AASB Standard | AASB 2020-2 March 2020 |

Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities

Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities

AASB Standard | AASB 2020-2 March 2020 |

Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities

Obtaining a copy of this Standard

This Standard is available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: standard@aasb.gov.au

Website: www.aasb.gov.au

Phone: (03) 9617 7600

E-mail: standard@aasb.gov.au

COPYRIGHT

© Commonwealth of Australia 2020

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Requests and enquiries concerning reproduction and rights should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

ISSN 1036-4803

Contents

PREFACE

ACCOUNTING STANDARD

AASB 2020-2 AMENDMENTS TO AUSTRALIAN ACCOUNTING STANDARDS – REMOVAL OF SPECIAL PURPOSE FINANCIAL STATEMENTS FOR CERTAIN FOR-PROFIT PRIVATE SECTOR ENTITIES

from page

APPLICATION 5

AMENDMENTS TO THE CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING 6

AMENDMENTS TO THE FRAMEWORK FOR THE PREPARATION AND PRESENTATION

OF FINANCIAL STATEMENTS 6

AMENDMENTS TO STATEMENT OF ACCOUNTING CONCEPTS SAC 1 7

AMENDMENTS TO AASB 1 7

AMENDMENTS TO AASB 10 7

AMENDMENTS TO AASB 1048 8

AMENDMENTS TO AASB 1053 8

AMENDMENTS TO AASB 1057 12

COMMENCEMENT OF THE LEGISLATIVE INSTRUMENT 16

BASIS FOR CONCLUSIONS

Australian Accounting Standard AASB 2020-2 Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities is set out on pages 5 – 16. All the paragraphs have equal authority.

Preface

Standards amended by AASB 2020-2

This Standard makes amendments to the Australian Accounting Standards and other pronouncements listed on page 5 of the Standard.

These amendments explicitly extend the application of the Standards and the AASB Conceptual Framework for Financial Reporting (May 2019) to additional for-profit private sector entities. The amendments build upon the consequential amendments to pronouncements previously made in Accounting Standard AASB 2019-1 Amendments to Australian Accounting Standards – References to the Conceptual Framework (May 2019).

Main features of this Standard

Main requirements

This Standard makes amendments to the Standards (via AASB 1057 Application of Australian Accounting Standards) and the Conceptual Framework for Financial Reporting (Conceptual Framework) so that they apply explicitly to:

(a) for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards (with the previous limitation to entities with public accountability removed); and

(b) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

The Conceptual Framework is also amended to apply to other for-profit entities (including for-profit public sector entities) that elect to prepare general purpose financial statements and as a result apply the Conceptual Framework and the consequential amendments to other pronouncements set out in this Standard, as well as in AASB 2019-1.

The applicability of the Framework for the Preparation and Presentation of Financial Statements and Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity is amended so that they continue to apply to for-profit entities that do not need to apply the Conceptual Framework (eg for-profit public sector entities and those whose constituting document was created or amended before 1 July 2021), as well as to not-for-profit entities (subject to exceptions stated in the Standards).

Consequential amendments are made to various Standards, including amending the applicability of the ‘reporting entity’ definition in AASB 1057 so that it is not relevant to the entities to which this Standard is applicable (all of which would apply the Conceptual Framework). As a consequence, the ability of such an entity to prepare special purpose financial statements is removed and it will need to prepare general purpose financial statements that comply with Australian Accounting Standards (or accounting standards, under legislative requirements).

This Standard also adds an Appendix to AASB 1053 Application of Tiers of Australian Accounting Standards to provide relief from restating comparative information for entities that elect to early adopt the requirements in this Standard.

Application date

This Standard applies to annual reporting periods beginning on or after 1 July 2021, with earlier application permitted.

Accounting Standard AASB 2020-2

The Australian Accounting Standards Board makes Accounting Standard AASB 2020-2 Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities under section 334 of the Corporations Act 2001.

Kris Peach

Dated 6 March 2020 Chair – AASB

Accounting Standard AASB 2020-2

Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities

Objective

This Standard amends:

(a) the Conceptual Framework for Financial Reporting (May 2019);

(b) the Framework for the Preparation and Presentation of Financial Statements (July 2004);

(c) Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity (August 1990);

(d) AASB 1 First-time Adoption of Australian Accounting Standards (July 2015);

(e) AASB 10 Consolidated Financial Statements (July 2015);

(f) AASB 1048 Interpretation of Standards (December 2017);

(g) AASB 1053 Application of Tiers of Australian Accounting Standards (June 2010); and

(h) AASB 1057 Application of Australian Accounting Standards (July 2015);

to update the set of for-profit entities for which the reporting entity concept in SAC 1 is no longer relevant. Such entities are therefore not able to prepare special purpose financial statements when financial statements are required to comply with Australian Accounting Standards or when legislation requires financial statements to comply with accounting standards. This Standard also makes transition and consequential amendments to other Standards and pronouncements.

Application

The amendments set out in this Standard apply to entities and financial statements in accordance with the application of the other Standards set out in AASB 1057 Application of Australian Accounting Standards and the other pronouncements.

This Standard applies to annual reporting periods beginning on or after 1 July 2021.

This Standard may be applied to annual reporting periods beginning before 1 July 2021. When an entity applies this Standard to such an annual period, it shall disclose that fact.

This Standard uses underlining, striking out and other typographical material to identify some of the amendments to a pronouncement, in order to make the amendments more understandable. However, the amendments made by this Standard do not include that underlining, striking out or other typographical material. Amended paragraphs are shown with deleted text struck through and new text underlined. Ellipses (…) are used to help provide the context within which amendments are made and also to indicate text that is not amended.

Paragraphs Aus1.1 and Aus1.2 are amended.

Aus1.1 This Conceptual Framework applies to:

(a) for-profit private sector entities that have public accountability* and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(b) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021; and

(c) other for-profit entities (private sector or public sector) that elect to prepare general purpose financial statements apply the Conceptual Framework and the consequential amendments to other pronouncements set out in Accounting Standard AASB 2019‑1 Amendments to Australian Accounting Standards – References to the Conceptual Framework.

* The term ‘public accountability’ is defined in AASB 1053 Application of Tiers of Australian Accounting Standards.

Aus1.2 This Conceptual Framework applies to periods beginning on or after 1 January 2020 July 2021. Earlier application is permitted if at the same time an entity also applies the amendments made by AASB 2019-1 Amendments to Australian Accounting Standards – References to the Conceptual Framework and AASB 2020-2 Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities.

Paragraphs Aus1.2A and Aus1.2B are amended.

…

Aus1.2A This Framework does not apply in relation to reporting periods beginning on or after 1 January July 2021 to:

(a) for-profit private sector entities that have public accountability* and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(b) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021; and

(c) other for-profit entities (private sector or public sector) that elect to prepare general purpose financial statements apply the Conceptual Framework for Financial Reporting and the consequential amendments to other pronouncements set out in AASB 2019‑1 Amendments to Australian Accounting Standards – References to the Conceptual Framework;

except as otherwise required by Australian Accounting Standards.

* The term ‘public accountability’ is defined in AASB 1053 Application of Tiers of Australian Accounting Standards.

Aus1.2B If an entity identified in paragraph Aus1.2A elects to apply the Conceptual Framework for Financial Reporting to an annual reporting period prior to its mandatory application for the entity beginning before 1 January 2020, the entity shall not apply this Framework to that period, except as otherwise required by Australian Accounting Standards.

Paragraphs 2A and 2B are amended.

Application and Operative Date

…

2A This Statement does not apply in relation to reporting periods beginning on or after 1 January 2020 July 2021 to:

(a) for-profit private sector entities that have public accountability* and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(b) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021; and

(c) other for-profit entities (private sector or public sector) that elect to prepare general purpose financial statements apply the consequential amendments to other pronouncements set out in AASB 2019‑1 Amendments to Australian Accounting Standards – References to the Conceptual Framework.

* The term ‘public accountability’ is defined in AASB 1053 Application of Tiers of Australian Accounting Standards.

2B If an entity identified in paragraph 2A elects to apply the Conceptual Framework for Financial Reporting to an annual reporting period prior to its mandatory application for the entity beginning before 1 January 2020, the entity shall not apply this Statement to that period.

Paragraph Aus12.1 is added.

Aus12.1 Entities that elect to apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities to periods beginning before 1 July 2021 (ie early application) may also elect to apply the short-term exemptions from restating comparative information set out in AASB 1053 Application of Tiers of Australian Accounting Standards Appendix E, where applicable. For entities that apply that relief, references to the ‘date of transition to Australian Accounting Standards’ in this Standard shall mean the beginning of the first Australian-Accounting-Standards reporting period.

Paragraph Aus4.2 is amended.

…

Aus4.2 Notwithstanding paragraphs 4(a) and Aus4.1, the ultimate Australian parent shall present consolidated financial statements that consolidate its investments in subsidiaries in accordance with this Standard when the ultimate Australian parent is required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards, except if the ultimate Australian parent is required, in accordance with paragraph 31 of this Standard, to measure all of its subsidiaries at fair value through profit or loss.

Paragraphs 10 and AusCF10 are amended.

10 Each reference to the Conceptual Framework for Financial Reporting (or Conceptual Framework) in other Australian Accounting Standards (including Interpretations) is taken to be a reference to the relevant pronouncement listed in Table 3 below. Each row in Table 3 is to be treated as a separate provision of this Standard.

Table 3: Australian conceptual framework pronouncements

Issue Date | Title | Application Date (annual reporting periods) |

March 2020 [as amended to] | Conceptual Framework for Financial Reporting (or Conceptual Framework) Note – for-profit entities applying the Conceptual Framework are set out in paragraph Aus1.1 of the Conceptual Framework | (beginning) 1 July 2021 |

[MonthMay 2019] | Conceptual Framework for Financial Reporting (or Conceptual Framework) Note – this pronouncement is applicable only to for-profit private sector entities that have public accountability and are required by legislation to comply with Australian Accounting Standards and other for-profit entities that elect to apply this Framework | (beginning) 1 January 2020 |

AusCF10 Notwithstanding paragraph 10, in respect of AusCF entities, each reference to the Framework for the Preparation and Presentation of Financial Statements (or Framework) in other Australian Accounting Standards (including Interpretations) is taken to be a reference to the relevant pronouncement listed in Table 3 below. Each row in Table 3 is to be treated as a separate provision of this Standard.

Table 3: Australian conceptual framework pronouncements

Issue Date | Title | Application Date (annual reporting periods) |

March 2020 [as amended to] | Framework for the Preparation and Presentation of Financial Statements (or Framework) | (beginning) 1 July 2021 |

May 2019 [as amended to] | Framework for the Preparation and Presentation of Financial Statements (or Framework) | (beginning) 1 January 2020 |

June 2014 [as amended to] | Framework for the Preparation and Presentation of Financial Statements (or Framework) | (beginning) 1 July 2014 |

Paragraph 2 is deleted. Paragraphs 11, 18A and 18B are amended. Paragraph 18D is added.

2 [Deleted by the AASB] This Standard applies to1:

(a) each entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) general purpose financial statements of each reporting entity;

(c) financial statements that are, or are held out to be, general purpose financial statements;

(d) financial statements of General Government Sectors (GGSs) prepared in accordance with AASB 1049 Whole of Government and General Government Sector Financial Reporting; and

(e) for-profit private sector entities that have public accountability and are required by legislation to comply with Australian Accounting Standards.

1 This application paragraph does not amend the application paragraphs of other Standards that are restricted to reporting entities.

…

11 The following types of entities shall prepare general purpose financial statements that comply with Tier 1 reporting requirements:

(a) for-profit private sector entities that have public accountability and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(b) the Australian Government and State, Territory and Local Governments.

…

…

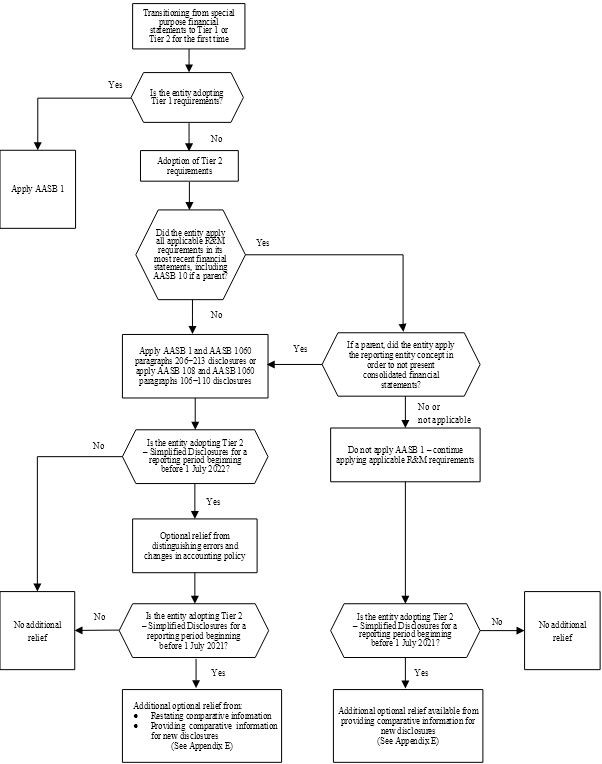

18A When applying Tier 2 reporting requirements for the first time, an entity that prepared its most recent previous financial statements in the form of special purpose financial statements:

(a) without applying, or only selectively applying, applicable recognition and measurement requirements of Australian Accounting Standards, including, if a parent entity, without presenting consolidated financial statements prepared in accordance with AASB 10 Consolidated Financial Statements (unless exempt), shall apply either:

(i) all the relevant requirements of AASB 1; or

(ii) Tier 2 reporting requirements directly using the requirements in AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors; and

(b) without presenting consolidated financial statements, on the basis that neither the parent nor the group was a reporting entity (as defined in AASB 1057), shall apply either:

(i) all the relevant requirements of AASB 1; or

(ii) Tier 2 reporting requirements directly using the requirements in AASB 108; and

(bc) applying all applicable recognition and measurement requirements of Australian Accounting Standards, including, if a parent entity, presenting consolidated financial statements prepared in accordance with AASB 10 (unless exempt), shall not apply AASB 1.

18B An entity applying paragraph 18A(bc) continues applying the applicable recognition and measurement requirements of Australian Accounting Standards, whether it had previously initially applied recognition and measurement requirements consistent with AASB 1 or a predecessor to AASB 108, whichever was applicable at the time.

…

18D Paragraph 18A(a) addresses where an entity has not applied, or only selectively applied, applicable recognition and measurement requirements, rather than whether the entity had made an explicit and unreserved statement of compliance with such requirements. As such, if an entity becomes aware it had claimed compliance with applicable recognition and measurement requirements of Australian Accounting Standards in error in its most recent previous special purpose financial statements, the entity applies paragraph 18A(a).

In Appendix C, Chart 1: First-time Adoption of Tier 1 or Tier 2 Reporting Requirements (paragraphs 18−18B) is replaced with the following.

Chart 1: First-time Adoption of Tier 1 or Tier 2 Reporting Requirements (paragraphs 18−18D)

![]()

Appendix E is added.

Appendix E

Short-term exemptions for entities applying Tier 2 – Simplified Disclosures for periods beginning before 1 July 2022

This appendix is an integral part of AASB 1053

E1 This appendix sets out optional short-term exemptions for for-profit private sector entities applying AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities to periods beginning before 1 July 2022, as follows:

(a) relief from distinguishing the correction of errors and changes in accounting policy, for periods beginning before 1 July 2022 (see paragraph E3);

(b) relief from providing comparative information not previously disclosed in the notes, for periods beginning before 1 July 2021 (see paragraph E4); and

(c) relief from restating comparative information, for periods beginning before 1 July 2021 (see paragraphs E5–E7).

E2 If an entity applies one or more of the exemptions set out in this appendix, it shall disclose that fact.

Relief from distinguishing the correction of errors and changes in accounting policy

E3 For periods beginning before 1 July 2022, notwithstanding AASB 1060 paragraph 211 (for entities applying AASB 1 First-time Adoption of Australian Accounting Standards to the period) and AASB 1060 paragraph 110 (for entities applying AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors instead of AASB 1), an entity applying paragraph 18A(a) or (b) need not distinguish the correction of errors and changes in accounting policies if the entity becomes aware of errors made in its most recent previous special purpose financial statements.

Relief from presenting comparative information not previously disclosed in the notes

E4 Notwithstanding AASB 1060 paragraph 20, entities that elect to apply AASB 1060 to periods beginning before 1 July 2021 (ie early application) need not present comparative information in the notes if the entity did not disclose the comparable information in its most recent previous financial statements.

Relief from restating comparative information for certain for-profit private sector entities

E5 Paragraphs E6–E7 apply to a for-profit private sector entity that elects to apply AASB 1060 to periods beginning before 1 July 2021 (ie early application) and also applies AASB 1 in preparing its first Australian-Accounting-Standards financial statements (Tier 2) for the period.

E6 Notwithstanding AASB 1 paragraph 7, comparative information need not be restated in the entity’s first Australian-Accounting-Standards financial statements (Tier 2). Under this approach, references to the ‘date of transition to Australian Accounting Standards’ in AASB 1 shall mean the beginning of the first Australian-Accounting-Standards reporting period. Consequently, consistent with AASB 1 paragraph 11, the entity shall recognise adjustments arising from any differences between the carrying amounts in its previous special purpose financial statements and its opening carrying amounts based on the retrospective application of Australian Accounting Standards directly in retained earnings (or, if appropriate, another category of equity) at the beginning of the first Australian-Accounting-Standards reporting period.

E7 An entity that elects to not restate comparative information in its first Australian-Accounting-Standards financial statements (Tier 2) in accordance with paragraph E6 need not provide the reconciliations required by AASB 1060 paragraphs 210(b) and (c). The entity shall:

(a) present two statements of financial position, two statements of profit or loss and other comprehensive income, two separate statements of profit or loss (if presented), two statements of cash flows and two statements of changes in equity and related notes, as follows:

(i) the statements and related notes as at the end of the first Australian-Accounting-Standards reporting period, compliant with Australian Accounting Standards; and

(ii) the statements and related notes presented in its most recent previous special purpose financial statements (not necessarily compliant with Australian Accounting Standards);

(b) disclose a reconciliation of its equity presented in its most recent previous special purpose financial statements to its equity determined in accordance with Australian Accounting Standards – Simplified Disclosures at the date of transition to Australian Accounting Standards – Simplified Disclosures;

(c) disclose a description of the main adjustments that would have been required to make the comparative statement of profit or loss and other comprehensive income and separate statement of profit or loss (if presented) compliant with Australian Accounting Standards. The entity need not quantify those adjustments; and

(d) prominently label the comparative information that is not compliant with Australian Accounting Standards as such.

Paragraphs 2, 5, 6–7, 9, 10, 12, 18, 20, 22–24 and 26 and the Appendix are amended. Paragraph 8 is deleted.

2 This Standard applies to:

(a) each entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) general purpose financial statements of each not-for-profit reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements;

(d) financial statements of General Government Sectors (GGSs) prepared in accordance with AASB 1049 Whole of Government and General Government Sector Financial Reporting; and

(e) for-profit private sector entities that have public accountability and are required by legislation* to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(f) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

* References in this Standard to ‘legislation’ mean legislation of a government in Australia.

…

5 Unless specified otherwise in paragraphs 5A–21, Australian Accounting Standards apply to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements; and

(d) for-profit private sector entities that have public accountability and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(e) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

…

6 AASB 8 Operating Segments and AASB 120 Accounting for Government Grants and Disclosure of Government Assistance applies to apply as set out in paragraph 5, provided the entity is a for-profit entity.

(a) each for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other for-profit reporting entity;

(c) financial statements of a for-profit entity that are, or are held out to be, general purpose financial statements; and

(d) for-profit private sector entities that have public accountability and are required by legislation to comply with Australian Accounting Standards.

6A AASB 17 Insurance Contracts applies as set out in paragraph 5,

(a) each entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other reporting entity; and

(c) financial statements that are, or are held out to be, general purpose financial statements;

except when the entity is:

(da) a superannuation entity applying AASB 1056; or

(eb) a not-for-profit public sector entity.

7 AASB 101 Presentation of Financial Statements, AASB 107 Statement of Cash Flows, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors, AASB 1048 Interpretation of Standards and AASB 1054 Australian Additional Disclosures apply to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) general purpose financial statements of each not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements; and

(d) for-profit private sector entities that have public accountability and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(e) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

8 [Deleted by the AASB] AASB 120 Accounting for Government Grants and Disclosure of Government Assistance applies to:

(a) each for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other for-profit reporting entity;

(c) financial statements of a for-profit entity that are, or are held out to be, general purpose financial statements; and

(d) for-profit private sector entities that have public accountability and are required by legislation to comply with Australian Accounting Standards.

9 AASB 133 Earnings per Share applies to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity or discloses earnings per share; and

(b) for-profit private sector entities that have public accountability and are required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act or disclose earnings per share.

10 AASB 134 Interim Financial Reporting applies to:

(a) each disclosing entity required to prepare half-year financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) interim financial reports that are general purpose financial statements of each other not-for-profit entity that is a reporting entity; and

(c) each entity that elects to prepare interim financial reports that are, or are held out to be, general purpose financial statements;

(d) interim financial reports of for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(e) interim financial reports of other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

…

12 AASB 1038 Life Insurance Contracts applies to:

(a) a life insurer; or

(b) the parent in a group that includes a life insurer;

when the entity is a not-for-profit public sector entity that:

(c) is a reporting entity and prepares general purpose financial statements; or

(d) prepares financial statements that are, or are held out to be, general purpose financial statements; or.

(f) is a for-profit private sector entity that has public accountability and is required by legislation to comply with Australian Accounting Standards.

…

18 AASB 1053 Application of Tiers of Australian Accounting Standards applies to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) general purpose financial statements of each not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements;

(d) financial statements of GGSs prepared in accordance with AASB 1049; and

(e) for-profit private sector entities that have public accountability and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(f) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

…

20 AASB 1056 Superannuation Entities applies to:

(a) general purpose financial statements of each not-for-profit superannuation entity that is a reporting entity;

(b) each superannuation entity that elects to prepare financial statements of a superannuation entity that are held out to be general purpose financial statements; and

(c) for-profit private sector superannuation entities that have public accountability and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(d) other for-profit private sector superannuation entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

…

22 Unless specified otherwise in paragraphs 23–26, Interpretations apply to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements; and

(d) for-profit private sector entities that have public accountability and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards, and

(e) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

23 Interpretation 110 Government Assistance – No Specific Relation to Operating Activities applies to: as set out in paragraph 22, provided the entity is a for-profit entity.

(a) each for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other for-profit reporting entity;

(c) financial statements of a for-profit entity that are, or are held out to be, general purpose financial statements; and

(d) for-profit private sector entities that have public accountability and are required by legislation to comply with Australian Accounting Standards.

24 Interpretation 1019 The Superannuation Contributions Surcharge applies to:

(a) each not-for-profit superannuation plan that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other not-for-profit superannuation plan that is a reporting entity;

(c) each superannuation plan that elects to prepare financial statements of a superannuation plan that are, or are held out to be, general purpose financial statements; and

(d) for-profit superannuation plans that have public accountability and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(e) other for-profit superannuation plans that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

…

26 Interpretation 1047 Professional Indemnity Claims Liabilities in Medical Defence Organisations applies to entities that are or include medical defence organisations as follows:

(a) general purpose financial statements of each not-for-profit public sector reporting entity; and

(b) each not-for-profit public sector entity that elects to prepare financial statements of each not-for-profit public sector entity that are, or are held out to be, general purpose financial statements; and.

(d) for-profit private sector entities that have public accountability and are required by legislation to comply with Australian Accounting Standards.

…

…

reporting entity

An entity in respect of which it is reasonable to expect the existence of users who rely on the entity’s general purpose financial statements for information that will be useful to them for making and evaluating decisions about the allocation of resources. A reporting entity can be a single entity or a group comprising a parent and all of its subsidiaries.

This reporting entity definition is not relevant to:

(a) for-profit private sector entities that have public accountability and are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(b) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021; and

(c) other for-profit entities (private sector or public sector) that elect to prepare general purpose financial statements and apply the Conceptual Framework for Financial Reporting and the consequential amendments to other pronouncements set out in AASB 2019‑1 Amendments to Australian Accounting Standards – References to the Conceptual Framework.

Commencement of the legislative instrument

For legal purposes, this legislative instrument commences on 30 June 2021.

This Basis for Conclusions accompanies, but is not part of, AASB 2020-2.

BC1 This Basis for Conclusions summarises the Australian Accounting Standards Board’s considerations in reaching the conclusions in AASB 2020-2. It sets out the reasons why the Board developed the Standard, the approach taken to developing the Standard, and the bases for key decisions made. In making decisions, individual Board members gave greater weight to some factors than to others.

BC2 For more than a decade the Board has been undertaking work aimed at addressing the problems that arise from entities being allowed to self-assess whether to prepare special purpose financial statements (SPFS) or general purpose financial statements (GPFS) when they are required to comply with Australian Accounting Standards (AAS) (see paragraphs BC10-BC13 for details). As is evident from empirical research and feedback from stakeholders (see paragraphs BC18-BC41), there is concern that SPFS lack consistency, comparability transparency and enforceability. The Board’s research has identified that there are users of financial statements that are publicly lodged with the Australian Securities and Investments Commission (ASIC), and the Board has been informed by those users that comparability, transparency, comprehensibility and consistency are what is most important to them when reading financial statements. For example comparability of recognition and measurement (R&M) requirements in AAS was rated 88% in importance to primary users[1] and 100% in importance to other users. They also expressed concern that key information is omitted from SPFSs (see paragraphs BC37-BC41).

BC3 Regulatory scrutiny of SPFS has also increased, for example in the Parliamentary Joint Committee on Corporations and Financial Services inquiry into the regulation of auditing, the Senate Economics References Committee Report on Tax Avoidance, and the requirement for all Significant Global Entities (SGEs) to lodge GPFS with the Australian Taxation Office (ATO) (see paragraph BC32(a)).

BC4 Within the context of the AASB’s International Financial Reporting Standards (IFRS Standards) adoption policy, the issue of a revised Conceptual Framework for Financial Reporting (March 2018) (referred to throughout this Basis for Conclusions as ‘the RCF’) by the International Accounting Standards Board (IASB) provides a timely opportunity to once again consider how best to improve the quality of financial reporting in Australia by solving the so-called ‘SPFS problem’ via a broader project aimed at removing the ability of certain for-profit private sector entities to prepare SPFS when they are required to prepare financial statements that comply with AAS.[2] The Board is progressing with this project by considering each sector separately, in the first instance for-profit private sector entities required to comply with AAS (being the subject of this Standard – as explained in paragraphs BC68-BC93).

BC5 The Board noted the Australian Government Treasury change in thresholds for large proprietary companies which defined the entities that are required to lodge their financial statements with ASIC (unless exempted by ASIC) in April 2019. Treasury doubled the thresholds used for determining what constitutes a large proprietary company. As set out in the Explanatory Memorandum accompanying the increase, the revised thresholds were set with the expectation of capturing entities with economic significance and noted the larger the entity, the more likely it is that there are GPFS users. These are key criteria in the AASB’s Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity for determining whether or not an entity is a reporting entity.

BC6 As noted in paragraph BC4, the solution to the SPFS problem provided by this Standard is to remove the ability of certain for-profit private sector entities to self-assess their financial reporting requirements and prepare SPFS when they are required to prepare financial statements that comply with AAS.[3] This will improve the consistency, comparability, transparency and enforceability of financial statements, thus meeting the needs of users who are accessing these financial statements on a public register or otherwise. The Board acknowledged that these changes could not be implemented in isolation, as merely removing the ability of certain for-profit private sector entities to prepare SPFS with no other mitigating action would result in increased reporting requirements for some entities if they were required to transition from SPFS to some form of Tier 2[4] GPFS framework. Therefore, this Standard is made in conjunction with AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities (March 2020), which provides simplified Tier 2 GPFS reporting requirements for those for-profit entities that are prohibited from preparing SPFS as a result of this Standard.

BC7 The Board also decided to provide transitional relief in addition to that which is currently available via AASB 1 First-time Adoption of Australian Accounting Standards and AASB 1053 (see paragraphs BC122-BC135), for entities that choose to early adopt the requirements in this Standard.

BC8 The remainder of this Basis for Conclusions provides further background and explanation about the reasons for developing this Standard, including:

(a) previous Board decisions in relation to earlier stages of the process (to provide a historical perspective, see for example paragraphs BC10-BC13);

(b) the basis for the key decisions made, including:

(i) the types of entities affected by the Standard and the technical requirements (including, for context, a summary of the basis for the revised Tier 2 GPFS framework (see paragraphs BC95-BC121), which is detailed in AASB 1060);

(ii) transitional provisions (see paragraphs BC122-BC135); and

(iii) the effective date (see paragraphs BC145-BC150);

(c) how the Board applied The AASB’s For-Profit Entity Standard-Setting Framework when developing this Standard (see paragraphs BC154-BC156); and

(d) the amendments necessary to implement the requirements outlined in this Standard (see paragraphs BC157-BC162.

(a) amendments to AAS to remove the ability of certain for-profit private sector entities to prepare SPFS by removing the ‘reporting entity’ concept for those entities required by:

(i) legislation to prepare financial statements that comply with either AAS or accounting standards; or

(ii) their constituting document (or another document) to prepare financial statements that comply with AAS, provided the relevant document was created or amended on or after 1 July 2021; and

(b) to provide relief from restating comparative information for entities transitioning to full R&M requirements, if the entity chooses to early adopt the requirements (see paragraphs BC122-BC135).

BC10 As noted in paragraph BC2, the Board had been aware of the problems with the application of the reporting entity concept and the consequential preparation and public lodgement of SPFS for some time. Indeed, the Board has previously publicly contemplated the removal of the ability of certain entities to self-assess and prepare SPFS when required to comply with AAS. For example:

(a) AASB Invitation to Comment ITC 12 Request for Comment on a Proposed Revised Differential Reporting Regime for Australia and IASB Exposure Draft of A Proposed IFRS for Small and Medium-sized Entities (May 2007) noted the concept of SPFS might have been misunderstood in some cases. To remove the ambiguity concerning the reporting entity concept, ITC 12 sought comment on whether all financial statements available on a public register should be required to be GPFS; and

(i) entities are asserted to be ‘abusing’ the reporting entity concept by claiming to be non-reporting entities and preparing SPFS when they should be preparing GPFS. An impetus for this is the desire to avoid the cost and exposure that would come from applying full IFRS Standards as adopted in Australia;

(ii) many of the regulators requiring the preparation and lodgement of financial statements may not have given sufficient consideration to the nature of the information they require and the needs of any external users of that information; and

(iii) preparation of SPFS by entities that are required by law to prepare financial statements in accordance with accounting standards and be lodged on a public register contradicts the legislation’s objective of providing information to a wide range of users who are not in a position to command specific information to satisfy their needs.

BC11 However, the Board noted mixed feedback from constituents in response to these due process documents in regard to removing the ability of certain entities to self-assess and prepare SPFS when required to comply with AAS, which suggested that (as noted in paragraphs BC10-BC17 of the Basis for Conclusions to AASB 1053):

(a) on the one hand, the reporting entity concept involves a high degree of subjectivity, is not universally understood and hence does not provide the intended result, nor does it provide a robust criterion for differential reporting purposes; and

BC12 Consequently, in 2010, the Board decided to issue AASB 1053 and introduce a second tier of GPFS reporting, being Tier 2: Australian Accounting Standards – Reduced Disclosure Requirements (RDR), but delay the phase of the project addressing the reporting entity concept and the removal of SPFS until further research had been undertaken. That research would consider in more detail the impact of removing the ability of certain entities to self-assess and prepare SPFS when required to comply with AAS. The RDR requirements were designed to substantially reduce the disclosure burden when compared to the full disclosure requirements of AAS.

BC13 Prompted by the views noted in paragraphs BC10-BC11, the Board initiated research projects, the findings of which are discussed in paragraphs BC18-BC25.

BC14 Australia is the only jurisdiction with a reporting entity concept that effectively permits entities to self-assess what type of financial reporting they do, when they are required by legislation or otherwise (such as by a constituting document) to prepare financial statements in accordance with AAS.[5] Therefore, unlike other jurisdictions, in Australia two similar entities might prepare very different sets of financial statements, one preparing GPFS using a robust and consistent framework, and the other preparing SPFS with self-selected requirements. This reduces comparability for entities of similar economic circumstances and undermines the fundamental principles of trust and transparency.

BC15 An analysis of the reporting practices of specified for-profit entities lodging financial statements with ASIC estimated that 71% of those entities prepared and publicly lodged SPFS in 2018. [6] This same research estimated that 24% of these entities lodging SPFS either did not comply with the R&M requirements in AAS or did not make clear whether they did (refer to paragraphs BC20-BC22). Therefore, only 76% of the SPFS voluntarily complied with ASIC Regulatory Guide 85 Reporting requirements for non-reporting entities (RG 85) recommended guidance to apply all the R&M requirements in AAS (refer BC28-BC29). This suggested a strong need to improve the consistency, comparability, transparency and enforceability of financial reporting, which would also increase the usefulness and credibility of financial reporting in Australia.

BC17 Therefore, as noted in paragraph BC6, the Board decided to play its role in improving the consistency, comparability, transparency and enforceability of financial statements to meet user needs, whilst mitigating, where appropriate, the increased reporting burden for entities that would no longer be able to prepare SPFS and would instead be required to prepare GPFS in accordance with AAS.

BC18 The Board initiated academic research that resulted in the publication of AASB Research Report No. 1 Application of the Reporting Entity Concept and Lodgement of Special Purpose Financial Statements (June 2014). Research Report No. 1 analysed the application of the reporting entity concept and the adoption of special purpose financial reporting, particularly by entities lodging financial statements with ASIC and with state-based regulators of Australia’s three most populous states, namely, Consumer Affairs Victoria, NSW Fair Trading and Queensland Office of Fair Trading. Research Report No. 1 showed that, based on lodgements as at 30 July 2011, approximately 66% of specified for-profit entities[7] lodged SPFS with ASIC. The findings of Research Report No. 1 indicated to the Board that:

(a) in light of the high incidence of SPFS being lodged with ASIC, there is doubt as to whether the reporting entity concept is being applied as intended by SAC 1;

(b) the reporting entity concept appears too subjective for regulators to enforce effectively and accordingly does not create a level playing field; and

BC19 The Board also initiated subsequent research[8] to understand how the reporting practices of for-profit entities lodging SPFS with ASIC may have changed since the introduction of the RDR reporting framework in 2010. An analysis of financial reports of the specified for-profit entities lodging financial statements with ASIC in 2018 confirmed that 71% of these entities were still lodging SPFS with ASIC, 13% lodged Tier 2 GPFS and 16% lodged Tier 1 GPFS. The Board also noted that those entities preparing Tier 2 GPFS (RDR) appear to have moved from Tier 1 GPFS to RDR and not from SPFS to RDR.

(a) 66% explicitly stated that they followed the R&M requirements in AAS (compared with the 63% found in Research Report No.1 – see paragraph BC18(c)); and

(b) 10% were assessed to have complied with the R&M requirements in AAS based on a qualitative review of the accounting policies, despite the absence of an explicit statement to that effect.

(a) 10% did not comply with the R&M requirements in AAS (of which only 0.5% clearly stated so); and

(b) the extent of compliance (or otherwise) with the R&M requirements in AAS of the remaining 14% was unclear.

BC22 In addition to it being difficult for the researchers to understand the extent of alignment between an entity’s accounting policies and the R&M requirements in AAS, the Board noted the same difficulties faced by financial statement users. This leads to fundamental issues with the transparency of information available to users of publicly lodged SPFS, consistency and the comparability of SPFS with other SPFS and GPFS. As noted in paragraph BC15, only 76% of entities preparing SPFS are voluntarily complying with RG 85 recommendations, suggesting that mandatory requirements were needed to improve the quality of financial reporting.

BC23 In response, in July 2019, the Board issued ED 293 Amendments to Australian Accounting Standards – Disclosure in Special Purpose Financial Statements of Compliance with Recognition and Measurement Requirements which proposed, as an interim measure, amendments to AAS to require entities preparing SPFS to make an explicit statement as to whether or not the accounting policies applied in the SPFS comply with all the R&M requirements in AAS. The Board acknowledged that disclosure of this information was not sufficient to address the problems with publicly lodged SPFS, however the interim measure was aimed at providing some measure of transparency to users until the resolution of the SPFS problem, in the short to medium term for for-profit private sector entities and in the longer term for not-for-profit entities. After considering feedback from respondents on ED 293, the Board decided to limit the scope of the proposals to only not-for-profit (NFP) entities as respondents “were particularly concerned about the costs of the ED 293 proposals exceeding any benefits for for-profit private sector entities given the ED 293 proposals were intended to be only a short-term measure for these entities. This is because the broader project proposing to remove the ability for certain for-profit private sector entities to prepare special purpose financial statements when they are required to comply with Australian Accounting Standards is expected to be completed by 30 June 2020.”[9]

BC24 In light of the effective date of this Standard being one year later than that proposed in ED 297, and also noting that there is likely to be a number of entities that will continue to be able to prepare SPFS (e.g. due to the exemption provided to entities with a non-legislative requirement to prepare financial statements that comply with AAS (refer paragraphs BC90-BC92)), the Board reconsidered this decision. The Board was concerned about the lack of transparency in the SPFS that continues to refer to AAS and therefore decided that these entities should also be required to disclose a statement of the entity’s compliance, or otherwise, with the R&M requirements in AAS (including requirements set out in AASB 10 Consolidated Financial Statements or AASB 128 Investments in Associates and Joint Ventures). The Board thought this was particularly important for securitisation trusts given they are listed on the ASX and other securities exchanges. The Board intends to communicate with the ASX and industry bodies to ensure they understand the implications of having SPFS on their public registers.

(a) other regulators should specify or determine whether an entity is required to lodge GPFS;[10] and

(b) if the reporting entity concept is not being applied correctly, this is a matter of enforcement for the appropriate regulator rather than a matter of standard-setting.

BC27 Thus, the Board has paid particular regard to the views of other regulators, and noted the increasing regulatory interest in and concern about the use of SPFS to assess what role the Board should play in addressing the issues.

BC28 The Board noted ASIC issued RG 85 in July 2005, which states “ASIC believes that non-reporting entities, which are required to prepare financial reports in accordance with Chapter 2M of the Corporations Act 2001 (Act), should comply with the recognition and measurement requirements of accounting standards”[11] “hence, the recognition and measurement requirements of accounting standards must also be applied in order to determine the financial position and profit or loss of any entity preparing financial reports in accordance with the Act”.[12]

BC29 RG 85 further states that “Directors of non-reporting entities must also consider carefully the need to make disclosures which are not directly prescribed by accounting standards, but which may be necessary in order for the financial statements to give a true and fair view”,[13] and that those standards that must be applied by entities reporting under the Corporations Act 2001 are AASB 101 Presentation of Financial Statements, AASB 107 Statement of Cash Flows, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors, AASB 1048 Interpretation of Standards and AASB 1054 Australian Additional Disclosures. However, as noted in paragraph BC21, research into the extent of compliance with the R&M requirements in AAS by specified for-profit entities lodging SPFS with ASIC shows that at least 10% and potentially up to 24% of them do not appear to have followed the guidance outlined in RG 85. ASIC has also indicated it finds the judgements required regarding the application of the reporting entity concept in SAC 1 to be unenforceable.

BC30 The appropriateness of SPFS have also been called into question in a number of other regulatory matters. For example, as part of the Senate Economics References Committee Report on Tax Avoidance, the Board’s Chair was asked to explain to the Committee the reporting entity concept and its role in facilitating the preparation of SPFS. The Board noted the subsequent Report, Corporate tax avoidance Part III, Much heat, little light so far (May 2018), outlined strong concern that multinationals operating within Australia are avoiding public scrutiny through the preparation of SPFS, which are not required to disclose corporate tax and related party transactions, and also noted the Board’s role in facilitating the public lodgement of SPFS through its reporting entity concept. The Report recommended the Government require all companies, trusts and other financial entities with income above a certain amount to lodge GPFS with ASIC. These comments, albeit with a focus on tax, reinforce the view that a problem exists in relation to the way in which the reporting entity concept is applied, as well as the information provided through the public lodgement of SPFS.

BC31 The Board also reflected on the recommendations in the Final Report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (February 2019), particularly the recommendation to remove special rules and exceptions that can create regulatory complexities. The Final Report indicated that exceptions departing from underlying principles have consequences often resulting in exploitation and that exceptions act as barriers to the simplification of regulation. The Board further considered the theme of enforceability within the Final Report, noting in particular that the subjectivity inherent in the current Australian reporting entity concept may not provide regulators with an objective basis on which to enforce financial reporting obligations.

(a) the requirement for SGEs[14] to lodge GPFS with the ATO, which would subsequently be provided to ASIC[15] (December 2015);

(b) questions to the Board’s Chair and the Financial Reporting Council’s (FRC) Chair on the AASB’s and FRC’s approaches to resolving the shortcomings of SPFS by the Parliamentary Joint Committee on Corporations and Financial Services as part of its inquiry into the oversight of ASIC and the Takeovers Panel (February 2018);

(c) the Senate Economics References Committee report Financial and tax practices of for-profit aged care providers (November 2018), which supported the Board’s intent to remove the ability of certain entities to prepare SPFS where they are required to prepare financial statements that comply with AAS; and

(d) further questions to the Board’s Chair on the status of the AASB’s work to remove SPFS from the Parliamentary Joint Committee on Corporations and Financial Services as part of its inquiry into the regulation of auditing in Australia (November 2019). SPFS were criticised both by members of that committee as well as in several submissions from the public in relation to that inquiry.

BC33 In light of the regulatory developments and public enquiries noted above, the Board also observed the increasing public interest and media scrutiny of the transparency and accountability of publicly available financial statements, both generally and specifically in relation to the reporting entity concept and its facilitation of publicly lodged SPFS.

BC34 In proposing to remove the ability of certain for-profit private sector entities to prepare SPFS when they are required to prepare financial statements that comply with AAS, the Board received support from other regulators, particularly ASIC and the ATO, which conveyed the following views to the Board:

(a) ASIC fully supports the consultation to remove SPFS for entities regulated by ASIC and remove the subjective ‘reporting entity’ test under SAC 1, facilitating a comparable, consistent and transparent framework for the preparation of financial statements in Australia; and

(b) the ATO is supportive of the AASB’s proposed approach to consulting on a series of principles or concepts for enhancing the transparency of entities currently preparing SPFS as part of adopting the RCF issued by the IASB and for inclusion in AAS by 2021. The ATO also noted its further support of the AASB’s recommendations surrounding the timing and application of the new Tier 2 disclosures requirements during the Board’s Exposure Draft process.

BC35 The Board provided input to Treasury in considering legislative requirements that specify which types of for-profit entities should be required to prepare and, in most cases, publicly lodge financial statements with ASIC. In April 2019, Treasury announced changes to the Corporations Regulations 2001[16] to increase (double) the thresholds used for determining whether an entity is a large proprietary company, with companies falling below the thresholds not being required to prepare or publicly lodge financial reports with ASIC. As part of the changes, the Board suggested Treasury provide objective criteria based on economic significance for determining the thresholds and noted the commentary in Treasury’s Explanatory Statement, which is consistent with the Board’s decision to remove the ability of certain entities to prepare SPFS when they are required to prepare financial statements that comply with AAS. In particular, the Board noted:

(a) the requirement for large proprietary companies to prepare and in some cases lodge financial reports was first introduced to focus regulation of reporting on the financial affairs of proprietary companies that have a significant economic influence; and

(b) the financial reports of companies that have economic significance should be publicly available because of their size and potential to affect the community and the economy. The larger the size, the more likely it is that there will exist users dependent on GPFS as a basis for making economic decisions.

BC36 This clearly indicates the new thresholds which apply from 1 July 2019 were set to reflect the ‘economic significance’ of the entities captured, which is another key criterion in SAC 1 for deciding whether or not an entity is a reporting entity.

BC38 As part of the due process, a significant amount of feedback was provided by users of financial statements. Of particular importance is the AASB Staff Paper Enhancing the revised Conceptual Framework and replacing Special Purpose Financial Statements – For-profit User and Preparer Survey Results (December 2018), which indicated that, from the perspective of the 37 users (analysts, investors and creditors) that responded:

(a) there is a problem with SPFS that needs to be addressed – 78% of primary users expressed concern that SPFS do not consistently apply R&M requirements in AAS;

(b) 93% of primary users and over 95% of other users said that comparability, transparency, comprehensibility and consistency are all paramount; and

(c) there is dissatisfaction with SPFS that needs to be addressed, particularly around the lack of related party disclosures, lack of comparability and that the extent to which entities comply with the R&M requirements in AAS is unclear to users.

BC39 The Board also conducted a range of meetings with users to understand their needs and received six formal submissions on ITC 39 from users of financial statements (out of the 33 responses relevant to this phase of the project). In those formal submissions, the Board noted that all of those respondents:

(a) noted, or referred to, the lack of comparability, consistency and transparency currently caused by SPFS that needs to be resolved; and

(b) supported public lodgement of financial statements that comply with all of the R&M requirements in AAS. Consistency, transparency and comparability were noted as important to users in their responses, with one user also noting the importance of consistent financial reporting to facilitate computer-based analysis and use of financial information.

(a) over 98,000 copies of financial statements were purchased during the year ending 30 June 2018 from ASIC. Of those financial statements purchased, 80% were of proprietary companies, 16% were of unlisted public companies and 4% were of small foreign-controlled companies;[17]

(b) anecdotally, data aggregators[18] rely on publicly available information to assist their clients with determining the viability, capacity and credit risk associated with a company; and

(a) small foreign-controlled companies have been specifically required to lodge financial statements with ASIC[19], and are already provided with significant relief from financial reporting obligations if the company is included in the consolidated financial statements of a registered foreign company that is lodged with ASIC. Additionally, ASIC Corporations (Foreign-Controlled Company Reports) Instrument 2017/204 provides further relief to small foreign-controlled entities – even if they are not consolidated by a registered foreign company lodging financial statements with ASIC – by requiring them to lodge financial statements with ASIC only if directed to do so by shareholders or ASIC, or if they are part of a large group in Australia. The requirement for small foreign-controlled companies to lodge financial statements where they are part of a large group is designed to prevent foreign-controlled companies disaggregating their Australian activities into smaller companies to avoid financial reporting obligations.[20] In light of this Australian public interest context, demonstrated also through the requirements for SGEs to lodge GPFS with the ATO and the strong public interest in seeing no avoidance of tax, there appears to be no justification for small foreign-controlled companies to be relieved from the requirement to prepare GPFS; and

(b) unlisted public companies by definition would have at least 50 non-employee shareholders (ie external users) and have the ability to offer shares to the public. As such, the Board noted it would be difficult to justify there being no external users of such entities’ financial statements – and therefore GPFS are warranted. In addition, it is possible that some of the 3,102 unlisted public companies[21] currently lodging financial statements with ASIC may be not-for-profit entities, and as such would not be affected by this Standard.

BC42 The IASB issued the RCF in March 2018. The RCF describes the objective and concepts for general purpose financial reporting under IFRS Standards. Its purpose is to assist standard-setters to develop Standards that are based on consistent concepts, and to help preparers develop consistent accounting policies when no Standard applies to a particular transaction or event, or when a Standard allows a choice of accounting policy.[22] It also assists anyone looking to understand and interpret the Standards. However, the RCF’s concept of ‘reporting entity’ is different from the reporting entity concept in SAC 1 and some AAS.[23]

BC43 Making the IASB’s RCF applicable in Australia, modified where necessary for public sector and NFP specific issues, is consistent with the FRC’s strategic direction to the Board and the Board’s strategic objectives. In accordance with those strategies, the Board should:

(a) maintain compliance with IFRS Standards for publicly accountable entities; and

(b) use IFRS Standards as a base for determining the reporting requirements for all other entities, modified as appropriate, in accordance with The AASB’s For-Profit Entity Standard-Setting Framework and The AASB’s Not-for-Profit Entity Standard-Setting Framework.

BC44 However, if the AASB’s current reporting entity concept were maintained at the same time the RCF is applied, the inconsistency of the Australian reporting entity concept with the RCF could result in confusion, misinterpretation and the incorrect application of AAS and non-compliance with IFRS Standards. The likelihood of inconsistencies would also increase as and when IFRS Standards are amended or revised and more references to the term ‘reporting entity’ as defined in the RCF are included in IFRS Standards.

(a) GPFS, which requires compliance with all AAS, including recognition, measurement, presentation and disclosure requirements; or

The ability of entities to self-assess their reporting requirements under the Australian reporting entity concept has led to the more fundamental ‘SPFS problem’.

BC46 Further, the SAC 1 reporting entity concept has led to confusion and diversity in practice regarding whether consolidation and equity accounting should be applied in SPFS publicly lodged with ASIC. RG 85 notes that some “companies have failed to prepare consolidated financial statements on the grounds that the parent entity was not a reporting entity”[24] and that the “sole determining factor as to whether consolidated financial statements are required is whether the group is a reporting entity” (emphasis added).[25] The RCF and AASB 10 however, require consolidation if an entity is a parent, with limited exceptions.[26]

BC48 To address the reporting entity clash, ITC 39 considered a number of options to apply the RCF (refer to paragraphs BC52-BC57), including considering whether it would be feasible to operate with two conceptual frameworks[27] – the RCF for publicly accountable entities and entities that wish to claim IFRS compliance, and the current Framework for the Preparation and Presentation of Financial Statements (existing Conceptual Framework) for other entities (which would include maintaining SAC 1, the Australian reporting entity concept and SPFS for all entities not applying the RCF). However, the Board decided that this option was not feasible, as new and revised AAS will be based on the RCF, which includes revised definitions and recognition criteria for assets and liabilities, a new chapter on the reporting entity and a new chapter on measurement. Therefore, if entities continued to apply the existing Conceptual Framework when developing accounting policies or interpreting AAS, they are likely to develop inappropriate accounting policies or incorrectly interpret AAS. This could result in inaccurate and inconsistent financial reporting which would reduce the transparency and comparability for users of financial statements.

BC49 Updating the existing Conceptual Framework for the changes made via the RCF other than the reporting entity concept was also not feasible given the pervasive use of ‘reporting entity’ throughout the RCF. The Board also considered an option to simply rename the reporting entity concept in SAC 1 to resolve the reporting entity clash.[28] The Board however decided that this approach would not meet any of the justifiable circumstances set out in The AASB’s For-Profit Entity Standard-Setting Framework for the AASB to have different requirements to IFRS Standards. Further, this would be inconsistent with the AASB’s legislative requirements to ensure there are appropriate accounting standards for each type of entity that must comply with accounting standards and to facilitate consistency, comparability, transparency and enforceability (refer paragraph BC16). This is because such an approach would not resolve the fundamental issues with the public lodgement of SPFS, which is addressed in the next section, or the evident inconsistency in practice and lack of transparency.

BC50 In light of the evidence provided to the Board in paragraphs BC9-BC49, the Board decided to resolve the clash between the reporting entity concepts, as well as to improve the consistency, comparability, transparency and enforceability of the for-profit private sector financial reporting framework, it is necessary to remove the Australian reporting entity concept (by making the consequential amendments to AAS set out in this Standard). This would remove the ability of an entity to self-assess that it is not a ‘reporting entity’ as currently defined in SAC 1, and so prevent it from preparing SPFS if it is required to prepare financial statements that comply with AAS.

BC51 The Board concluded the removal of the self-assessment of the reporting entity concept and disallowance of the preparation of SPFS for certain for-profit private sector entities would simplify the reporting framework by providing a single set of minimum requirements, facilitating the objective of a consistent, comparable, transparent and enforceable Australian financial reporting framework. In arriving at this solution the Board considered a range of alternatives through ITC 39, as noted in the next section.

(a) in the short term maintaining compliance with IFRS Standards for publicly accountable for-profit private sector entities required by legislation to comply with AAS and other for-profit entities voluntarily claiming compliance with IFRS Standards (Phase 1); and

(b) in the medium term maintaining IFRS Standards as a base by removing the Australian reporting entity concept from AAS and providing a revised Tier 2 GPFS framework (Phase 2). This would remove the ability of an entity to prepare SPFS where they are required to prepare financial statements that comply with AAS.

BC53 The Board decided in favour of this two-phased approach because it:

(a) allowed for-profit private sector entities with public accountability and entities that voluntarily report compliance with IFRS Standards to continue to do so;

(b) allowed all other entities to continue preparing SPFS in the short term while the Board undertook consultation and outreach activities and determined the appropriate Tier 2 GPFS framework to replace SPFS;

(c) maintained IFRS Standards as a base for all entities in the medium term;

(d) solved the reporting entity problem in the medium term;

(e) solved the SPFS problem in the medium term;

(f) allowed time for the Board to consult and determine any NFP modifications that may be necessary to the RCF in accordance with The AASB’s Not-for-Profit Entity Standard-Setting Framework; and

(g) facilitated comparability and ensured there were appropriate accounting standards for each type of entity required to prepare financial statements that comply with AAS.

BC54 Phase 1 implemented the RCF for publicly accountable for-profit private sector entities and other entities voluntarily reporting compliance with IFRS Standards so that they continue to maintain IFRS compliance when the RCF took effect internationally on 1 January 2020. Entities in Australia with public accountability must apply the full IFRS Standards as AAS incorporate IFRS Standards and therefore, the Board reconfirmed its view that for-profit private sector entities in Australia with public accountability should be required to prepare Tier 1 GPFS. The Board completed Phase 1 in May 2019 (see AASB 2019-1 Amendments to Australian Accounting Standards – References to the Conceptual Framework).

(a) RDR – The existing Tier 2 GPFS framework as currently exists in AASB 1053, consisting of full R&M, including consolidation and equity accounting (where applicable) with reduced disclosures from each applicable AAS; or

(b) Specified Disclosure Requirements (SDR) – A new Tier 2 GPFS framework that would consist of full R&M including consolidation and equity accounting (where applicable), however with specified disclosures from only some AAS.

The Board subsequently decided that neither RDR nor SDR were appropriate Tier 2 disclosure frameworks. The Board instead decided to develop another alternative, the Simplified Disclosures Framework, as enacted by AASB 1060 and explained further in paragraph BC98.