AASB Standard | AASB 2021-2 |

[AASB 7, AASB 101, AASB 108, AASB 134 & AASB Practice Statement 2]

This Standard is available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: standard@aasb.gov.au

Website: www.aasb.gov.au

Phone: (03) 9617 7600

E-mail: standard@aasb.gov.au

COPYRIGHT

© Commonwealth of Australia 2021

This AASB Standard contains IFRS Foundation copyright material. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

ISSN 1036-4803

Preface

Accounting Standard

AASB 2021-2 Amendments to Australian Accounting Standards – Disclosure of Accounting Policies and Definition of Accounting Estimates

from page

Application 5

Amendments to AASB 101 5

Amendments to AASB 108 8

AMENDMENTS TO OTHER AASB STANDARDS AND PUBLICATIONS 9

Amendments to AASB 7 9

Amendments to AASB 134 11

Amendments to AASB Practice Statement 2 11

COMMENCEMENT OF THE LEGISLATIVE INSTRUMENT 17

aVailable on the AASB website

IASB Implementation guidance – Amendments

IASB Bases for Conclusions – Amendments

Australian Accounting Standard AASB 2021-2 Amendments to Australian Accounting Standards – Disclosure of Accounting Policies and Definition of Accounting Estimates is set out on pages 5 – 17. All the paragraphs have equal authority.

This Standard makes amendments to the following Australian Accounting Standards:

(a) AASB 7 Financial Instruments: Disclosures (August 2015);

(b) AASB 101 Presentation of Financial Statements (July 2015);

(c) AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors (August 2015); and

(d) AASB 134 Interim Financial Reporting (August 2015).

The Standard also makes amendments to AASB Practice Statement 2 Making Materiality Judgements (December 2017).

These amendments arise from the issuance by the International Accounting Standards Board (IASB) in February 2021 of the following International Financial Reporting Standards:

(a) Disclosure of Accounting Policies (Amendments to IAS 1 and IFRS Practice Statement 2); and

(b) Definition of Accounting Estimates (Amendments to IAS 8).

Main requirements

This Standard amends:

(a) AASB 7, to clarify that information about measurement bases for financial instruments is expected to be material to an entity’s financial statements;

(b) AASB 101, to require entities to disclose their material accounting policy information rather than their significant accounting policies;

(c) AASB 108, to clarify how entities should distinguish changes in accounting policies and changes in accounting estimates;

(d) AASB 134, to identify material accounting policy information as a component of a complete set of financial statements; and

(e) AASB Practice Statement 2, to provide guidance on how to apply the concept of materiality to accounting policy disclosures.

Application date

This Standard applies to annual periods beginning on or after 1 January 2023. The amendments to individual Standards may be applied early, separately from the amendments to the other Standards, where feasible.

The Australian Accounting Standards Board makes Accounting Standard AASB 2021-2 Amendments to Australian Accounting Standards – Disclosure of Accounting Policies and Definition of Accounting Estimates under section 334 of the Corporations Act 2001.

| Keith Kendall |

Dated 30 March 2021 | Chair – AASB |

Amendments to Australian Accounting Standards – Disclosure of Accounting Policies and Definition of Accounting Estimates

This Standard amends:

(a) AASB 7 Financial Instruments: Disclosures (August 2015);

(b) AASB 101 Presentation of Financial Statements (July 2015);

(c) AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors (August 2015);

(d) AASB 134 Interim Financial Reporting (August 2015); and

(e) AASB Practice Statement 2 Making Materiality Judgements (December 2017);

as a consequence of the issuance by the International Accounting Standards Board in February 2021 of the following International Financial Reporting Standards:

(f) Disclosure of Accounting Policies (Amendments to IAS 1 and IFRS Practice Statement 2); and

(g) Definition of Accounting Estimates (Amendments to IAS 8).

The amendments set out in this Standard apply to entities and financial statements in accordance with the application of the other Standards set out in AASB 1057 Application of Australian Accounting Standards.

This Standard applies to annual periods beginning on or after 1 January 2023. The amendments to individual Standards may be applied early, separately from the amendments to the other Standards, where feasible.

This Standard uses underlining, striking out and other typographical material to identify some of the amendments to a Standard, in order to make the amendments more understandable. However, the amendments made by this Standard do not include that underlining, striking out or other typographical material. Ellipses (…) are used to help provide the context within which amendments are made and also to indicate text that is not amended.

Paragraphs 7, 10, 114, 117 and 122 are amended. Paragraphs 117A–117E and 139V are added. Paragraphs 118, 119 and 121 are deleted. New text is underlined and deleted text is struck through. |

Definitions

7 The following terms are used in this Standard with the meanings specified:

Accounting policies are defined in paragraph 5 of AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors, and the term is used in this Standard with the same meaning.

...

Financial statements

...

Complete set of financial statements

10 A complete set of financial statements comprises:

…

(e) notes, comprising material significant accounting policy information policies and other explanatory information;

…

Structure and content

...

Notes

Structure

...

114 Examples of systematic ordering or grouping of the notes include:

…

(c) following the order of the line items in the statement(s) of profit or loss and other comprehensive income and the statement of financial position, such as:

…

(ii) material significant accounting policy information policies applied (see paragraph 117);

…

Disclosure of accounting policy information policies

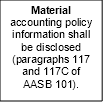

117 An entity shall disclose material its significant accounting policy information (see paragraph 7). Accounting policy information is material if, when considered together with other information included in an entity’s financial statements, it can reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements. policies comprising:

(a) the measurement basis (or bases) used in preparing the financial statements; and

(b) the other accounting policies used that are relevant to an understanding of the financial statements.

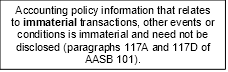

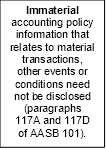

117A Accounting policy information that relates to immaterial transactions, other events or conditions is immaterial and need not be disclosed. Accounting policy information may nevertheless be material because of the nature of the related transactions, other events or conditions, even if the amounts are immaterial. However, not all accounting policy information relating to material transactions, other events or conditions is itself material.

117B Accounting policy information is expected to be material if users of an entity’s financial statements would need it to understand other material information in the financial statements. For example, an entity is likely to consider accounting policy information material to its financial statements if that information relates to material transactions, other events or conditions and:

(a) the entity changed its accounting policy during the reporting period and this change resulted in a material change to the information in the financial statements;

(b) the entity chose the accounting policy from one or more options permitted by Australian Accounting Standards—such a situation could arise if the entity chose to measure investment property at historical cost rather than fair value;

(c) the accounting policy was developed in accordance with AASB 108 in the absence of an Australian Accounting Standard that specifically applies;

(d) the accounting policy relates to an area for which an entity is required to make significant judgements or assumptions in applying an accounting policy, and the entity discloses those judgements or assumptions in accordance with paragraphs 122 and 125; or

(e) the accounting required for them is complex and users of the entity’s financial statements would otherwise not understand those material transactions, other events or conditions—such a situation could arise if an entity applies more than one Australian Accounting Standard to a class of material transactions.

117C Accounting policy information that focuses on how an entity has applied the requirements of the Australian Accounting Standards to its own circumstances provides entity-specific information that is more useful to users of financial statements than standardised information, or information that only duplicates or summarises the requirements of the Standards.

117D If an entity discloses immaterial accounting policy information, such information shall not obscure material accounting policy information.

117E An entity’s conclusion that accounting policy information is immaterial does not affect the related disclosure requirements set out in other Australian Accounting Standards.

118 [Deleted]It is important for an entity to inform users of the measurement basis or bases used in the financial statements (for example, historical cost, current cost, net realisable value, fair value or recoverable amount) because the basis on which an entity prepares the financial statements significantly affects users’ analysis. When an entity uses more than one measurement basis in the financial statements, for example when particular classes of assets are revalued, it is sufficient to provide an indication of the categories of assets and liabilities to which each measurement basis is applied.

119 [Deleted]In deciding whether a particular accounting policy should be disclosed, management considers whether disclosure would assist users in understanding how transactions, other events and conditions are reflected in reported financial performance and financial position. Each entity considers the nature of its operations and the policies that the users of its financial statements would expect to be disclosed for that type of entity. Disclosure of particular accounting policies is especially useful to users when those policies are selected from alternatives allowed in Australian Accounting Standards. An example is disclosure of whether an entity applies the fair value or cost model to its investment property (see AASB 140 Investment Property). Some Australian Accounting Standards specifically require disclosure of particular accounting policies, including choices made by management between different policies they allow. For example, AASB 116 requires disclosure of the measurement bases used for classes of property, plant and equipment.

120 [Deleted]

121 [Deleted]An accounting policy may be significant because of the nature of the entity’s operations even if amounts for current and prior periods are not material. It is also appropriate to disclose each significant accounting policy that is not specifically required by Australian Accounting Standards but the entity selects and applies in accordance with AASB 108.

122 An entity shall disclose, along with material its significant accounting policy information policies or other notes, the judgements, apart from those involving estimations (see paragraph 125), that management has made in the process of applying the entity’s accounting policies and that have the most significant effect on the amounts recognised in the financial statements.

...

Transition and effective date

...

139V AASB 2021-2 Amendments to Australian Accounting Standards – Disclosure of Accounting Policies and Definition of Accounting Estimates, issued in March 2021, amended paragraphs 7, 10, 114, 117 and 122, added paragraphs 117A–117E and deleted paragraphs 118, 119 and 121. It also amended AASB Practice Statement 2 Making Materiality Judgements. An entity shall apply the amendments to AASB 101 for annual reporting periods beginning on or after 1 January 2023. Earlier application is permitted. If an entity applies those amendments for an earlier period, it shall disclose that fact.

Paragraphs 5, 32, 34, 38 and 48 and the heading above paragraph 32 are amended. Paragraphs 32A–32B, 34A and 54I and the headings above paragraphs 34 and 36 are added. The heading above paragraph 39 is amended to be a sub-heading of the heading added above paragraph 34. Deleted text is struck through and new text is underlined. |

Definitions

5 The following terms are used in this Standard with the meanings specified:

Accounting estimates are monetary amounts in financial statements that are subject to measurement uncertainty.

…

A change in accounting estimate is an adjustment of the carrying amount of an asset or a liability, or the amount of the periodic consumption of an asset, that results from the assessment of the present status of, and expected future benefits and obligations associated with, assets and liabilities. Changes in accounting estimates result from new information or new developments and, accordingly, are not corrections of errors.

…

Accounting Changes in accounting estimates

32 An accounting policy may require items in financial statements to be measured in a way that involves measurement uncertainty – that is, the accounting policy may require such items to be measured at monetary amounts that cannot be observed directly and must instead be estimated. In such a case, an entity develops an accounting estimate to achieve the objective set out by the accounting policy. As a result of the uncertainties inherent in business activities, many items in financial statements cannot be measured with precision but can only be estimated. Developing accounting estimates involves the use of judgements or assumptions Estimation involves judgements based on the latest available, reliable information. Examples of accounting estimates include For example, estimates may be required of:

(a) a loss allowance for expected credit losses, applying AASB 9 Financial Instruments bad debts;

(b) the net realisable value of an item of inventory, applying AASB 102 Inventories inventory obsolescence;

(c) the fair value of an asset or liability, applying AASB 13 Fair Value Measurement financial assets or financial liabilities;

(d) the depreciation expense for an item of property, plant and equipment, applying AASB 116 the useful lives of, or expected pattern of consumption of the future economic benefits embodied in, depreciable assets; and

(e) a provision for warranty obligations, applying AASB 137 Provisions, Contingent Liabilities and Contingent Assets.

32A An entity uses measurement techniques and inputs to develop an accounting estimate. Measurement techniques include estimation techniques (for example, techniques used to measure a loss allowance for expected credit losses applying AASB 9) and valuation techniques (for example, techniques used to measure the fair value of an asset or liability applying AASB 13).

32B The term ‘estimate’ in Australian Accounting Standards sometimes refers to an estimate that is not an accounting estimate as defined in this Standard. For example, it sometimes refers to an input used in developing accounting estimates.

…

Changes in accounting estimates

34 An entity may need to change an accounting estimate may need revision if changes occur in the circumstances on which the accounting estimate was based or as a result of new information, new developments or more experience. By its nature, a change in an accounting the revision of an estimate does not relate to prior periods and is not the correction of an error.

34A The effects on an accounting estimate of a change in an input or a change in a measurement technique are changes in accounting estimates unless they result from the correction of prior period errors.

…

Applying changes in accounting estimates

36 …

38 Prospective recognition of the effect of a change in an accounting estimate means that the change is applied to transactions, other events and conditions from the date of that the change in estimate. A change in an accounting estimate may affect only the current period’s profit or loss, or the profit or loss of both the current period and future periods. For example, a change in a loss allowance for expected credit losses the estimate of the amount of bad debts affects only the current period’s profit or loss and therefore is recognised in the current period. However, a change in the estimated useful life of, or the expected pattern of consumption of the future economic benefits embodied in, a depreciable asset affects depreciation expense for the current period and for each future period during the asset’s remaining useful life. In both cases, the effect of the change relating to the current period is recognised as income or expense in the current period. The effect, if any, on future periods is recognised as income or expense in those future periods.

Disclosure

Disclosure

39 …

Errors

…

48 Corrections of errors are distinguished from changes in accounting estimates. Accounting estimates by their nature are approximations that may need changing revision as additional information becomes known. For example, the gain or loss recognised on the outcome of a contingency is not the correction of an error.

…

Effective date and transition

…

54I AASB 2021-2 Amendments to Australian Accounting Standards – Disclosure of Accounting Policies and Definition of Accounting Estimates, issued in March 2021, amended paragraphs 5, 32, 34, 38 and 48 and added paragraphs 32A, 32B and 34A. An entity shall apply these amendments for annual reporting periods beginning on or after 1 January 2023. Earlier application is permitted. An entity shall apply the amendments to changes in accounting estimates and changes in accounting policies that occur on or after the beginning of the first annual reporting period in which it applies the amendments.

Amendments to AASB 7

Paragraphs 21 and B5 are amended. Paragraph 44II is added. New text is underlined and deleted text is struck through. |

Significance of financial instruments for financial position and performance

...

Other disclosures

Accounting policies

21 In accordance with paragraph 117 of AASB 101 Presentation of Financial Statements, an entity discloses material its significant accounting policy information policies comprising the measurement basis (or bases) used in preparing the financial statements and the other accounting policies used that are relevant to an understanding of the financial statements. Information about the measurement basis (or bases) for financial instruments used in preparing the financial statements is expected to be material accounting policy information.

...

Effective date and transition

...

44II AASB 2021-2 Amendments to Australian Accounting Standards – Disclosure of Accounting Policies and Definition of Accounting Estimates, which amends AASB 101 and AASB Practice Statement 2 Making Materiality Judgements, and was issued in March 2021, amended paragraphs 21 and B5. An entity shall apply that amendment for annual reporting periods beginning on or after 1 January 2023. Earlier application is permitted. If an entity applies the amendment for an earlier period, it shall disclose that fact.

...

Appendix B

Application guidance

...

Classes of financial instruments and level of disclosure (paragraph 6)

...

Other disclosure – accounting policies (paragraph 21)

B5 Paragraph 21 requires disclosure of material accounting policy information, which is expected to include information about the measurement basis (or bases) for financial instruments used in preparing the financial statements and the other accounting policies used that are relevant to an understanding of the financial statements. For financial instruments, such disclosure may include:

…

Paragraph 122 of AASB 101 also requires entities to disclose, along with material its significant accounting policy information policies or other notes, the judgements, apart from those involving estimations, that management has made in the process of applying the entity’s accounting policies and that have the most significant effect on the amounts recognised in the financial statements.

Amendments to AASB 134

Paragraph 5 is amended and paragraph 60 is added. New text is underlined and deleted text is struck through. |

Content of an interim financial report

5 AASB 101 defines a complete set of financial statements as including the following components:

…

(e) notes, material comprising significant accounting policy information policies and other explanatory information;

…

Effective date

...

60 AASB 2021-2 Amendments to Australian Accounting Standards – Disclosure of Accounting Policies and Definition of Accounting Estimates, which amends AASB 101 and AASB Practice Statement 2 Making Materiality Judgements, and was issued in March 2021, amended paragraph 5. An entity shall apply that amendment for annual reporting periods beginning on or after 1 January 2023. Earlier application is permitted. If an entity applies the amendment for an earlier period, it shall disclose that fact.

Paragraphs 88A–88G and their heading, and Examples S and T, are added. Paragraphs 117, 117A, 117B, 117C, 117D and 117E of AASB 101 are added to Appendix B and Appendix AusCF B. For ease of reading, new text is not underlined. |

Specific topics

...

Information about accounting policies

88A Paragraph 117 of AASB 101 requires an entity to disclose material accounting policy information.

88B Accounting policy information relating to immaterial transactions, other events or conditions is immaterial and need not be disclosed. Accounting policy information may nevertheless be material because of the nature of the related transactions, other events or conditions, even if the amounts are immaterial. An entity is required to disclose accounting policy information relating to material transactions, other events or conditions if that information is material to the financial statements.

88C In assessing whether accounting policy information is material to its financial statements, an entity considers whether users of the entity’s financial statements would need that information to understand other material information in the financial statements. An entity makes this assessment in the same way it assesses other information: by considering qualitative and quantitative factors, as described in paragraphs 44–55. Diagram 2 illustrates how an entity assesses whether accounting policy information is material and, therefore, shall be disclosed.

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Diagram 2—determining whether accounting policy information is material

Diagram 2—determining whether accounting policy information is material

88D Paragraph 117B of AASB 101 includes examples of circumstances in which an entity is likely to consider accounting policy information to be material to its financial statements. The list is not exhaustive, but provides guidance on when an entity would normally consider accounting policy information to be material.

88E Paragraph 117C of AASB 101 describes the type of material accounting policy information that users of financial statements find most useful. Users generally find information about the characteristics of an entity’s transactions, other events or conditions—entity-specific information—more useful than disclosures that only include standardised information, or information that duplicates or summarises the requirements of the Australian Accounting Standards. Entity-specific accounting policy information is particularly useful when that information relates to an area for which an entity has exercised judgement—for example, when an entity applies an Australian Accounting Standard differently from similar entities in the same industry.

88F Although entity-specific accounting policy information is generally more useful, material accounting policy information could sometimes include information that is standardised, or that duplicates or summarises the requirements of the Australian Accounting Standards. Such information may be material if, for example:

(a) users of the entity’s financial statements need that information to understand other material information provided in the financial statements. Such a scenario might arise when an entity applying AASB 9 Financial Instruments has no choice regarding the classification of its financial instruments. In such scenarios, users of that entity’s financial statements may only be able to understand how the entity has accounted for its material financial instruments if users also understand how the entity has applied the requirements of AASB 9 to its financial instruments.

(b) an entity reports in a jurisdiction in which entities also report applying local accounting standards.

(c) the accounting required by the Australian Accounting Standards is complex, and users of financial statements need to understand the required accounting. Such a scenario might arise when an entity accounts for a material class of transactions, other events or conditions by applying more than one Australian Accounting Standard.

88G Paragraph 117D of AASB 101 states that if an entity discloses immaterial accounting policy information, such information shall not obscure material information. Paragraphs 56–59 provide guidance about how to communicate information clearly and concisely in the financial statements.

Example S—making materiality judgements and focusing on entity-specific information while avoiding standardised (boilerplate) accounting policy information |

Background An entity operates within the telecommunications industry. It has entered into contracts with retail customers to deliver mobile phone handsets and data services. In a typical contract, the entity provides a customer with a handset and data services over three years. The entity applies AASB 15 Revenue from Contracts with Customers and recognises revenue when, or as, the entity satisfies its performance obligations in line with the terms of the contract. |

The entity has identified two performance obligations and related considerations: (a) the handset—the customer makes monthly payments for the handset over three years; and (b) data—the customer pays a fixed monthly charge to use a specified monthly amount of data over three years. |

For the handset, the entity concludes that it should recognise revenue when it satisfies the performance obligation (when it provides the handset to the customer). For the provision of data, the entity concludes that it should recognise revenue as it satisfies the performance obligation (as the entity provides data services to the customer over the three-year life of the contract). |

The entity notes that, in accounting for revenue it has made judgements about: (a) the allocation of the transaction price to the performance obligations; and (b) the timing of satisfaction of the performance obligations. The entity has concluded that revenue generated from these contracts is material to the reporting period. |

Application The entity notes that for contracts of this type it applies separate accounting policies for two sources of revenue, namely revenue from: (a) the sale of handsets; and (b) the provision of data services. |

Having identified revenue from contracts of this type as material to the financial statements, the entity assesses whether accounting policy information for revenue from these contracts is, in fact, material. |

The entity evaluates the effect of disclosing the accounting policy information by considering the presence of qualitative factors. The entity noted that its revenue recognition accounting policies: (a) were unchanged during the reporting period; (b) were not chosen from accounting policy options available in the Australian Accounting Standards; (c) were not developed in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors in the absence of an Australian Accounting Standard that specifically applies; and (d) are not so complex that primary users will be unable to understand the related revenue transactions without standardised descriptions of the requirements of AASB 15. |

However, some of the entity’s revenue recognition accounting policies relate to an area for which the entity has made significant judgements in applying its accounting policies—for example, in deciding how to allocate the transaction price to the performance obligations, and the timing of revenue recognition. |

The entity considers that, in addition to disclosing the information required by paragraphs 123–126 of AASB 15 about the significant judgements made in applying AASB 15, primary users of its financial statements are likely to need to understand related accounting policy information. Consequently, the entity concludes that such accounting policy information could reasonably be expected to influence the decisions of the primary users of its financial statements. For example, understanding: (a) how the entity allocates the transaction price to its performance obligations is likely to help users understand how each component of the transaction contributes to the entity’s revenue and cash flows; and (b) that some revenue is recognised at a point in time and some is recognised over time is likely to help users understand how reported cash flows relate to revenue. |

The entity also notes that the judgements it made are specific to the entity. Consequently, material accounting policy information would include information about how the entity has applied the requirements of AASB 15 to its specific circumstances. |

The entity, therefore, assesses that accounting policy information about revenue recognition is material and should be disclosed. Such disclosure would include information about how the entity allocates the transaction price to its performance obligations and when the entity recognises revenue. |

Example T—making materiality judgements on accounting policy information that only duplicates requirements in the Australian Accounting Standards |

Background Property, plant and equipment are material to an entity’s financial statements. |

The entity has no intangible assets or goodwill and has not recognised an impairment loss on its property, plant or equipment in either the current or comparative reporting periods. |

In previous reporting periods, the entity disclosed accounting policy information relating to impairment of non-current assets which duplicates the requirements of AASB 136 Impairment of Assets and provides no entity-specific information. The entity disclosed that: |

The carrying amounts of the group’s intangible assets and its property, plant and equipment are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists, the asset’s recoverable amount is estimated. For goodwill and intangibles with an indefinite useful life, the recoverable amount is estimated at least annually. An impairment loss is recognised in the statement of profit or loss whenever the carrying amount of an asset or its cash-generating unit exceeds its recoverable amount. The recoverable amount of assets is the greater of their fair value less costs to sell and their value in use. In measuring value in use, estimated future cash flows are discounted to present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. For an asset that does not generate largely independent cash inflows, the recoverable amount is determined for the cash-generating unit to which the asset belongs. Impairment losses recognised in respect of cash-generating units are allocated first to reduce the carrying amount of any goodwill allocated to that cash-generating unit and then to reduce the carrying amount of the other assets in the unit on a pro rata basis. An impairment loss in respect of goodwill is not subsequently reversed. For other assets, an impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount, but only to the extent that the new carrying amount does not exceed the carrying amount that would have been determined, net of depreciation and amortisation, if no impairment loss had been recognised. |

Application Having identified assets subject to impairment testing as being material to the financial statements, the entity assesses whether the accounting policy information for impairment is, in fact, material. |

As part of its assessment, the entity considers that an impairment or a reversal of an impairment had not occurred in the current or comparative reporting periods. Consequently, accounting policy information about how the entity recognises and allocates impairment losses is unlikely to be material to its primary users. Similarly, because the entity has no intangible assets or goodwill, information about its accounting policy for impairments of intangible assets and goodwill is unlikely to provide its primary users with material information. |

However, the entity’s impairment accounting policy relates to an area for which the entity is required to make significant judgements or assumptions, as described in paragraphs 122 and 125 of AASB 101. Given the entity’s specific circumstances, it concludes that information about its significant judgements and assumptions related to its impairment assessments could reasonably be expected to influence the decisions of the primary users of the entity’s financial statements. The entity notes that its disclosures about significant judgements and assumptions already include information about the significant judgements and assumptions used in its impairment assessments. |

The entity decides that the primary users of its financial statements would be unlikely to need to understand the recognition and measurement requirements of AASB 136 to understand related information in the financial statements. |

Consequently, the entity concludes that disclosing a summary of the requirements in AASB 136 in a separate accounting policy for impairment would not provide information that could reasonably be expected to influence decisions made by the primary users of its financial statements. Instead, the entity discloses material accounting policy information related to the significant judgements and assumptions the entity has applied in its impairment assessments elsewhere in the financial statements. |

Although the entity assesses some accounting policy information for impairments of assets as immaterial, the entity still assesses whether other disclosure requirements of AASB 136 provide material information that should be disclosed. |

...

Appendix B

References to the Conceptual Framework for Financial Reporting and Australian Accounting Standards

...

Extracts from AASB 101 Presentation of Financial Statements

…

Paragraph 117

Referred to in paragraphs 88A and 88C of the Practice Statement

An entity shall disclose material accounting policy information (see paragraph 7). Accounting policy information is material if, when considered together with other information included in an entity’s financial statements, it can reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements.

Paragraph 117A

Referred to in paragraph 88C of the Practice Statement

Accounting policy information that relates to immaterial transactions, other events or conditions is immaterial and need not be disclosed. Accounting policy information may nevertheless be material because of the nature of the related transactions, other events or conditions, even if the amounts are immaterial. However, not all accounting policy information relating to material transactions, other events or conditions is itself material.

Paragraph 117B

Referred to in paragraphs 88C and 88D of the Practice Statement

Accounting policy information is expected to be material if users of an entity’s financial statements would need it to understand other material information in the financial statements. For example, an entity is likely to consider accounting policy information material to its financial statements if that information relates to material transactions, other events or conditions and:

(a) the entity changed its accounting policy during the reporting period and this change resulted in a material change to the information in the financial statements;

(b) the entity chose the accounting policy from one or more options permitted by Australian Accounting Standards—such a situation could arise if the entity chose to measure investment property at historical cost rather than fair value;

(c) the accounting policy was developed in accordance with AASB 108 in the absence of an Australian Accounting Standard that specifically applies;

(d) the accounting policy relates to an area for which an entity is required to make significant judgements or assumptions in applying an accounting policy, and the entity discloses those judgements or assumptions in accordance with paragraphs 122 and 125; or

(e) the accounting required for them is complex and users of the entity’s financial statements would otherwise not understand those material transactions, other events or conditions—such a situation could arise if an entity applies more than one Australian Accounting Standard to a class of material transactions.

Paragraph 117C

Referred to in paragraphs 88C and 88E of the Practice Statement

Accounting policy information that focuses on how an entity has applied the requirements of the Australian Accounting Standards to its own circumstances provides entity-specific information that is more useful to users of financial statements than standardised information, or information that only duplicates or summarises the requirements of the Standards.

Paragraph 117D

Referred to in paragraphs 88C and 88G of the Practice Statement

If an entity discloses immaterial accounting policy information, such information shall not obscure material accounting policy information.

Paragraph 117E

Referred to in paragraph 88C of the Practice Statement

An entity’s conclusion that accounting policy information is immaterial does not affect the related disclosure requirements set out in other Australian Accounting Standards.

...

Appendix AusCF B

References to the Framework for the Preparation and Presentation of Financial Statements and Australian Accounting Standards

...

Extracts from AASB 101 Presentation of Financial Statements

…

Paragraph 117

Referred to in paragraphs 88A and 88C of the Practice Statement

An entity shall disclose material accounting policy information (see paragraph 7). Accounting policy information is material if, when considered together with other information included in an entity’s financial statements, it can reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements.

Paragraph 117A

Referred to in paragraph 88C of the Practice Statement

Accounting policy information that relates to immaterial transactions, other events or conditions is immaterial and need not be disclosed. Accounting policy information may nevertheless be material because of the nature of the related transactions, other events or conditions, even if the amounts are immaterial. However, not all accounting policy information relating to material transactions, other events or conditions is itself material.

Paragraph 117B

Referred to in paragraphs 88C and 88D of the Practice Statement

Accounting policy information is expected to be material if users of an entity’s financial statements would need it to understand other material information in the financial statements. For example, an entity is likely to consider accounting policy information material to its financial statements if that information relates to material transactions, other events or conditions and:

(a) the entity changed its accounting policy during the reporting period and this change resulted in a material change to the information in the financial statements;

(b) the entity chose the accounting policy from one or more options permitted by Australian Accounting Standards—such a situation could arise if the entity chose to measure investment property at historical cost rather than fair value;

(c) the accounting policy was developed in accordance with AASB 108 in the absence of an Australian Accounting Standard that specifically applies;

(d) the accounting policy relates to an area for which an entity is required to make significant judgements or assumptions in applying an accounting policy, and the entity discloses those judgements or assumptions in accordance with paragraphs 122 and 125; or

(e) the accounting required for them is complex and users of the entity’s financial statements would otherwise not understand those material transactions, other events or conditions—such a situation could arise if an entity applies more than one Australian Accounting Standard to a class of material transactions.

Paragraph 117C

Referred to in paragraphs 88C and 88E of the Practice Statement

Accounting policy information that focuses on how an entity has applied the requirements of the Australian Accounting Standards to its own circumstances provides entity-specific information that is more useful to users of financial statements than standardised information, or information that only duplicates or summarises the requirements of the Standards.

Paragraph 117D

Referred to in paragraphs 88C and 88G of the Practice Statement

If an entity discloses immaterial accounting policy information, such information shall not obscure material accounting policy information.

Paragraph 117E

Referred to in paragraph 88C of the Practice Statement

An entity’s conclusion that accounting policy information is immaterial does not affect the related disclosure requirements set out in other Australian Accounting Standards.

...

For legal purposes, this legislative instrument commences on 31 December 2022.