Tax Agent Services Regulations 2022

I, General the Honourable David Hurley AC DSC (Retd), Governor‑General of the Commonwealth of Australia, acting with the advice of the Federal Executive Council, make the following regulations.

Dated 03 March 2022

David Hurley

Governor‑General

By His Excellency’s Command

Michael Sukkar

Assistant Treasurer, Minister for Housing and Minister for Homelessness, Social and Community Housing

Contents

Part 1—Preliminary

1 Name

2 Commencement

3 Authority

4 Schedules

5 Definitions

Part 2—Recognition of professional associations

Division 1—Purpose of Part

6 Purpose of this Part

Division 2—Recognised BAS agent associations

7 Application for recognition

8 Recognition of association

9 Notice to Board if association ceases to meet requirements

10 Notice if Board requests

11 Termination of recognition

Division 3—Recognised tax agent associations

12 Application for recognition

13 Recognition of association

14 Notice to Board if association ceases to meet requirements

15 Notice if Board requests

16 Termination of recognition

17 Notice of recognition—tax (financial) adviser association

Division 4—Miscellaneous

18 Review of decisions

19 List of recognised associations

Part 3—Registration of BAS agents and tax agents

Division 1—Registered BAS agents

20 Requirements for registration

Division 2—Registered tax agents

21 Requirements for registration

Division 3—Application fees for registration

22 Application fee for registration

Part 4—Investigations

23 Power to require witnesses to attend—allowances and expenses

Part 5—The Tax Practitioners Board

24 Administrative assistance to the Board

25 Register of registered and deregistered tax agents and BAS agents

Part 6—Services that are not tax agent services

26 Specified services that are not tax agent services

Schedule 1—Requirements for recognition of professional associations

Part 1—Recognised BAS agent associations

Part 2—Recognised tax agent associations

Schedule 2—Requirements for registration as a BAS agent or tax agent

Part 1—Registered BAS agents

Part 2—Registered tax agents

Schedule 3—Repeal of the Tax Agent Services Regulations 2009

Tax Agent Services Regulations 2009

Part 1—Preliminary

1 Name

This instrument is the Tax Agent Services Regulations 2022.

2 Commencement

(1) Each provision of this instrument specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information |

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. The whole of this instrument | 1 April 2022. | 1 April 2022 |

Note: This table relates only to the provisions of this instrument as originally made. It will not be amended to deal with any later amendments of this instrument.

(2) Any information in column 3 of the table is not part of this instrument. Information may be inserted in this column, or information in it may be edited, in any published version of this instrument.

3 Authority

This instrument is made under the Tax Agent Services Act 2009.

4 Schedules

Each instrument that is specified in Schedule 3 to this instrument is amended or repealed as set out in the applicable items in that Schedule, and any other item in that Schedule has effect according to its terms.

5 Definitions

Note: A number of expressions included in this instrument are defined in the Act, including the following:

(a) BAS service;

(b) Board;

(c) registered BAS agent;

(d) registered tax agent;

(e) tax agent service.

In this instrument:

Act means the Tax Agent Services Act 2009.

recognised BAS agent association means an association recognised by the Board under section 8.recognised tax agent association means:

(a) an association recognised by the Board under section 13; or

(b) an association that, immediately before 1 January 2022, was a recognised tax (financial) adviser association within the meaning of the Tax Agent Services Regulations 2009 as in force at that time.

Part 2—Recognition of professional associations

Division 1—Purpose of Part

6 Purpose of this Part

For the purposes of section 20‑10 of the Act, this Part provides for a system to allow the Board to accredit professional associations.

Division 2—Recognised BAS agent associations

7 Application for recognition

(1) A not‑for‑profit association may apply to the Board for recognition as a recognised BAS agent association.

(2) The application must:

(a) be in writing; and

(b) be in a form approved by the Board; and

(c) be accompanied by the information (if any) required by the Board.

8 Recognition of association

(1) If an association makes an application in accordance with section 7, the Board must consider the application as soon as practicable and decide:

(a) to recognise the association under subsection (2) or (3) of this section; or

(b) to refuse to recognise the association.

Note: A decision to refuse to recognise an association is a reviewable decision (see section 18).

(2) The Board must recognise the association as a recognised BAS agent association if the Board is satisfied that the association meets the requirements in clauses 101 to 109 of Part 1 of Schedule 1.

(3) The Board may also recognise the association as a recognised BAS agent association if:

(a) the Board is satisfied that the association meets the requirements in clauses 101 to 107 of Part 1 of Schedule 1; and

(b) the Board considers it appropriate to recognise the association having regard to:

(i) the purposes of this instrument and the Act; and

(ii) the role of recognised BAS agent associations.

(4) If the Board recognises the association as a recognised BAS agent association under subsection (2) or (3), the Board must give the association written notice of the decision.

9 Notice to Board if association ceases to meet requirements

(1) This section applies if one or more requirements in clauses 101 to 109 of Part 1 of Schedule 1 are no longer met in relation to an association recognised under subsection 8(2) or 8(3).

(2) The association:

(a) must give the Board notice in writing within 30 days after the association first becomes aware (or ought reasonably to have become aware) that the requirement is no longer met in relation to the association; and

(b) may make a submission in writing to the Board about why the association’s recognition should not be terminated.

10 Notice if Board requests

(1) This section applies if:

(a) a recognised BAS agent association is recognised under subsection 8(3); and

(b) the Board gives the association a written request that the association tell the Board the reasons why it is still appropriate for the association to be recognised under subsection 8(3).

(2) The recognised BAS agent association must:

(a) notify the Board in writing whether, in the association’s view, the recognition is still appropriate having regard to:

(i) the purposes of this instrument and the Act; and

(ii) the role of recognised BAS agent associations; and

(b) give the notice within 30 days of receiving the Board’s request.

11 Termination of recognition

Termination of recognition by the Board

(1) The Board may terminate the recognition of an association that is recognised under subsection 8(2) or 8(3) if:

(a) both of the following apply:

(i) the association is required to give notice in accordance with section 9 or 10;

(ii) the association has not given such notice; or

(b) both of the following apply:

(i) the Board reasonably believes that one or more requirements in clauses 101 to 109 of Part 1 of Schedule 1 are no longer met in relation to the association;

(ii) the Board is not satisfied that it is appropriate for the association to continue to be recognised having regard to the purposes of this instrument and the Act and the role of recognised BAS agent associations.

(2) Before the Board decides to terminate the recognition of an association under subsection (1), the Board must notify the association, in writing, that termination is being considered.

(3) The notice must:

(a) set out the Board’s reasons for considering termination; and

(b) invite the association to make a submission in writing to the Board about the matter; and

(c) specify a reasonable period within which the association may provide the submission.

(4) In considering whether to terminate the association’s recognition under subsection (1), the Board must:

(a) have regard to any submission made by the association under paragraph 9(2)(b) or paragraph (3)(b) of this section; and

(b) make a decision as soon as practicable after the end of the period mentioned in paragraph (3)(c) of this section.

Note: A decision to terminate an association’s recognition is a reviewable decision (see section 18).

(5) If the Board terminates the recognition of an association under subsection (1), the Board must give the association written notice of the decision.

Termination at the request of the association

(6) A recognised BAS agent association may surrender its recognition by notice in writing to the Board.

(7) If the Board receives a notice from an association under subsection (6), the Board must terminate the recognition of the association:

(a) on, or as soon as practicable after, the day the Board receives the notice; or

(b) if a later day is specified in the notice—on that later day.

Division 3—Recognised tax agent associations

12 Application for recognition

(1) A not‑for‑profit association may apply to the Board for recognition as a recognised tax agent association.

(2) The application must:

(a) be in writing; and

(b) be in a form approved by the Board; and

(c) be accompanied by the information (if any) required by the Board.

13 Recognition of association

(1) If an association makes an application in accordance with section 12, the Board must consider the application as soon as practicable and decide:

(a) to recognise the association under subsection (2) or (3) of this section; or

(b) to refuse to recognise the association.

Note: A decision to refuse to recognise an association is a reviewable decision (see section 18).

(2) The Board must recognise the association as a recognised tax agent association if the Board is satisfied that the association meets the requirements in clauses 201 to 210 of Part 2 of Schedule 1.

(3) The Board may also recognise the association as a recognised tax agent association if:

(a) the Board is satisfied that the association meets the requirements in clauses 201 to 208 of Part 2 of Schedule 1; and

(b) the Board considers it appropriate to recognise the association having regard to:

(i) the purposes of this instrument and the Act; and

(ii) the role of recognised tax agent associations.

(4) If the Board recognises the association as a recognised tax agent association under subsection (2) or (3), the Board must give the association written notice of the decision.

14 Notice to Board if association ceases to meet requirements

(1) This section applies if one or more requirements in clauses 201 to 210 of Part 2 of Schedule 1 are no longer met in relation to an association recognised under subsection 13(2) or 13(3).

(2) The association:

(a) must give the Board notice in writing within 30 days after the association first becomes aware (or ought reasonably to have become aware) that the requirement is no longer met in relation to the association; and

(b) may make a submission in writing to the Board about why the association’s recognition should not be terminated.

15 Notice if Board requests

(1) This section applies if:

(a) a recognised tax agent association is recognised under subsection 13(3); and

(b) the Board gives the association a written request that the association tell the Board the reasons why it is still appropriate for the association to be recognised under subsection 13(3).

(2) The recognised tax agent association must:

(a) notify the Board in writing whether, in the association’s view, the recognition is still appropriate having regard to:

(i) the purposes of this instrument and the Act; and

(ii) the role of recognised tax agent associations; and

(b) give the notice within 30 days of receiving the Board’s request.

16 Termination of recognition

Termination of recognition by the Board

(1) The Board may terminate the recognition of an association that is recognised under subsection 13(2) or 13(3) if:

(a) both of the following apply:

(i) the association is required to give notice in accordance with section 14 or 15;

(ii) the association has not given such notice; or

(b) both of the following apply:

(i) the Board reasonably believes that one or more requirements in clauses 201 to 210 of Part 2 of Schedule 1 are no longer met in relation to the association;

(ii) the Board is not satisfied that it is appropriate for the association to continue to be recognised having regard to the purposes of this instrument and the Act and the role of recognised tax agent associations.

(2) Before the Board decides to terminate the recognition of an association under subsection (1), the Board must notify the association, in writing, that termination is being considered.

(3) The notice must:

(a) set out the Board’s reasons for considering termination; and

(b) invite the association to make a submission in writing to the Board about the matter; and

(c) specify a reasonable period within which the association may provide the submission.

(4) In considering whether to terminate the association’s recognition under subsection (1), the Board must:

(a) have regard to any submission made by the association under paragraph 14(2)(b) or paragraph (3)(b) of this section; and

(b) make a decision as soon as practicable after the end of the period mentioned in paragraph (3)(c) of this section.

Note: A decision to terminate an association’s recognition is a reviewable decision (see section 18).

(5) If the Board terminates the recognition of an association under subsection (1), the Board must give the association written notice of the decision.

Termination at the request of the association

(6) A recognised tax agent association may surrender its recognition by notice in writing to the Board.

(7) If the Board receives a notice from an association under subsection (6), the Board must terminate the recognition of the association:

(a) on, or as soon as practicable after, the day the Board receives the notice; or

(b) if a later day is specified in the notice—on that later day.

17 Notice of recognition—tax (financial) adviser association

(1) This section applies if, immediately before 1 January 2022, an association was recognised as a tax (financial) adviser association within the meaning of the Tax Agent Services Regulations 2009.

(2) The Board must publish a notice on its website that on that day the association became a recognised tax agent association because of paragraph (b) of the definition of recognised tax agent association.

Division 4—Miscellaneous

18 Review of decisions

Application may be made to the Administrative Appeals Tribunal for review of any of the following decisions of the Board:

(a) a decision under section 8 to refuse to recognise an association as a recognised BAS agent association;

(b) a decision under section 11 to terminate a recognised BAS agent association’s recognition;

(c) a decision under section 13 to refuse to recognise an association as a recognised tax agent association;

(d) a decision under section 16 to terminate a recognised tax agent association’s recognition.

19 List of recognised associations

The Board must keep and maintain a list of recognised BAS agent associations and recognised tax agent associations on the Board’s website.

Part 3—Registration of BAS agents and tax agents

Division 1—Registered BAS agents

20 Requirements for registration

For the purposes of paragraph 20‑5(1)(b) of the Act, the requirements in respect of registration of an individual as a registered BAS agent are that either or both of clauses 101 or 102 of Part 1 of Schedule 2 applies in relation to the individual.

Note: If the Board grants an application for registration, the Board may impose one or more conditions to which the registration is subject (see subsections 20‑25(5) to (7) of the Act).

Division 2—Registered tax agents

21 Requirements for registration

For the purposes of paragraph 20‑5(1)(b) of the Act, the requirements in respect of registration of an individual as a registered tax agent are that one or more of clauses 201 to 211 of Part 2 of Schedule 2 applies in relation to the individual.

Note: If the Board grants an application for registration, the Board may impose one or more conditions to which the registration is subject (see subsections 20‑25(5) to (7) of the Act).

Division 3—Application fees for registration

22 Application fee for registration

(1) For the purposes of paragraph 20‑20(2)(b) of the Act, the fee for an application of a kind referred to in column 1 of an item of the following table is the fee set out in column 2 of that item.

Application fees |

Item | Column 1 Kind of application | Column 2 Fee |

1 | Application for registration of an individual as a registered tax agent other than where item 2 applies | $704 (subject to indexation under subsection (2)) |

2 | Application for registration of an individual as a registered tax agent in the case where clause 211 of Part 2 of Schedule 2 applies in relation to the individual | Nil |

3 | Application for registration as a BAS agent | $141 (subject to indexation under subsection (2)) |

Annual indexation of fees

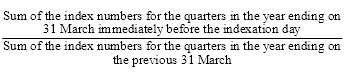

(2) On 1 July 2022 and each 1 July following that day (an indexation day), the dollar amount mentioned in an item of the table in subsection (1) is replaced by the amount worked out using the following formula:

(3) The indexation factor for an indexation day is the number worked out using the following formula:

(3) The indexation factor for an indexation day is the number worked out using the following formula:

where:

index number, for a quarter, means the All Groups Consumer Price Index number (being the weighted average of the 8 capital cities) first published by the Australian Statistician for the quarter.

quarter means a period of 3 months ending on 31 March, 30 June, 30 September or 31 December.

(4) An indexation factor is to be calculated to 3 decimal places (rounding up if the fourth decimal place is 5 or more).

(5) If an indexation factor worked out under subsections (3) and (4) would be less than 1, that indexation factor is to be increased to 1.

(6) Amounts worked out under subsection (2) are to be rounded to the nearest whole dollar (rounding 50 cents upwards).

Part 4—Investigations

23 Power to require witnesses to attend—allowances and expenses

For the purposes of subsections 60‑105(2) and (3) of the Act, the following table sets out the allowances and expenses payable to a person who is required, under subsection 60‑105(1) of the Act, to appear before the Board for the purposes of an investigation.

Item | Persons | Allowances and expenses |

1 | All persons | The amount specified in the High Court Rules 2004 (as in force from time to time) in relation to expenses of witnesses for each hour that the person is required to appear |

2 | A person appearing because of their professional, scientific or other special skill or knowledge | In addition to the amount payable to the person under any other item—an amount that the Board considers reasonable for preparing to give evidence and appearing to give evidence |

3 | A person who has to travel | In addition to the amount payable to the person under any other item—an amount that the Board considers reasonable for the cost of travel |

4 | A person who is required to be absent overnight from their usual place of residence | In addition to the amount payable to the person under any other item—an amount that the Board considers reasonable for the cost of meals and accommodation |

Part 5—The Tax Practitioners Board

24 Administrative assistance to the Board

(1) The Commissioner must:

(a) after consulting the Board, make available to the Board a person:

(i) engaged under the Public Service Act 1999; and

(ii) performing duties in the Australian Taxation Office;

to be the Secretary of the Board; and

(b) make available to the Board persons:

(i) engaged under the Public Service Act 1999; and

(ii) performing duties in the Australian Taxation Office;

to provide administrative assistance to the Board; and

(c) determine the number of persons having regard to:

(i) the number of persons who would be required to enable the Board to perform its functions and exercise its powers under the Act; and

(ii) the funding that has been allocated, as agreed between the Commissioner and the Board, for the purpose of allowing the Board to perform its functions and exercise its powers under the Act.

(2) The Secretary of the Board must:

(a) attend all meetings of the Board; and

(b) keep a record of the proceedings of the Board.

25 Register of registered and deregistered tax agents and BAS agents

Registered entities

(1) For the purposes of subsection 60‑135(2) of the Act, the register established under subsection 60‑135(1) of the Act must include the following information for each entity that is a registered tax agent or registered BAS agent:

(a) the name of the entity;

(b) the contact details of the entity;

(c) any relevant professional affiliation of the entity;

(d) the duration of the registration of the entity;

(e) any condition to which the registration of the entity;

(f) any sanction (other than a caution or termination) that has been imposed by the Board on the entity.

Note: Subsection (3) explains the information that must be placed on the register of entities in relation to the termination of the registration of a registered tax agent or registered BAS agent.

(2) Information on the register that relates to a sanction (other than a caution or termination) that has been imposed by the Board on a registered tax agent or registered BAS agent must be kept on the register for the longer of:

(a) 12 months starting on the day on which the sanction is imposed; or

(b) the period during which the sanction has effect.

Terminated entities

(3) For the purposes of subsection 60‑135(2) of the Act, the register must include the following information for each entity whose registration as a registered tax agent or a registered BAS agent has been terminated:

(a) the name of the entity;

(b) the contact details of the entity;

(c) the date of effect of the termination of the entity’s registration;

(d) the reason for the termination of the entity’s registration.

Other information

(4) The register may include other information that is relevant to the operation of the arrangements for the registration of tax agents and BAS agents.

Part 6—Services that are not tax agent services

26 Specified services that are not tax agent services

(1) For the purposes of subsection 90‑5(2) of the Act, the following services are specified:

(a) a service provided by an auditor of a self managed superannuation fund under the Superannuation Industry (Supervision) Act 1993;

(b) a service provided by an entity to a related entity;

(c) a service provided by a related entity of an entity (the first entity) to another related entity of the first entity;

(d) a service provided by a trustee of a trust (or a related entity of the trustee) to the trust, or a member of the trust, in relation to the trust;

(e) a service provided by a trustee of a trust (or a related entity of the trustee) to a wholly owned or controlled entity of the trust in relation to the entity;

(f) a service provided by a responsible entity (within the meaning of the Corporations Act 2001) of a managed investment scheme (within the meaning of that Act) (or a related entity of the responsible entity, the manager of the managed investment scheme or the operator of the managed investment scheme) to the scheme, or a member of the scheme, in relation to the scheme;

(g) a service provided by an operator (within the meaning of the Corporations Act 2001) of a notified foreign passport fund (within the meaning of that Act) or a related entity of the operator to the fund, or a member of the fund, in relation to the fund;

(h) a service provided by a partner in a partnership (or a related entity of the partner) to another partner of the partnership in relation to the partnership;

(i) a service provided by a member of a joint venture (or a related entity of the member) to another member of the joint venture or an entity established to pursue the joint venture:

(i) in accordance with a written agreement; and

(ii) in relation to the joint venture;

(j) a service that is a custodial or depository service (within the meaning of the Corporations Act 2001) provided by a financial services licensee (within the meaning of that Act) or an authorised representative (within the meaning of section 761A of that Act) of the licensee;

(k) a service provided by an entity (the first entity) to an entity previously owned by the first entity (the second entity) in relation to the second entity’s obligations under a taxation law for the income year in which it was sold by the first entity;

(l) a service that is required, by a law of the Commonwealth or of a State or Territory, to be provided only by an actuary (within the meaning of the Income Tax Assessment Act 1997);

(m) a service provided by an actuary (within the meaning of the Income Tax Assessment Act 1997) in relation to either or both of the following:

(i) a defined benefit superannuation scheme (within the meaning of the Superannuation Guarantee (Administration) Act 1992);

(ii) an allocation from a reserve in a superannuation scheme (within the meaning of the Superannuation Guarantee (Administration) Act 1992) other than a defined benefit superannuation scheme (within the meaning of that Act);

(n) subject to subsection (2), a tax (financial) advice service provided between 1 January and 31 December 2022 by an entity that:

(i) immediately before 1 January 2022, was a registered tax (financial) adviser (within the meaning of the Act as in force at that time); and

(ii) is not a relevant provider (within the meaning of section 910A of the Corporations Act 2001).

(2) Paragraph (1)(n) does not cover a service provided by an entity if:

(a) on or after 1 January 2022, the entity applies, under section 20‑20 of the Act, for registration as a tax agent; and

(b) the service is provided:

(i) if the Board grants the application—after the registration commences; or

(ii) if the Board rejects the application—after the Board notifies the entity of its decision.

(3) In this section:

Note: The terms under common ownership, stapled entity and taxation law have the same meaning as in the Income Tax Assessment Act 1997 (see subsection 90‑1(2) of the Tax Agent Services Act 2009).

related entity, in relation to an entity, means:

(a) an associated entity (within the meaning of the Corporations Act 2001) of the entity; or

(b) an entity under common ownership with the entity; or

(c) a stapled entity of the entity or an associated entity of the stapled entity; or

(d) an entity connected with the entity (within the meaning of section 328‑125 of the Income Tax Assessment Act 1997, applied as if references in that section to a control percentage of 40% were references to a control percentage of 50%).

Schedule 1—Requirements for recognition of professional associations

Note: See sections 8 and 13.

Part 1—Recognised BAS agent associations

101 The association is a non‑profit association.

102 The association has adequate corporate governance and operational procedures to ensure that:

(a) it is properly managed; and

(b) its internal rules are enforced.

103 The association has professional and ethical standards for its voting members, including terms to the effect that:

(a) voting members must undertake at least 15 hours of continuing professional education each year; and

(b) voting members must be of good fame, integrity and character; and

(c) each voting member is subject to rules controlling the member’s conduct in the practice of the member’s profession; and

(d) each voting member is subject to discipline for breaches of those rules; and

(e) if a voting member is permitted by that association to be in public practice, the voting member has professional indemnity insurance.

104 The association has satisfactory arrangements in place for:

(a) notifying clients of its members, or of members of its member bodies, about how to make complaints; and

(b) receiving, hearing and deciding those complaints; and

(c) taking disciplinary action if complaints are justified.

105 The association has satisfactory arrangements in place for publishing annual statistics about:

(a) the kinds and number of complaints made to the association; and

(b) findings made as a result of the complaints; and

(c) action taken as a result of those findings.

106 The association is able to pay its debts as they fall due.

107 The management of the association:

(a) is required to be accountable to its members; and

(b) is required to abide by the corporate governance and operational procedures of the association.

108 The association has at least 1000 voting members, of whom at least 500 are registered BAS agents.

Note: The term registered BAS agent is defined in the Act.

109 Each voting member of the association has been awarded a Certificate IV in Accounting and Bookkeeping (or a Certificate IV Bookkeeping or Certificate IV Accounting), or a higher qualification in bookkeeping or accounting, from:

(a) a registered training organisation; or

(b) an equivalent institution.

Part 2—Recognised tax agent associations

201 The association is a non‑profit association.

202 The association has adequate corporate governance and operational procedures to ensure that:

(a) it is properly managed; and

(b) its internal rules are enforced.

203 The association has satisfactory arrangements for ensuring appropriate professional and ethical requirements standards for its voting members, including:

(a) voting members must undertake an appropriate number of hours of continuing professional education each year; and

(b) voting members must be of good fame, integrity and character; and

(c) each voting member is subject to rules controlling the member’s conduct in the practice of the member’s profession; and

(d) each voting member is subject to discipline for breaches of those rules; and

(e) if a voting member is permitted by the association to be in public practice, the voting member has professional indemnity insurance.

204 The association has satisfactory arrangements for dealing with complaints, including:

(a) notifying clients of its members, or of members of its member bodies, about how to make complaints; and

(b) receiving, hearing and deciding those complaints; and

(c) taking disciplinary action if complaints are justified.

205 The association has satisfactory arrangements for publishing annual statistics about:

(a) the kinds and number of complaints made to the association; and

(b) findings made as a result of the complaints; and

(c) action taken as a result of those findings.

206 The association is able to pay its debts as they fall due.

207 The management of the association:

(a) is required to be accountable to its members; and

(b) is required to abide by the corporate governance and operational procedures of the association.

208 An association is taken to have arrangements that comply with a requirement mentioned in clause 203, 204 or 205 if:

(a) a law of a State or Territory that has the same, or substantially the same, effect as the requirement in that paragraph applies in relation to the association or its members (as the case may be); and

(b) the association or its members (as the case may be) complies with that law.

209 The association has at least 1000 voting members, of whom at least 500 are registered tax agents.

Note: The term registered tax agent is defined in the Act.

210 At least one of the following applies in relation to each voting member of the association:

(a) the member has been awarded a degree or a post‑graduate award in a relevant discipline (within the meaning of Part 2 of Schedule 2) from:

(i) an Australian tertiary education institution; or

(ii) an equivalent institution;

(b) the member has been awarded a diploma or higher award in a relevant discipline (within the meaning of Part 2 of Schedule 2) from:

(i) a registered training organisation; or

(ii) an equivalent institution;

(c) the member has the academic qualifications required to be an Australian legal practitioner;

(d) the member has at least 8 years of full time experience (or part time equivalent) in providing tax agent services in the last 10 years;

(e) the member has at least 6 years of full time experience (or part time equivalent) in providing tax (financial) advice services in the last 8 years.

Note: The terms tax agent service and tax (financial) advice service are defined in the Act.

Schedule 2—Requirements for registration as a BAS agent or tax agent

Note: See sections 20 and 21.

Part 1—Registered BAS agents

Accounting qualifications

101 This clause applies if the individual:

(a) has been awarded a Certificate IV in Accounting and Bookkeeping (or a Certificate IV Bookkeeping or Certificate IV Accounting), or a higher qualification in bookkeeping or accounting, from a registered training organisation or an equivalent institution; and

(b) has successfully completed a course in basic GST/BAS taxation principles that is approved by the Board; and

(c) has undertaken at least 1400 hours of relevant experience in the last 4 years.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: For the definition of relevant experience, see clause 103 of this Part.

Professional association membership

102 This clause applies if the individual:

(a) is a voting member of a recognised BAS agent association or a recognised tax agent association; and

(b) has been awarded a Certificate IV in Accounting and Bookkeeping (or a Certificate IV Bookkeeping or Certificate IV Accounting), or a higher qualification in bookkeeping or accounting, from a registered training organisation or an equivalent institution; and

(c) has successfully completed a course in basic GST/BAS taxation principles that is approved by the Board; and

(d) has undertaken at least 1000 hours of relevant experience in the last 4 years.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: For the definitions of recognised BAS agent association and recognised tax agent association, see section 5. For the definition of relevant experience, see clause 103 of this Part.

Definitions

103 In this Part:

relevant experience means work by an individual:

(a) as a registered tax agent or a registered BAS agent; or

(b) under the supervision and control of a registered tax agent or a registered BAS agent; or

(c) of another kind approved by the Board;

that includes substantial involvement in the provision of one or more of the types of BAS services described in section 90‑10 of the Act.

Note: The terms registered BAS agent and registered tax agent are defined in the Act.

Part 2—Registered tax agents

Tertiary qualifications—accounting

201 This clause applies if the individual:

(a) has been awarded either:

(i) a degree, or a post graduate award, in accounting from an Australian tertiary education institution; or

(ii) a degree, or an award, in accounting that is approved by the Board, and that is from an equivalent institution; and

(b) has successfully completed a course in commercial law that is approved by the Board; and

(c) has successfully completed a course in Australian taxation law that is approved by the Board; and

(d) has undertaken at least 1 year of full time relevant experience (or part time equivalent) in the last 5 years.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: For the definition of relevant experience, see clause 212 of this Part.

Tertiary qualifications—specialists

202 This clause applies if the individual:

(a) has been awarded either:

(i) a degree, or a post graduate award, in an area (other than accounting) that is relevant to the tax agent service to which the individual’s application for registration relates from an Australian tertiary education institution; or

(ii) a degree, or an award, in an area (other than accounting) that is approved by the board, relevant to the tax agent service to which the individual’s application for registration relates, and that is from an equivalent institution; and

(b) if the Board considers it relevant to the tax agent service to which the individual’s application for registration relates—has successfully completed as many of the following courses as the Board considers necessary:

(i) a course in basic accounting principles that is approved by the Board;

(ii) a course in commercial law that is approved by the Board;

(iii) a course in Australian taxation law that is approved by the Board; and

(c) has undertaken at least 1 year of full time relevant experience (or part time equivalent) in the last 5 years.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: The term tax agent service is defined in the Act. For the definition of relevant experience, see clause 212 of this Part.

Diploma or higher award

203 This clause applies if the individual:

(a) has been awarded a diploma or higher award in accounting from a registered training organisation or an equivalent institution; and

(b) has successfully completed a course in Australian taxation law that is approved by the Board; and

(c) has successfully completed a course in commercial law that is approved by the Board; and

(d) has undertaken at least 2 years of full time relevant experience (or part time equivalent) in the last 5 years.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: For the definition of relevant experience, see clause 212 of this Part.

Tertiary qualifications—law

204 This clause applies if the individual:

(a) has the academic qualifications required to be an Australian legal practitioner; and

(b) has successfully completed a course in basic accounting principles that is approved by the Board; and

(c) has successfully completed a course in Australian taxation law that is approved by the Board; and

(d) has undertaken at least 1 year of full time relevant experience (or part time equivalent) in the last 5 years.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: For the definition of relevant experience, see clause 212 of this Part.

Work experience

205 This clause applies if the individual:

(a) has successfully completed a course in basic accounting principles that is approved by the Board; and

(b) has successfully completed a course in Australian taxation law that is approved by the Board; and

(c) has successfully completed a course in commercial law that is approved by the Board; and

(d) has undertaken at least 8 years of full time relevant experience (or part time equivalent) in the last 10 years.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: For the definition of relevant experience, see clause 212 of this Part.

Membership of professional association

206 This clause applies if the individual:

(a) is a voting member of a recognised tax agent association; and

(b) has undertaken at least 8 years of full time relevant experience (or part time equivalent) in the last 10 years.

Note: For the definition of recognised tax agent association, see section 5. For the definition of relevant experience, see clause 212 of this Part.

Tertiary qualifications—financial services licensees and their representatives

207 This clause applies if the individual:

(a) has been awarded either:

(i) a degree, or a post‑graduate award, in a relevant discipline, from an Australian tertiary education institution; or

(ii) a degree, or an award, in a relevant discipline that is approved by the Board, and that is from an equivalent institution; and

(b) has successfully completed a course in commercial law that is approved by the Board; and

(c) has successfully completed a course in Australian taxation law that is approved by the Board; and

(d) has undertaken at least 1 year of full time relevant tax (financial) advice experience (or part time equivalent) in the last 5 years; and

(e) is, or was within the last 90 days:

(i) a financial services licensee within the meaning of Chapter 7 of the Corporations Act 2001; or

(ii) a representative of a financial services licensee mentioned in paragraph (a) of the definition of representative in section 910A of the Corporations Act 2001.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: For the definitions of relevant discipline and relevant tax (financial) advice experience, see clause 212 of this Part.

Diploma or higher award—financial services licensees and their representatives

208 This clause applies if the individual:

(a) has been awarded a diploma, or higher award, in a relevant discipline, from a registered training organisation or an equivalent institution; and

(b) has successfully completed a course in commercial law that is approved by the Board; and

(c) has successfully completed a course in Australian taxation law that is approved by the Board; and

(d) has undertaken at least 18 months of full time relevant tax (financial) advice experience (or part time equivalent) in the last 5 years; and

(e) is, or was within the last 90 days:

(i) a financial services licensee within the meaning of Chapter 7 of the Corporations Act 2001; or

(ii) a representative of a financial services licensee mentioned in paragraph (a) of the definition of representative in section 910A of the Corporations Act 2001.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: For the definitions of relevant discipline and relevant tax (financial) advice experience, see clause 212 of this Part.

Work experience—financial services licensees and their representatives

209 This clause applies if the individual:

(a) has successfully completed a course in commercial law that is approved by the Board; and

(b) has successfully completed a course in Australian taxation law that is approved by the Board; and

(c) has undertaken at least 3 years of full time relevant tax (financial) advice experience (or part time equivalent) in the last 5 years; and

(d) is, or was within the last 90 days:

(i) a financial services licensee within the meaning of Chapter 7 of the Corporations Act 2001; or

(ii) a representative of a financial services licensee mentioned in paragraph (a) of the definition of representative in section 910A of the Corporations Act 2001.

Note 1: The Board may approve a course by an approval process, an accreditation scheme, or by other means.

Note 2: For the definition of relevant tax (financial) advice experience, see clause 212 of this Part.

Membership of professional associations—financial services licensees and their representatives

210 This clause applies if the individual:

(a) is a voting member of a recognised tax agent association; and

(b) has undertaken at least 6 years of full time relevant tax (financial) advice experience (or part time equivalent) in the last 8 years; and

(c) is, or was within the last 90 days:

(i) a financial services licensee within the meaning of Chapter 7 of the Corporations Act 2001; or

(ii) a representative of a financial services licensee mentioned in paragraph (a) of the definition of representative in section 910A of the Corporations Act 2001.

Registered tax (financial) advisers

211 This clause applies if:

(a) immediately before 1 January 2022, the individual was a registered tax (financial) adviser within the meaning of the Act as in force at that time; and

(b) the individual’s application for registration, under section 20‑20 of the Act, is made before 1 January 2023.

Definitions

212 In this Part:

relevant discipline includes a discipline related to finance, financial planning, commerce, economics, business, tax, accounting, or law.

relevant experience means work by an individual:

(a) as a registered tax agent; or

(b) as a tax agent registered under Part VIIA of the Income Tax Assessment Act 1936 as in force immediately before 1 March 2010; or

(c) under the supervision and control of a registered tax agent; or

(d) under the supervision and control of a tax agent registered under Part VIIA of the Income Tax Assessment Act 1936 as in force immediately before 1 March 2010; or

(e) as an Australian legal practitioner; or

(f) of another kind approved by the Board;

that includes substantial involvement in the provision of one or more of the types of tax agent services described in section 90‑5 of the Act, or substantial involvement in the practice of a particular area of taxation law to which one or more of those types of tax agent services relate.

Note: The terms registered tax agent and tax agent service are defined in the Act.

relevant tax (financial) advice experience means work by an individual:

(a) as a registered tax (financial) adviser within the meaning of the Act as in force immediately before 1 January 2022; or

(b) as a registered tax agent, or a tax agent registered under Part VIIA of the Income Tax Assessment Act 1936 as in force immediately before 1 March 2010; or

(c) under the supervision and control of a registered tax (financial) adviser within the meaning of the Act as in force immediately before 1 January 2022; or

(d) under the supervision and control of a registered tax agent or a tax agent registered under Part VIIA of the Income Tax Assessment Act 1936 as in force immediately before 1 March 2010; or

(e) as a qualified tax relevant provider; or

(f) under the supervision and control of a qualified tax relevant provider; or

(g) of another kind approved by the Board;

that includes substantial involvement in the provision of one or more of the types of tax (financial) advice services described in section 90‑15 of the Act, or substantial involvement in the practice of a particular area of taxation law to which one or more of those types of tax (financial) advice services relate.

Note: The terms registered tax agent and tax (financial) advice service are defined in the Act.