make the amendments more understandable. However, the amendments made by this Standard do not include that underlining, striking out or other typographical material. Amended paragraphs are shown with deleted text struck through and new text underlined. Ellipses (…) are used to help provide the context within which amendments are made and also to indicate text that is not amended.

5 Paragraph AusC4.1 is added as follows:

AusC4.1 Notwithstanding paragraphs C3 and C4, a public sector entity is not required to apply this Standard to assets that would be classified as service concession assets in accordance with AASB 1059 Service Concession Arrangements: Grantors. The entity shall continue to apply its existing accounting policy to these assets until AASB 1059 is applied.

6 Paragraphs B76 and C4, paragraphs IG10 and IG13 in the accompanying implementation guidance and paragraphs IE42–IE43 in the accompanying illustrative examples are amended as follows:

B76 The grantor determines whether guarantees provided by the grantor as part of a service concession arrangement meet the definition of a financial guarantee contract. If so, the grantor applies AASB 7, AASB 9 and AASB 132 in accounting for the financial guarantee. Where the financial guarantee is regarded as an insurance contract, the grantor can elect to apply AASB 4 Insurance Contracts or AASB 1023 General Insurance Contracts instead if it has previously used accounting applicable to insurance contracts for such guarantees.

…

C4 If a grantor elects to apply this Standard retrospectively in accordance with paragraph C3(b), the grantor shall:

(a) …

(b) measure a financial liability arising under a service concession arrangement in accordance with this Standard at fair value at the date of initial application;

(c) measure a liability representing the unearned portion of any revenue arising from the receipt of a service concession asset under the grant of a right to the operator model at the fair value (current replacement cost) of the related service concession asset at the date of initial application, adjusted to reflect the remaining period of the service concession arrangement relative to the remaining economic life of the asset total period of the arrangement, less any related financial liabilities measured in accordance with paragraph (b);

(d) measure a liability representing the unearned portion of any revenue arising from the receipt of additional consideration from the operator for access to an existing asset of the grantor that has been reclassified as a service concession asset at the proceeds received, adjusted to reflect the remaining period of the service concession arrangement relative to the total period of the arrangement;

(de) recognise any net adjustments to the amounts of assets and liabilities as an adjustment to the opening balance of accumulated surplus (deficiency) at the date of initial application; and

(ef) disclose that it has applied this transition approach and information relating to the measurement of the assets and liabilities in support of the disclosure objective in paragraph 28.

…

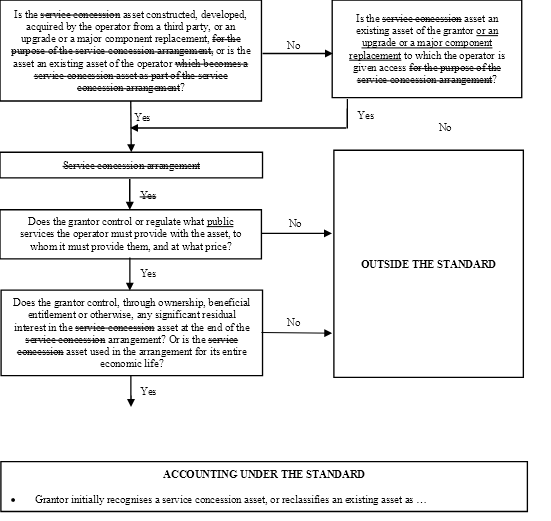

IG10 The diagram below summarises the accounting recognition and measurement requirements for assets (other than goodwill) and service concession arrangements in accordance with subject to AASB 1059.

![]()

![]()

![]()

Features | Construction contract with service outsourcing contract1 | Lease2 (grantor is lessor) | Service concession arrangement3 | Sale/Privatisation4 |

Determining whether arrangement is within the scope of AASB 1059 (paragraphs 2, IG2) | Conclusion (based on analysis below) – Outside the scope of AASB 1059 and grantor controls the asset. | Conclusion (based on analysis below) – Depending on terms of arrangement, can be outside or within the scope of AASB 1059. | Conclusion (based on analysis below) – Within the scope of AASB 1059 and grantor controls the asset. | Conclusion (based on analysis below) – Outside the scope of AASB 1059 and grantor does not control the asset. |

Operator provides public services related to the asset on behalf of the grantor and is responsible for at least some of the management of the asset the management of at least some of the public services (paragraph B10)? | Operator provides construction services, not public services. Operator provides management of asset acts as an agent in providing public services and related services as predetermined by the grantor | Operator involvement in the management of the asset public services and related services varies, depending on the lease terms (ie operator may have full involvement or be limited to facility management pre-determined by the grantor that is not a significant component of the public services provided by the asset). | Operator involved in management of service concession asset public services provided by the asset that is not predetermined by grantor (ie operator has discretion as to how the asset is managed the public services are provided and managed). | Operator does not provide public services on behalf of the grantor, despite any protective rights of the grantor. |

… | … | … | … | … |

Example 10: Transition – measuring the liability under the grant of a right to the operator model at the date of initial application

…

IE42 This example illustrates the approach set out in paragraph C4(c) to measuring a liability under the grant of a right to the operator model at the date of initial application. The liability related to the grant of a right to the operator is required to be measured at the fair value (current replacement cost) of the related service concession asset at the date of initial application, adjusted to reflect the remaining period of the service concession arrangement relative to the remaining economic life of the asset total period of the arrangement, less any related financial liabilities.

IE43 Assuming that the service concession arrangement in this example does not also give rise to a financial liability for the grantor, the information needed for measuring the liability is illustrated in the following table:

Table 10 Estimates at the date of initial application

Parameter | Amount or period |

Fair value (current replacement cost) of the | CU1,200 |

Remaining economic life of the asset Total period of the arrangement | 20 years |

Remaining service concession period | 10 years |

Apportionment for the liability re grant of rights | CU1,200 x 10/20 = CU600 |

7 For legal purposes, this legislative instrument commences on 31 December 2019.

Basis for Conclusions

This Basis for Conclusions accompanies, but is not part of, AASB 2019-2.

Introduction

BC1 This Basis for Conclusions summarises the Australian Accounting Standards Board’s considerations in reaching the conclusions in this Standard. It sets out the reasons why the Board developed the Standard, the approach taken to developing the Standard and the key decisions made. In making decisions, individual Board members gave greater weight to some factors than to others.

Background

Reasons for issuing this Standard

BC2 The Board received feedback from some public sector stakeholders regarding issues applying the modified retrospective method to measure the Grant of a Right to the Operator (GORTO) liability stated in paragraph C4(c) of AASB 1059 Service Concession Arrangements: Grantors. Stakeholders also commented that, since mandatory application of AASB 1059 has been deferred by one year to annual periods beginning on or after 1 January 2020, it would be possible for some service concession arrangements to be captured by AASB 16 Leases prior to the application of AASB 1059. Stakeholders expressed a view that applying AASB 16 for one year to service concession arrangements could be onerous. The Board considered stakeholders’ feedback and decided to propose amendments to AASB 16 and AASB 1059 to address these issues. The Board also decided to make editorial amendments to the implementation guidance accompanying AASB 1059.

Issue of Fatal-Flaw Review version of the Standard

BC3 In June 2019, the Board issued a Fatal-Flaw Review version of the Standard for public comment. Submissions were received from four stakeholders. All respondents were supportive of the Board changing the modified retrospective method to measure the GORTO liability stated in paragraph C4(c) of AASB 1059 and providing a practical expedient to grantors of service concession arrangements to not apply AASB 16 to assets that would be recognised as service concession assets under AASB 1059.

BC4 These respondents also provided feedback on additional issues in applying the modified retrospective method stated in paragraph C4 of AASB 1059 in relation to:

BC5 The Board considered stakeholders’ feedback and decided to amend AASB 16 and AASB 1059 to address these issues.

Modified retrospective method to measure the financial liability

BC6 The Board received comments from stakeholders that AASB 1059 was not clear whether the financial liability should be measured under the modified retrospective approach at the same amount as the fair value (current replacement cost) of the service concession asset received (similar to the initial recognition requirement); or in accordance with AASB 9 Financial Instruments (similar to the subsequent measurement requirement). The Board decided to amend paragraph C4(b) to clarify the measurement of the financial liability at fair value on the date of initial application.

BC7 The Board noted that paragraphs 5.1.1A and B5.1.2A of AASB 9 require entities to recognise a financial liability at fair value at initial recognition and the difference between the fair value at initial recognition and the transaction price. The Board considered that, for the purpose of the modified retrospective method, the grantor of a service concession arrangement would not be required to identify the difference between the fair value of the financial liability on the date of initial recognition and the historical transaction price, and so referred directly to measurement at fair value rather than in accordance with AASB 9.

Modified retrospective method to measure the GORTO liability resulting from receipt of a service concession asset

BC8 Under the modified retrospective method in AASB 1059 paragraph C4(c), a grantor measures a GORTO liability resulting from receipt of a service concession asset based on the “fair value (current replacement cost) of the related service concession asset received at the date of initial application, adjusted to reflect the remaining period of the service concession arrangement relative to the remaining economic life of the asset …” (emphasis added). Stakeholders indicated two issues in applying the calculation: (1) anomalous outcomes when a service concession asset has an indefinite economic life; and (2) a significantly lower GORTO liability compared to the asset if the remaining economic life of the service concession asset is significantly greater than the remaining concession period on transition to AASB 1059.

Extent of the issues and The AASB’s Not-for-Profit Entity Standard-Setting Framework

BC9 In discussions with the Treasury/Finance departments and/or Audit Offices in four jurisdictions, it was noted that some agencies in two States and some local councils in one State are experiencing the issues described in paragraph BC8. Representatives of these jurisdictions also commented that there would likely be a significant number of service concession assets with an indefinite useful life, such as earthworks. They also suggested that the GORTO liability calculated under paragraph C4(c) would be significantly smaller compared to the asset in some arrangements, particularly those in the early stages. Moreover, they believe the full retrospective method (the only alternative method) could not be applied as some agencies might not be able to obtain sufficient historical data to perform the full retrospective calculations.

BC10 The Board considered there is merit in changing the modified retrospective GORTO liability calculation method set out in paragraph C4(c). Even if entities could choose to apply the full retrospective model – if the necessary historical information was available – the Board was of the view that it would not be appropriate to completely remove the modified retrospective method at this stage of implementation of the Standard, as such an approach would require entities to apply the full retrospective method.

BC11 The Board also considered that changing the modified retrospective method is justified under The AASB’s Not-for-Profit Entity Standard-Setting Framework paragraph 28(a)[1], as the existing modified retrospective GORTO liability calculation would appear to result in reported performance or financial position not reflecting economic reality, particularly when the service concession asset has an indefinite useful life.

Options for addressing the issues

BC12 The Board considered four possible options for resolving the issues:

BC13 The Board considered the advantages and disadvantages of each option and decided to adopt Option 1 – change the modified retrospective GORTO liability calculation method so that it is initially measured based on the current replacement cost of the service concession asset at the date of initial application adjusted to reflect the remaining concession period relative to the total period of the arrangement, rather than relative to the remaining economic life of the service concession asset.

BC14 Option 1 would result in a larger GORTO liability compared to the current modified retrospective calculation method when the service concession asset has a remaining economic life longer than the total concession period. The Board considered that this larger GORTO liability calculated under Option 1 better reflects the grantor’s unearned revenue on transition date, under a short-cut method, compared to the current calculation method. This is because the grantor would be able to continue to benefit from the asset after the service concession arrangement has ended, and would then recognise income based on the grantor’s future use of the asset. The unearned revenue to be recognised under the service concession arrangement at the date of transition in the form of the GORTO liability therefore relates to the remaining service concession period and should be recognised as revenue over that period.

Modified retrospective method to measure the liability arising from the receipt of additional consideration from the operator for access to an existing asset of the grantor

BC15 Some stakeholders commented that AASB 1059 did not specify the recognition and measurement of additional consideration given by the operator to the grantor for access to an existing asset of the grantor that has been reclassified as a service concession asset, on transition to the Standard under the modified retrospective approach.

BC16 Consistent with paragraph 11 of AASB 1059, the Board considered that a liability should be recognised by the grantor where additional consideration is provided by the operator for access to an existing asset of the grantor that has been reclassified as a service concession asset. Consequently, a new paragraph C4(d) was added to specify the measurement requirement. For consistency, the Board decided that the same proportion used in measuring the GORTO liability resulting from receipt of a service concession asset – the remaining period of the service concession arrangement relative to the total period of the arrangement – should be applied to the amount of the proceeds received in measuring this liability under the modified retrospective approach.

Non-application of AASB 16 to assets that would be recognised as service concession assets

BC17 AASB 1059 was originally effective for annual reporting periods beginning on or after 1 January 2019, which was the same effective date as AASB 16. Subsequently, the mandatory effective date of AASB 1059 was deferred by one year to reporting periods beginning on or after 1 January 2020 by AASB 2018-5 Amendments to Australian Accounting Standards – Deferral of AASB 1059. Stakeholders noted that it would be possible for some service concession arrangements to be captured by AASB 16 prior to the application of AASB 1059. Stakeholders expressed a view that applying AASB 16 for one year could be onerous, requiring another change in accounting policy for service concession assets in the following year.

BC18 The Board considered whether changing the date of initial application of AASB 1059 – from the beginning of the earliest reporting period for which comparative information is presented in the financial statements to the beginning of the annual reporting period in which an entity first applies AASB 1059 – would avoid applying AASB 16 for one year to service concession arrangements. However, the Board noted that an entity would need to early adopt AASB 1059 in order to avoid applying AASB 16 to service concession arrangements. Changing the date of initial application as indicated would not change this need, but could make it more feasible for entities to early adopt AASB 1059.

BC19 The Board decided instead to modify AASB 16 to provide a practical expedient to public sector grantors of service concession arrangements so that AASB 16 would not need to be applied to assets that would be recognised as service concession assets under AASB 1059. Entities would be permitted to continue applying their existing accounting policy to these assets until AASB 1059 is applied. The Board had proposed in the Fatal-Flaw Review version limiting this practical expedient to assets recognised under AASB 117, but extended the scope to all assets that would be recognised under AASB 1059 following comments from respondents that some assets might be subject to AASB 16 without having been accounted for explicitly under AASB 117.

Editorial amendments

BC20 The Board decided to amend paragraph B76 of the application guidance to clarify that the grantor’s policy choice of continuing to apply insurance accounting is limited to contracts that meet the definition of a financial guarantee under AASB 9, if they had previously been accounted for as insurance contracts. The Board considered that compensation of revenue shortfalls in the context of AASB 1059 paragraph 16(b) would not meet the definition of a financial guarantee under AASB 9 for the grantor where the grantor is guaranteeing payments to the operator to cover lower usage of service concession assets than expected. Therefore, insurance accounting would not be appropriate in measuring the liability to the operator in the case of such revenue shortfalls. On the other hand, if the grantor guarantees to make payments to the operator in the event of users of the service concession assets defaulting on usage payments to the operator, then the grantor would assess whether it has a financial guarantee contract and would be eligible for continued insurance accounting, if previously applied.

BC21 A stakeholder expressed the view that the flowchart in paragraph IG10 of the implementation guidance in its current form could be misinterpreted – if either of the top two boxes is ‘Yes’, then the arrangement would automatically be a service concession arrangement without considering the two criteria in paragraph 2 of AASB 1059: whether the operator provides public services on behalf of the grantor, and whether the operator manages at least some of those services under its own discretion. The Board decided to amend the flowchart for the avoidance of doubt.

BC22 The Board also decided to amend the table in paragraph IG13 of the implementation guidance to be more consistent with paragraph B10, to indicate that the operator must be responsible for managing at least some of the public services provided through the asset, rather than being responsible for at least some of the management of the asset, for a transaction to be a service concession arrangement.

[1] Note that there are two paragraphs 28(a) in The AASB’s Not-for-Profit Entity Standard-Setting Framework. The reference here is to the second paragraph 28(a), which states “the prevalence and magnitude of NFP-specific transactions, circumstances and events results in NFP entities’ reported performance or financial position not reflecting economic reality (eg transfers of assets at significantly less than fair value primarily to enable a NFP entity to achieve its objectives, and for public sector entities, the provision of social benefits and related sustainability and sovereign power issues)”.