Taxation (Multinational—Global and Domestic Minimum Tax) Rules 2024

I, Dr Jim Chalmers, Treasurer, make the following rules.

Dated 18 December 2024

Dr Jim Chalmers

Treasurer

Taxation (Multinational—Global and Domestic Minimum Tax) Rules 2024

I, Dr Jim Chalmers, Treasurer, make the following rules.

Dated 18 December 2024

Dr Jim Chalmers

Treasurer

Contents

Chapter 1—Preliminary etc

Part 1‑1—Preliminary

1‑5 Name

1‑10 Commencement

1‑15 Authority

Part 1‑2—Excluded Entities

1‑20 Excluded Entities

Part 1‑3—Currency conversion

1‑25 Foreign currency translation—general

Chapter 2—Liability amounts

Part 2‑1—Application of the IIR

2‑5 Meaning of IIR Top‑up Tax Amount

Part 2‑2—Allocation of Top‑up Tax under the IIR

2‑10 Meaning of Allocable Share

2‑15 Meaning of Inclusion Ratio

Part 2‑3—IIR offset mechanism

2‑20 IIR offset mechanism

Part 2‑4—Domestic Top‑up Tax Amount

2‑25 Meaning of Domestic Top‑up Tax Amount

2‑30 Amount of Domestic Top‑up Tax Amount

2‑35 Computing Top‑up Tax for the purposes of section 2‑30—principles

2‑40 Domestic Top‑up Tax Amount—special rule for consolidated groups

Part 2‑5—UTPR Top‑up Tax Amount

2‑45 Meaning of UTPR Top‑up Tax Amount

2‑50 UTPR Top‑up Tax Amount—special rule for consolidated groups

2‑55 Meaning of Total UTPR Top‑up Tax Amount

Part 2‑6—Allocation of Top‑Up Tax for the UTPR

2‑60 Allocation of Total UTPR Top‑Up Tax Amount to Australia

2‑65 Meaning of UTPR Percentage

2‑70 Distribution of allocated Total UTPR Top‑Up Tax Amount to Australian Constituent Entity

2‑75 Number of employees in a jurisdiction

2‑80 Meaning of Net Book Value of Tangible Assets

2‑85 Employees and the Net Book Value of Tangible Assets of Investment Entities and Securitisation Entities to be disregarded

2‑90 Employees and the Net Book Value of Tangible Assets allocated to Permanent Establishment

2‑95 Employees and the Net Book Value of Tangible Assets allocated from Flow‑through Entity

Chapter 3—Computation of GloBE Income or Loss

Part 3‑1—Financial accounts

3‑5 Meaning of GloBE Income or Loss

3‑10 Meaning of Financial Accounting Net Income or Loss

Part 3‑2—Adjustments to determine GloBE Income or Loss

Division 1—Article 3.2.1 adjustments

3‑15 Adjustment—net taxes expense

3‑20 Adjustment—Excluded Dividends

3‑25 Meaning of Excluded Dividends, Short‑term Portfolio Shareholding and Portfolio Shareholding

3‑30 Adjustment—Excluded Equity Gain or Loss

3‑35 Meaning of Excluded Equity Gain or Loss

3‑40 Adjustment—insurance reserves

3‑45 Adjustment—Included Revaluation Method Gain or Loss

3‑50 Meaning of Included Revaluation Method Gain or Loss and Other Comprehensive Income

3‑55 Adjustment—asymmetric foreign currency gains or losses

3‑60 Meaning of tax functional currency and accounting functional currency

3‑65 Adjustment—policy disallowed expenses

3‑70 Adjustment—prior period errors and changes in accounting principles

3‑75 Adjustment—accrued pension expense

3‑80 Adjustment—qualified debt release amount

3‑85 Meaning of qualified debt release amount

Division 2—Other Article 3.2 adjustments

3‑90 Adjustment—stock‑based compensation expense

3‑95 Adjustment—Arm’s Length Principle and tax/accounting permanent differences in respect of cross‑border transactions

3‑100 Adjustment—Arm’s Length Principle and transactions between Constituent Entities located in the same jurisdiction

3‑105 Meaning of Arm’s Length Principle

3‑110 Adjustment—Refundable Tax Credits and transferable tax credits

3‑115 Qualified Refundable Tax Credits—amounts

3‑120 Marketable Transferable Tax Credits—amounts

3‑125 Meaning of Qualified Refundable Tax Credit, Non‑Qualified Refundable Tax Credit and Refundable Tax Credit

3‑130 Meaning of Marketable Transferable Tax Credit

3‑135 Meaning of Marketable Price Floor

3‑140 Meaning of Non‑Marketable Transferable Tax Credit and Other Tax Credit

3‑145 Adjustment—loss on transfer of purchased Non‑Marketable Transferable Tax Credits

3‑150 Adjustment—assets and liabilities that are subject to fair value or impairment accounting

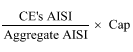

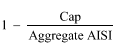

3‑155 Adjustment—Aggregate Asset Gain—election

3‑160 Adjustment—Aggregate Asset Gain—effect

3‑165 Adjustment—Aggregate Asset Gain—allocation of amounts

3‑170 Meaning of Aggregate Asset Gain, Net Asset Gain, etc

3‑175 Meaning of Look‑back Period and Loss Year

3‑180 Adjustment—Intragroup Financing Arrangements

3‑185 Meaning of Intragroup Financing Arrangement

3‑190 Meaning of Low‑Tax Entity and High‑Tax Counterparty

3‑195 Meaning of Low‑Tax Jurisdiction

3‑200 Adjustment—election to apply consolidated accounting treatment

3‑205 Adjustment—insurance company amounts charged to policyholders for taxes paid in respect of returns to policy holders

3‑210 Adjustment—distributions paid or payable in respect of Additional Tier One Capital or Restricted Tier One Capital

3‑215 Adjustments as necessary for Chapters 6 and 7

Part 3‑3—International Shipping Income exclusion

3‑220 Adjustment—certain shipping income

3‑225 Meaning of International Shipping Income, etc.

3‑230 Meaning of Qualified Ancillary International Shipping Income, etc.

3‑235 International traffic

Part 3‑4—Allocation of income or loss between a Main Entity and a Permanent Establishment

3‑240 Meaning of Financial Accounting Net Income or Loss—Permanent Establishment

3‑245 Adjustment of Permanent Establishment’s Financial Accounting Net Income or Loss

3‑250 Computing GloBE Income or Loss of the Main Entity in respect of a Permanent Establishment

Part 3‑5—Allocation of income or loss from a Flow‑through Entity

3‑255 Constituent Entity that is a Flow‑through Entity—Financial Accounting Net Income or Loss

Chapter 4—Computation of Adjusted Covered Taxes

Part 4‑1—Adjusted Covered Taxes

4‑5 Meaning of Adjusted Covered Taxes

4‑10 Meaning of Accrued Current Covered Tax Expense

4‑15 Meaning of Additions to Covered Taxes

4‑20 Meaning of Reductions to Covered Taxes

4‑25 No double counting of Covered Taxes

4‑30 Additional Current Top‑up Tax where MNE Group has no Net GloBE Income and tax falls short of expected tax

4‑35 Additional Current Top‑up Tax under section 4‑30—Excess Negative Tax Expense Carry‑forward

Part 4‑2—Definition of Covered Taxes

4‑40 Meaning of Covered Taxes

Part 4‑3—Allocation of Covered Taxes from one Constituent Entity to another Constituent Entity

4‑45 Allocation of amounts from Constituent Entity to Permanent Establishment—general rule

4‑50 Allocation of amounts from Tax Transparent Entity to a Constituent Entity‑owner of the Tax Transparent Entity

4‑55 Allocation of amounts from Constituent Entity‑owner to CFC

4‑60 Meaning of Blended CFC Tax Regime

4‑65 Allocation of amounts from Constituent Entity‑owner to Hybrid Entity or Reverse Hybrid Entity

4‑70 Amounts accrued in financial accounts of Constituent Entity‑owner on distribution from Constituent Entity to Constituent Entity‑owner—allocation to Constituent Entity

4‑75 Allocation of amounts in respect of Passive Income—inclusion in Constituent Entity’s Adjusted Covered Taxes

4‑80 Allocation of amounts from Permanent Establishment to Main Entity

Part 4‑4—Mechanism to address temporary differences

4‑85 Meaning of Total Deferred Tax Adjustment Amount

4‑90 Total Deferred Tax Adjustment Amount—effect of Substitute Loss Carry‑forward DTA

4‑95 Meaning of Substitute Loss Carry‑forward DTA

4‑100 Effect of Recaptured Deferred Tax Liability

4‑105 Meaning of Recaptured Deferred Tax Liability

4‑110 Meaning of Recapture Exception Accrual

4‑115 Meaning of Disallowed Accrual and Unclaimed Accrual

Part 4‑5—The GloBE Loss Election

4‑120 GloBE Loss Election

4‑125 GloBE Loss Deferred Tax Asset of an MNE Group

4‑130 GloBE Loss Election for an Ultimate Parent Entity

4‑135 GloBE Loss Deferred Tax Asset of an Ultimate Parent Entity

Part 4‑6—Post‑filing adjustments and tax rate changes

4‑140 Effect of adjustment to the liability for Covered Taxes

4‑145 Tax rate changes and unpaid current tax expense

Chapter 5—Computation of Effective Tax Rate

Part 5‑1—Determination of Effective Tax Rate

5‑5 Meaning of Effective Tax Rate

5‑10 Effective Tax Rate—Excess Negative Tax Expense administrative procedure

5‑15 Meaning of Net GloBE Income and Net GloBE Loss

Part 5‑2—Top‑up Tax

5‑20 Meaning of Top‑up Tax Percentage

5‑25 Meaning of Excess Profit

5‑30 Meaning of Jurisdictional Top‑up Tax

5‑35 Certain amounts of Domestic Top‑up Tax disregarded

5‑40 Top‑up Tax of a Constituent Entity

5‑45 Treatment of Stateless Constituent Entities

Part 5‑3—Substance‑based Income Exclusion

5‑50 Substance‑based Income Exclusion Amount

5‑55 Payroll Carve‑out Amount

5‑60 Meaning of Eligible Payroll Costs and Eligible Employee

5‑65 Tangible Asset Carve‑out Amount

5‑70 Operating leases and intragroup finance leases

5‑75 Meaning of Eligible Tangible Asset

5‑80 Allocation of amounts between a Main Entity and a Permanent Establishment

5‑85 Allocation of amounts in relation to Flow‑through Entities

5‑90 Allocation of amounts in relation to Deductible Dividend Regimes

Part 5‑4—Additional Current Top‑up Tax

5‑95 Additional Current Top‑up Tax—ETR Adjustment Provisions

5‑100 Additional Current Top‑up Tax—Adjusted Covered Taxes less than expected amount

Part 5‑5—De minimis exclusion

5‑105 De minimis exclusion

5‑110 Meaning of Average GloBE Revenue etc.

5‑115 Recalculations under an ETR Adjustment Provision

Part 5‑6—Minority‑Owned Constituent Entities

5‑120 Minority‑Owned Constituent Entities that comprise a Minority‑Owned Subgroup

5‑125 Minority‑Owned Constituent Entities that are not part of a Minority‑Owned Subgroup

5‑130 Meaning of Minority‑Owned Constituent Entity and Minority‑Owned Parent Entity

5‑135 Meaning of Minority‑Owned Subsidiary and Minority‑Owned Subgroup

Chapter 6—Corporate restructurings and holding structures

Part 6‑1—Application of consolidated revenue threshold to Group mergers and demergers

6‑5 Applicable MNE Groups—mergers

6‑10 Applicable MNE Groups—demergers

Part 6‑2—Constituent Entities joining and leaving an MNE Group

Division 1—Transfers of Ownership Interests

6‑15 Application of this Division

6‑20 Target’s assets etc. included in MNE Group’s Consolidated Financial Statements

6‑25 Target’s Financial Accounting Net Income or Loss and Adjusted Covered Taxes

6‑30 Historical carrying value of target’s assets and liabilities

6‑35 Target’s Eligible Payroll Costs and Tangible Asset Carve‑out Amount

6‑40 Deferred tax assets and deferred tax liabilities

6‑45 Target’s Top‑up Tax if Parent Entity in 2 or more MNE Groups

Division 2—Transfer of Ownership Interests treated as transfer of assets and liabilities

6‑50 Transfer of Ownership Interests treated as transfer of assets and liabilities

Part 6‑3—Transfer of assets and liabilities

6‑55 Acquisitions and disposals of assets and liabilities

6‑60 GloBE Reorganisations

6‑65 Meaning of GloBE Reorganisation and Non‑qualifying Gain or Loss

6‑70 Fair value adjustments

Part 6‑4—Joint Ventures

6‑75 Joint Ventures

Part 6‑5—Multi‑Parented MNE Groups

6‑80 Multi‑Parented MNE Groups

6‑85 Meaning of Multi‑Parented MNE Group etc.

Chapter 7—Tax neutrality and distribution regimes

Part 7‑1—Ultimate Parent Entity that is a Flow‑through Entity

7‑5 Flow‑through Entity that is Ultimate Parent Entity—reduce GloBE Income and Covered Taxes

7‑10 Flow‑through Entity that is Ultimate Parent Entity—reduce GloBE Loss

7‑15 Application of sections 7‑5 and 7‑10 to Permanent Establishment

Part 7‑2—Ultimate Parent Entity subject to Deductible Dividend Regime

7‑20 Ultimate Parent Entity subject to Deductible Dividend Regime—reduce GloBE Income and Covered Taxes

7‑25 Ultimate Parent Entity subject to Deductible Dividend Regime—reduce GloBE Income and Covered Taxes of other Constituent Entities

7‑30 Meaning of Deductible Dividend Regime

7‑35 Meaning of Deductible Dividend

Part 7‑3—Eligible Distribution Tax Systems

7‑40 Deemed distribution tax election

7‑45 Meaning of Eligible Distribution Tax System

7‑50 Effect of election—amount in respect of deemed distribution tax added to Adjusted Covered Taxes

7‑55 Deemed Distribution Tax Recapture Account

7‑60 Recapture Account Loss Carry‑forward

7‑65 Effect of positive balance of Deemed Distribution Tax Recapture Account after 4 Fiscal Years—reduce Adjusted Covered Taxes for original year

7‑70 Distribution taxes excluded in Adjusted Covered Taxes

7‑75 Effect of Constituent Entity leaving jurisdiction, etc.

Part 7‑4—Effective Tax Rate computation for Investment Entities

Division 1—Application

7‑80 Application of this Part

7‑85 Insurance Investment Entity treated as Investment Entity

7‑90 Computing GloBE Income or Loss of Investment Entity

Division 2—Allocable Share of Top‑up Tax of Investment Entity

7‑95 Allocable Share of Top‑up Tax of Investment Entity

Division 3—Top‑up Tax of Investment Entity etc.

7‑100 Top‑up Tax etc. of Investment Entity—primary deeming rule

7‑105 Computing Jurisdictional Top‑up Tax for the purposes of computing Top‑up Tax of Investment Entity

7‑110 Meaning of Allocable GloBE Income or Loss

Division 4—Top‑up Tax of non‑Investment Entity

7‑115 Top‑up Tax of Constituent Entity that is not Investment Entity

Part 7‑5—Investment Entity tax transparency election

7‑120 Application of this Part

7‑125 Investment Entity tax transparency election

7‑130 Effect of election—Investment Entity treated as Tax Transparent Entity

7‑135 Effect of revocation of election—Investment Entity treated as Tax Transparent Entity

Part 7‑6—Taxable distribution method election

7‑140 Application of this Part

7‑145 Taxable distribution method election

7‑150 Effect of election—distributions and deemed distributions received by Constituent Entity‑owner included in computing its GloBE Income, etc.

7‑155 Effect of election—where positive balance of Undistributed Net GloBE Income Account after 3 Fiscal Years, increase Top‑up Tax for tested year

7‑160 Meaning of Undistributed Net GloBE Income Account

7‑165 Deemed distributions

7‑170 Effect of revoking election

Chapter 8—Administration

Part 8‑2—Safe harbours

Division 1—Preliminary

8‑5 Application of this Part to Minority‑Owned Constituent Entities, Joint Ventures and Investment Entities

Division 2—Transitional CbCR Safe Harbour

Subdivision A—Transitional CbCR Safe Harbour

8‑10 Transitional CbCR Safe Harbour—general rule

8‑15 Meaning of Transition Period

Subdivision B—De minimis test

8‑20 Meeting the De minimis test

8‑25 Meaning of Total Revenue of MNE Group

8‑30 Meaning of Profit (Loss) before Income Tax

8‑35 Meaning of Qualified CbC Report

Subdivision C—Simplified ETR test

8‑40 Meeting the Simplified ETR test

8‑45 Meaning of Simplified ETR

8‑50 Meaning of Simplified Covered Taxes

8‑55 Meaning of Transition Rate

Subdivision D—Routine profits test

8‑60 Meeting the Routine profits test

8‑65 Meaning of CbCR Resident

Subdivision E—Qualified Financial Statements

8‑70 Meaning of Qualified Financial Statements

8‑75 Use of same kind of Qualified Financial Statements

Subdivision F—Special rules for particular circumstances

8‑80 Transitional CbCR Safe Harbour—special rule for Joint Ventures

8‑85 Transitional CbCR Safe Harbour—special rule for Ultimate Parent Entity that is Flow‑through Entity

8‑90 Transitional CbCR Safe Harbour—special rule for Deductible Dividend Regimes

8‑95 Transitional CbCR Safe Harbour—special rules for Investment Entities and their Constituent Entity‑owners

8‑100 Transitional CbCR Safe Harbour—special rule for Net Unrealised Fair Value Loss

8‑105 Transitional CbCR Safe Harbour—exclusions

Subdivision G—Treatment of Hybrid Arbitrage Arrangements

8‑110 Transitional CbCR Safe Harbour—Hybrid Arbitrage Arrangements

8‑115 Meaning of Hybrid Arbitrage Arrangement

8‑120 Meaning of deduction/non‑inclusion arrangement

8‑125 Meaning of duplicate loss arrangement

8‑130 Meaning of duplicate tax recognition arrangement

8‑135 Entities treated as Constituent Entities for purposes of this Subdivision

8‑140 Financial statements for purposes of this Subdivision

8‑145 Financial statements—Flow‑through Entity

8‑150 Arrangement treated as having been entered into after 15 December 2022

Division 3—Simplified Calculations Safe Harbour

Subdivision A—Simplified Calculations Safe Harbour

8‑155 Simplified Calculations Safe Harbour—general rule

Subdivision B—SC De minimis test, SC ETR test and SC Routine profits test

8‑160 Meeting the SC De minimis test

8‑165 Meeting the SC ETR test

8‑170 Meeting the SC Routine profits test

Subdivision C—NMCE simplified calculations

8‑175 NMCE simplified calculations

8‑180 NMCE simplified calculations election

8‑185 Meaning of Non‑material Constituent Entity (or NMCE)

Subdivision D—Miscellaneous

8‑190 Meaning of Total Revenue and Income Tax Accrued (Current Year) of Constituent Entity

8‑195 Meaning of Relevant CbC Regulations and Country‑by‑Country Reporting regulations

Division 4—Qualified Domestic Minimum Top‑up Tax (QDMTT) Safe Harbour

8‑200 QDMTT Safe Harbour—general rule

8‑205 Disqualification from election—disputed amounts

8‑210 Disqualification from election—switch‑off rule

8‑215 Meaning of OECD Securitisation Entity

8‑220 Meaning of Securitisation Arrangement

Division 5—Transitional UTPR Safe Harbour

8‑225 Transitional UTPR Safe Harbour

Chapter 9—Transition rules

Part 9‑1—Tax attributes upon transition

9‑5 Pre‑Transition Year deferred tax assets and liabilities

9‑10 Pre‑Transition Year deferred tax assets and liabilities—amounts

9‑15 Pre‑Transition Year intra‑MNE Group asset transfers

9‑20 Meaning of Transition Year

Part 9‑2—Transitional relief for the Substance‑based Income Exclusion

9‑25 Application of this Part

9‑30 Transitional relief for Payroll Carve‑out Amount

9‑35 Transitional relief for Tangible Asset Carve‑out Amount

Part 9‑3—Exclusion from the UTPR of MNE Groups in the initial phase of their international activity

9‑40 Total UTPR Top‑up Tax Amount reduced to zero

9‑45 If Australia is the Reference Jurisdiction, section 9‑40 does not apply etc.

9‑50 Meaning of Reference Jurisdiction

Chapter 10—Definitions

Part 10‑1—Defined terms

10‑5 Definitions

10‑10 GloBE Implementation Framework

10‑15 Qualified GloBE taxes

10‑20 Direct Ownership Interest—interest differently classified

Part 10‑2—Definitions of Securitisation Entity, Flow‑through Entity, Tax Transparent Entity, Reverse Hybrid Entity, and Hybrid Entity

10‑25 Meaning of Securitisation Entity

10‑30 Meaning of Flow‑through Entity

10‑35 Meaning of Tax Transparent Entity

10‑40 Meaning of Reverse Hybrid Entity

10‑45 Fiscal transparency and meaning of Tax Transparent Structure

10‑50 Deemed Flow‑through Entity and Tax Transparent Entity

10‑55 Meaning of Hybrid Entity

Part 10‑3—Location of dual‑located entities

10‑60 Dual‑located entities

10‑65 Dual‑located Parent Entity located in non‑IIR jurisdiction

This instrument is the Taxation (Multinational—Global and Domestic Minimum Tax) Rules 2024.

(1) Each provision of this instrument specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. The whole of this instrument | The day after this instrument is registered. | 24 December 2024 |

Note: This table relates only to the provisions of this instrument as originally made. It will not be amended to deal with any later amendments of this instrument.

(2) Any information in column 3 of the table is not part of this instrument. Information may be inserted in this column, or information in it may be edited, in any published version of this instrument.

This instrument is made under the Taxation (Multinational—Global and Domestic Minimum Tax) Act 2024.

Note: This instrument applies generally in relation to Fiscal Years starting on or after 1 January 2024: see subsection 5(1) of the Act. However, to the extent that this instrument applies to Australian UTPR Tax, it applies in relation to Fiscal Years starting on or after 1 January 2025: see subsection 5(2) of the Act.

(1) For the purposes of paragraph 20(1)(h) of the Act, the following Entities are prescribed:

(a) an Excluded Exempt Income Entity;

(b) an Excluded Non‑Profit Subsidiary.

(2) An Entity is an Excluded Exempt Income Entity if:

(a) at least 85% of the value of the Entity is owned (directly or through a chain of Excluded Entities) by one or more of the following (other than a Pension Services Entity):

(i) an Excluded Entity under paragraph 20(1)(a), (b), (c), (d), (e) or (f) of the Act;

(ii) if the Entity is an Ultimate Parent Entity—an Investment Fund or a Real Estate Investment Vehicle; and

(b) substantially all of the Entity’s income is Excluded Dividends or Excluded Equity Gain or Loss that is excluded from the computation of GloBE Income or Loss in accordance with section 3‑20 or 3‑30 of this instrument.

(3) An Entity is an Excluded Non‑Profit Subsidiary if:

(a) 100% of the value of the Entity is owned (directly or indirectly) by one or more Non‑profit Organisations; and

(b) the sum of the revenue of all Group Entities of the MNE Group of which the Entity is a Group Entity (other than such revenue as is attributable to a Group Entity of the MNE Group that is a Non‑profit Organisation, an Excluded Service Entity or an Excluded Exempt Income Entity):

(i) does not exceed the MNE Group’s GloBE Threshold for the Fiscal Year; and

(ii) is less than 25% of the total revenue of the MNE Group.

1‑25 Foreign currency translation—general

General foreign currency translation

(1) Subsection (2) applies for the purposes of computing an amount under this instrument in relation to an MNE Group for a Fiscal Year, if the amount:

(a) is denominated in a currency other than the reporting currency of the Consolidated Financial Statements of the Ultimate Parent Entity of the MNE Group (the relevant reporting currency); and

(b) is not converted to the relevant reporting currency in the course of preparing the Consolidated Financial Statements; and

(c) is not an amount to which subsection (4) applies.

(2) Convert the amount to the relevant reporting currency using the foreign currency translation principles of the Authorised Financial Accounting Standard that would have been used to convert the amount to the relevant reporting currency if that conversion were undertaken in the course of preparing the Consolidated Financial Statements for the Fiscal Year.

Foreign currency translation for materiality or other threshold

(3) Subsection (4) applies for the purposes of determining if a materiality or other threshold mentioned in subsection 12(4) or section 35 of the Act, or in this instrument, that is denominated in Euros is satisfied or exceeded by an amount in respect of a Group, Entity or jurisdiction for a particular Fiscal Year.

(4) If the amount is denominated in another currency, convert the amount from that currency to Euros using the average of the daily rates of exchange, in respect of the 2 currencies for the month of December included in the Fiscal Year immediately preceding the particular Fiscal Year, as quoted by:

(a) the European Central Bank; or

(b) if the European Central Bank does not quote a daily rate of exchange in respect of the 2 currencies—the Reserve Bank of Australia; or

(c) if both the European Central Bank and the Reserve Bank of Australia do not quote a daily rate of exchange in respect of the 2 currencies—a source specified in a determination under subsection (5).

(5) For the purposes of paragraph (4)(c), the Minister may, by legislative instrument, make a determination specifying a source quoting rates of exchange.

Part 2‑1—Application of the IIR

2‑5 Meaning of IIR Top‑up Tax Amount

Constituent Entities

(1) A Parent Entity of an Applicable MNE Group for a Fiscal Year has an IIR Top‑up Tax Amount for the Fiscal Year in respect of a Low‑Taxed Constituent Entity for the Fiscal Year of the Applicable MNE Group if:

(a) the Parent Entity is located in Australia; and

(b) the Parent Entity holds an Ownership Interest in the Low‑Taxed Constituent Entity at any time during the Fiscal Year; and

(c) the Low‑Taxed Constituent Entity is not located in Australia.

Note: A Parent Entity that is taken to be located in another jurisdiction under subsection 10‑60(2) or (3) may be treated as being located in Australia for the purposes of paragraph (a) of this subsection: see section 10‑65.

(2) The IIR Top‑up Tax Amount is equal to the Parent Entity’s Allocable Share of the Top‑up Tax of the Low‑Taxed Constituent Entity for the Fiscal Year.

Joint Ventures and JV Subsidiaries

(3) A Parent Entity of an Applicable MNE Group for a Fiscal Year has an IIR Top‑up Tax Amount for the Fiscal Year in respect of a Joint Venture of the Applicable MNE Group, or a JV Subsidiary of a Joint Venture of the Applicable MNE Group, for the Fiscal Year if:

(a) the Parent Entity is located in Australia; and

(b) the Parent Entity holds an Ownership Interest in the Joint Venture or JV Subsidiary at any time during the Fiscal Year; and

(c) the Joint Venture or JV Subsidiary is not located in Australia; and

(d) the Joint Venture or JV Subsidiary is a Low‑Taxed Constituent Entity for the Fiscal Year.

Note: For the purposes of determining whether a Joint Venture or its JV Subsidiaries are Low‑Taxed Constituent Entities, treat them as comprising a separate MNE Group, of which the Joint Venture is the Ultimate Parent Entity: see paragraph 6‑75(3)(b).

(4) The IIR Top‑up Tax Amount is equal to the Parent Entity’s Allocable Share of the Top‑up Tax of the Joint Venture or JV Subsidiary for the Fiscal Year, computed in accordance with section 6‑75.

Ordering rule

(5) Despite subsections (1) and (3), the Parent Entity mentioned in those subsections does not have an IIR Top‑up Tax Amount for the Fiscal Year in any of the following circumstances:

(a) in a case where the Parent Entity is an Intermediate Parent Entity of the Applicable MNE Group:

(i) the Ultimate Parent Entity of the Applicable MNE Group is required to apply a Qualified IIR for that Fiscal Year; or

(ii) another Intermediate Parent Entity of the Applicable MNE Group that holds (directly or indirectly) a Controlling Interest in the Intermediate Parent Entity is required to apply a Qualified IIR for that Fiscal Year;

(b) in a case where the Parent Entity is a Partially‑Owned Parent Entity of the Applicable MNE Group:

(i) the Partially‑Owned Parent Entity is wholly owned (directly or indirectly) by another Partially‑Owned Parent Entity of the Applicable MNE Group; and

(ii) the other Partially‑Owned Parent Entity is required to apply a Qualified IIR for that Fiscal Year.

Part 2‑2—Allocation of Top‑up Tax under the IIR

2‑10 Meaning of Allocable Share

A Parent Entity’s Allocable Share of the Top‑up Tax of a Low‑Taxed Constituent Entity for a Fiscal Year is an amount equal to:

(a) the Top‑up Tax of the Low‑Taxed Constituent Entity for the Fiscal Year;

multiplied by:

(b) the Parent Entity’s Inclusion Ratio for the Low‑Taxed Constituent Entity for the Fiscal Year.

Note 1: See section 2‑20 for the effect of the IIR offset mechanism on the Allocable Share.

Note 2: See section 7‑95 for the computation of a Parent Entity’s Allocable Share of the Top‑up Tax of a Constituent Entity that is an Investment Entity.

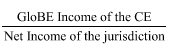

2‑15 Meaning of Inclusion Ratio

(1) The Inclusion Ratio, of a Parent Entity of an MNE Group, for a Low‑Taxed Constituent Entity for a Fiscal Year, is:

(a) the GloBE Income of the Low‑Taxed Constituent Entity for the Fiscal Year, reduced by the amount of that GloBE Income attributable to Ownership Interests held by other owners (see subsection (2));

divided by:

(b) the GloBE Income of the Low‑Taxed Constituent Entity for the Fiscal Year.

Note: See subsection (3) if the Low‑Taxed Constituent Entity is a Flow‑through Entity.

(2) For the purposes of paragraph (1)(a), the amount of GloBE Income attributable to Ownership Interests in the Low‑Taxed Constituent Entity held by other owners is the amount that would have been treated as attributable to such owners under the principles of the Acceptable Financial Accounting Standard used in the Consolidated Financial Statements of the Ultimate Parent Entity of the MNE Group on the following assumptions:

(a) the Low‑Taxed Constituent Entity’s net income were equal to its GloBE Income;

(b) the Parent Entity had prepared Consolidated Financial Statements in accordance with that Acceptable Financial Accounting Standard (the hypothetical Consolidated Financial Statements);

(c) the Parent Entity held a Controlling Interest in the Low‑Taxed Constituent Entity such that all of the income and expenses of the Low‑Taxed Constituent Entity were consolidated on a line‑by‑line basis with those of the Parent Entity in the hypothetical Consolidated Financial Statements;

(d) all of the Low‑Taxed Constituent Entity’s GloBE Income were attributable to transactions with persons that are not Group Entities of the MNE Group;

(e) all Ownership Interests not held by the Parent Entity were held by owners that are not Group Entities of the MNE Group.

(3) However, if the Low‑Taxed Constituent Entity is a Flow‑through Entity, treat references in this section to GloBE Income as not including any amount by which its Financial Accounting Net Income or Loss is reduced under paragraph 3‑255(1)(a) (amounts attributable to an owner that is not a Group Entity of the MNE Group).

(1) A Parent Entity of an MNE Group’s Allocable Share of the Top‑up Tax of a Low‑Taxed Constituent Entity is reduced if:

(a) the Parent Entity holds an Indirect Ownership Interest in the Low‑Taxed Constituent Entity through an Intermediate Parent Entity or a Partially‑Owned Parent Entity of the MNE Group; and

(b) the Intermediate Parent Entity or a Partially‑Owned Parent Entity is not eligible for an exclusion under subsection 2‑5(5), or an equivalent law of a non‑Australian jurisdiction.

(2) The amount of the reduction is the portion of the Parent Entity’s Allocable Share of the Top‑up Tax that is brought into charge by the Intermediate Parent Entity or the Partially‑Owned Parent Entity under a Qualified IIR.

Part 2‑4—Domestic Top‑up Tax Amount

2‑25 Meaning of Domestic Top‑up Tax Amount

Constituent Entities generally

(1) Subsection (2) applies if a Low‑Taxed Constituent Entity for a Fiscal Year of an Applicable MNE Group for the Fiscal Year:

(a) is located in Australia for the Fiscal Year; or

(b) is a Stateless Constituent Entity of the Applicable MNE Group that:

(i) is created in Australia; or

(ii) is a Stateless Constituent Entity under subsection 41(3) or 42(3) of the Act; or

(iii) is a Permanent Establishment in relation to which paragraph 19(1)(d) of the Act applies, and is a place of business (including a deemed place of business) in Australia.

(2) The Low‑Taxed Constituent Entity has a Domestic Top‑up Tax Amount for the Fiscal Year if it has Top‑up Tax for the Fiscal Year.

Note: If the Low‑Taxed Constituent Entity is a Securitisation Entity, its Domestic Top‑up Tax Amount for the Fiscal Year will be zero (see subsection 2‑35(3)) unless the only Constituent Entities of the MNE Group located in Australia are Securitisation Entities (see subsection 2‑35(4)).

Permanent Establishments

(3) Subsection (4) applies if:

(a) a Low‑Taxed Constituent Entity for a Fiscal Year of an Applicable MNE Group for the Fiscal Year is a Permanent Establishment of a Main Entity; and

(b) the Low‑Taxed Constituent Entity is located in Australia for the Fiscal Year; and

(c) the Main Entity is not located in Australia for the Fiscal Year.

(4) If the Low‑Taxed Constituent Entity has Top‑up Tax for the Fiscal Year:

(a) despite subsection (2), the Low‑Taxed Constituent Entity does not have a Domestic Top‑up Tax Amount for the Fiscal Year; and

(b) the Main Entity has a Domestic Top‑up Tax Amount for the Fiscal Year in respect of the Low‑Taxed Constituent Entity.

Joint Ventures and JV Subsidiaries

(5) Subsection (6) applies if:

(a) a Joint Venture of an MNE Group, or a JV Subsidiary of a Joint Venture of an MNE Group, is located in Australia for a Fiscal Year; and

(b) the MNE Group is an Applicable MNE Group for the Fiscal Year; and

(c) the Joint Venture, or the JV Subsidiary, is a Low‑Taxed Constituent Entity for the Fiscal Year.

Note: For the purposes of determining whether a Joint Venture or its JV Subsidiaries are Low‑Taxed Constituent Entities, treat them as comprising a separate MNE Group, of which the Joint Venture is the Ultimate Parent Entity: see paragraph 6‑75(3)(b).

(6) The Joint Venture, or the JV Subsidiary, has a Domestic Top‑up Tax Amount for the Fiscal Year if it has Top‑up Tax for the Fiscal Year.

(7) Subsection (8) applies if:

(a) a JV Subsidiary of a Joint Venture of an MNE Group is a Permanent Establishment of a Main Entity that is:

(i) the Joint Venture; or

(ii) another JV Subsidiary of the Joint Venture; and

(b) the JV Subsidiary is a Low‑Taxed Constituent Entity for the Fiscal Year; and

(c) the JV Subsidiary is located in Australia for the Fiscal Year; and

(d) the Main Entity is not located in Australia for the Fiscal Year.

(8) If the JV Subsidiary has Top‑up Tax for the Fiscal Year:

(a) despite subsection (6), the JV Subsidiary does not have a Domestic Top‑up Tax Amount for the Fiscal Year; and

(b) the Main Entity has a Domestic Top‑up Tax Amount for the Fiscal Year in respect of the JV Subsidiary.

2‑30 Amount of Domestic Top‑up Tax Amount

Constituent Entities generally and Permanent Establishments

(1) For the purposes of subsection 2‑25(2) or (4), the amount of the Domestic Top‑up Tax Amount is equal to the amount of the Top‑up Tax mentioned in that subsection, computed in accordance with the principles set out in section 2‑35.

Joint Ventures and JV Subsidiaries

(2) For the purposes of subsection 2‑25(6) or (8), the amount of the Domestic Top‑up Tax Amount is equal to the amount of the Top‑up Tax mentioned in that subsection, computed in accordance with the principles set out in sections 2‑35 and 6‑75.

(3) Subsection (4) applies if:

(a) any of the following circumstances exist:

(i) a Joint Venture of an MNE Group is also a Joint Venture of another MNE Group;

(ii) a JV Subsidiary of a Joint Venture of an MNE Group is also a JV Subsidiary of a Joint Venture of another MNE Group; and

(b) as a result of those circumstances, subsection 2‑25(6) or (8) applies to the Joint Venture, or the JV Subsidiary, for a Fiscal Year, in relation to each of the MNE Groups.

(4) Treat the reference in subsection (2) to “the amount of the Top‑up Tax” as instead being a reference to “half the amount of the Top‑up Tax”.

Note: This means that the Joint Venture or the JV Subsidiary (or if subsection 2‑25(8) applies, the Main Entity) has a Domestic Top‑up Tax Amount for the Fiscal Year of half the amount of the Top‑up Tax, in relation to each MNE Group.

2‑35 Computing Top‑up Tax for the purposes of section 2‑30—principles

(1) This section sets out principles for the purposes of section 2‑30.

(2) Assume that the amount of Domestic Top‑up Tax referred to in section 5‑30, for the Fiscal Year mentioned in subsection 2‑25(1) or (5), were zero.

(3) If a Constituent Entity of an MNE Group is a Securitisation Entity:

(a) treat the GloBE Income of the Constituent Entity for any Fiscal Year as being zero for the purposes of the following:

(i) the definition of Aggregate GloBE Income of all CEs in subsection 5‑40(2);

(ii) the definition of Aggregate GloBE Income of all CEs for prior year in subsection 5‑40(5) (including that definition as it applies for the purposes of subsection 5‑40(7));

(iii) the definition of GloBE Income of the CE in subsection 5‑40(2);

(iv) the definition of GloBE Income of the CE for prior year in subsection 5‑40(5) (including that definition as it applies for the purposes of subsection 5‑40(7)); and

(b) for those purposes, do not apply paragraph 5‑40(7)(b) in relation to the GloBE Income of the Constituent Entity.

(4) Subsection (3) does not apply if the only Constituent Entities of the MNE Group that are located in Australia are Securitisation Entities.

(5) If subsection (3) applies and no Constituent Entity of the MNE Group that is located in Australia and is not a Securitisation Entity has GloBE Income for the Fiscal Year:

(a) treat the GloBE Income of each such Constituent Entity as being one Euro for any Fiscal Year, for the purposes of the following:

(i) the definition of Aggregate GloBE Income of all CEs in subsection 5‑40(2);

(ii) the definition of Aggregate GloBE Income of all CEs for prior year in subsection 5‑40(5) (including that definition as it applies for the purposes of subsection 5‑40(7));

(iii) the definition of GloBE Income of the CE in subsection 5‑40(2);

(iv) the definition of GloBE Income of the CE for prior year in subsection 5‑40(5) (including that definition as it applies for the purposes of subsection 5‑40(7)); and

(b) for those purposes, do not apply paragraph 5‑40(7)(b) in relation to the GloBE Income of each such Constituent Entity.

(6) Assume that the following provisions did not apply in relation to the allocation of an amount in respect of Covered Taxes to a Constituent Entity covered by subsection (7):

(a) section 4‑45 (Allocation of amounts from Constituent Entity to Permanent Establishment);

(b) section 4‑55 (Allocation of amounts from Constituent Entity‑owner to CFC);

(c) section 4‑65 (Allocation of amounts from Constituent Entity‑owner to Hybrid Entity or Reverse Hybrid Entity);

(d) section 4‑70 (Amounts accrued in financial accounts of Constituent Entity‑owner on distribution from Constituent Entity to Constituent Entity‑owner—allocation to Constituent Entity), unless the amount in respect of Covered Taxes is an amount in respect of Australian final withholding tax.

(7) For the purposes of subsection (6), this subsection covers any of the following:

(a) a Constituent Entity that is located in Australia;

(b) a Constituent Entity that is a Stateless Constituent Entity that:

(i) is created in Australia; or

(ii) is a Stateless Constituent Entity under subsection 41(3) or 42(3) of the Act; or

(iii) is a Permanent Establishment in relation to which paragraph 19(1)(d) of the Act applies, and is a place of business (including a deemed place of business) in Australia.

(8) Assume that section 4‑75 (Allocation of amounts in respect of Passive Income) were omitted.

2‑40 Domestic Top‑up Tax Amount—special rule for consolidated groups

(1) Subsection (2) applies if a Constituent Entity of an MNE Group is a subsidiary member of a consolidated group.

(2) Despite section 2‑30, the Constituent Entity’s Domestic Top‑up Tax Amount for the Fiscal Year is taken to be reduced to zero.

(3) Subsection (4) applies if the Constituent Entity is the head company of a consolidated group.

(4) The amount of the Constituent Entity’s Domestic Top‑up Tax Amount for the Fiscal Year is taken to be increased by the amount of each reduction under subsection (2) of this section (if any) in respect of a subsidiary member of the consolidated group.

(5) This section applies in relation to a MEC group in the same way in which it applies in relation to a consolidated group.

(6) The following terms have the same meaning in this section as they do in the Income Tax Assessment Act 1997:

(a) consolidated group;

(b) head company;

(c) MEC group;

(d) subsidiary member.

Part 2‑5—UTPR Top‑up Tax Amount

2‑45 Meaning of UTPR Top‑up Tax Amount

(1) Subsection (2) applies if a Constituent Entity of an Applicable MNE Group for a Fiscal Year is located in Australia.

(2) The Constituent Entity has a UTPR Top‑up Tax Amount for the Fiscal Year if:

(a) the Total UTPR Top‑up Tax Amount for the Applicable MNE Group for the Fiscal Year is greater than zero; and

(b) an amount of the Total UTPR Top‑up Tax Amount is allocated to Australia under section 2‑60; and

(c) an amount of that allocated amount is distributed to the Constituent Entity under section 2‑70.

(3) Subsection (4) applies if:

(a) a Constituent Entity for a Fiscal Year of an Applicable MNE Group for the Fiscal Year is a Permanent Establishment of a Main Entity; and

(b) the Constituent Entity is located in Australia for the Fiscal Year; and

(c) the Main Entity is not located in Australia for the Fiscal Year.

(4) If, disregarding this subsection, the Constituent Entity has a UTPR Top‑up Tax Amount for the Fiscal Year:

(a) despite subsection (2), the Constituent Entity does not have a UTPR Top‑up Tax Amount for the Fiscal Year; and

(b) the Main Entity has a UTPR Top‑up Tax Amount for the Fiscal Year.

(5) For the purposes of subsections (2) and (4), the UTPR Top‑up Tax Amount is equal to the amount distributed to the Constituent Entity as mentioned in paragraph (2)(c).

(6) To avoid doubt, if the Constituent Entity is an Investment Entity or Insurance Investment Entity, it does not have a UTPR Top‑up Tax Amount for the Fiscal Year.

Note 1: Under the formula in subsection 2‑70(3), an amount of the Australian allocated amount will not be distributed to such a Constituent Entity (see section 2‑85).

Note 2: If the Constituent Entity is Securitisation Entity, it will not have a UTPR Top‑up Tax Amount for the Fiscal Year unless the only Constituent Entities of the MNE Group that are located in its jurisdiction are Securitisation Entities (see paragraph 2‑85(2)(c)).

2‑50 UTPR Top‑up Tax Amount—special rule for consolidated groups

(1) Subsection (2) applies if a Constituent Entity of an MNE Group:

(a) is a subsidiary member of a consolidated group; and

(b) is not any of the following:

(i) an Investment Entity;

(ii) an Insurance Investment Entity;

(iii) a Securitisation Entity for the Fiscal Year.

(2) Despite section 2‑45, the Constituent Entity’s UTPR Top‑up Tax Amount for the Fiscal Year is taken to be reduced to zero.

(3) Subsection (4) applies if the Constituent Entity is the head company of a consolidated group.

(4) The amount of the Constituent Entity’s UTPR Top‑up Tax Amount for the Fiscal Year is taken to be increased by the amount of each reduction under subsection (2) of this section (if any) in respect of a subsidiary member of the consolidated group.

(5) This section applies in relation to a MEC group in the same way in which it applies in relation to a consolidated group.

(6) The following terms have the same meaning in this section as they do in the Income Tax Assessment Act 1997:

(a) consolidated group;

(b) head company;

(c) MEC group;

(d) subsidiary member.

2‑55 Meaning of Total UTPR Top‑up Tax Amount

(1) The Total UTPR Top‑up Tax Amount for an MNE Group for a Fiscal Year is the sum of the following:

(a) the total of the Top‑up Tax for the Fiscal Year of each Low‑Taxed Constituent Entity for the Fiscal Year of the MNE Group, as adjusted in accordance with this section;

(b) if there are one or more Joint Ventures of the MNE Group—the total of the Ultimate Parent Entity’s Allocable Share of the Top‑up Tax of each Joint Venture, and of each of its JV Subsidiaries (if any), as adjusted in accordance with this section.

Note: The Total UTPR Top‑up Tax Amount for an MNE Group for a jurisdiction may be modified by Part 8‑2 (Safe harbours).

Reduction if required to apply a Qualified IIR

(2) For the purposes of paragraph (1)(a), reduce the Top‑up Tax for the Fiscal Year of a Low‑Taxed Constituent Entity to zero if:

(a) the Low‑Taxed Constituent Entity is the MNE Group’s Ultimate Parent Entity; and

(b) the Ultimate Parent Entity is required to apply a Qualified IIR for that Fiscal Year.

(3) For the purposes of paragraph (1)(a), reduce the Top‑up Tax for the Fiscal Year of a Low‑Taxed Constituent Entity to zero if:

(a) all of the Ownership Interests in the Low‑Taxed Constituent Entity held by the MNE Group’s Ultimate Parent Entity are any of the following:

(i) Direct Ownership Interests;

(ii) Indirect Ownership Interests held through one or more Parent Entities of the MNE Group; and

(b) if subparagraph (a)(i) applies (whether or not subparagraph (a)(ii) also applies)—the Ultimate Parent Entity is required to apply a Qualified IIR for that Fiscal Year; and

(c) if subparagraph (a)(ii) applies (whether or not subparagraph (a)(i) also applies)—each of the Indirect Ownership Interests mentioned in subparagraph (a)(ii) arise because of Ownership Interests in the Low‑Taxed Constituent Entity held by Parent Entities mentioned in subparagraph (a)(ii) that are required to apply a Qualified IIR for that Fiscal Year.

Reduction—amounts brought into charge under a Qualified IIR

(4) For the purposes of paragraph (1)(a), reduce the Top‑up Tax for the Fiscal Year of a Low‑Taxed Constituent Entity if:

(a) subsection (3) does not apply in relation to the Fiscal Year and the Low‑Taxed Constituent Entity; and

(b) a Parent Entity of the MNE Group holds an Ownership Interest in the Low‑Taxed Constituent Entity.

Note: The Low‑Taxed Constituent Entity may be located in Australia.

(5) The amount of the reduction is the portion of the Parent Entity’s Allocable Share of the Top‑up Tax that is brought into charge by the Parent Entity under a Qualified IIR.

Reduction—amounts brought into charge under a Qualified IIR—JV Entities

(6) For the purposes of paragraph (1)(b), reduce the Top‑up Tax for the Fiscal Year of a Joint Venture, or of a JV Subsidiary, if a Parent Entity of the MNE Group holds an Ownership Interest in the Joint Venture or JV Subsidiary.

Note: The Joint Venture or JV Subsidiary may be located in Australia.

(7) The amount of the reduction is the portion of the Parent Entity’s Allocable Share of the Top‑up Tax that is brought into charge by the Parent Entity under a Qualified IIR.

Part 2‑6—Allocation of Top‑Up Tax for the UTPR

2‑60 Allocation of Total UTPR Top‑Up Tax Amount to Australia

(1) For the purposes of this instrument, the Total UTPR Top‑up Tax Amount for an MNE Group for a Fiscal Year is allocated to Australia in accordance with this section.

(2) The amount of the Total UTPR Top‑up Tax Amount allocated to Australia is:

(a) the Total UTPR Top‑up Tax Amount;

multiplied by:

(b) the MNE Group’s UTPR percentage for the Fiscal Year for Australia.

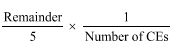

2‑65 Meaning of UTPR Percentage

(1) An MNE Group’s UTPR Percentage for a Fiscal Year for a jurisdiction that has a Qualified UTPR in force for the Fiscal Year is the percentage computed under the following formula:

where:

Number of employees in all UTPR jurisdictions means the total number of employees of all Constituent Entities of the MNE Group located in each jurisdiction that has a Qualified UTPR in force for the Fiscal Year.

Number of employees in the jurisdiction means the total number of employees of all Constituent Entities of the MNE Group located in the jurisdiction.

Total value of tangible assets in all UTPR jurisdictions means the sum of the Net Book Value of tangible assets for the Fiscal Year of all Constituent Entities of the MNE Group located in each jurisdiction that has a Qualified UTPR in force for the Fiscal Year.

Total value of tangible assets in the jurisdiction means the sum of the Net Book Value of tangible assets for the Fiscal Year of all Constituent Entities of the MNE Group located in the jurisdiction.

Note 1: Australia is a jurisdiction that has a Qualified UTPR in force for the Fiscal Year.

Note 2: For the treatment of Investment Entities, Insurance Investment Entities and Securitisation Entities, see section 2‑85.

(2) Despite subsection (1), the MNE Group’s UTPR Percentage for the Fiscal Year (the current Fiscal Year) for the jurisdiction is zero if:

(a) an amount of the Total UTPR Top‑up Tax Amount for the MNE Group for a prior Fiscal Year is allocated to the jurisdiction for the prior Fiscal Year under the provisions of a law of the jurisdiction that is equivalent to this Part; and

(b) that amount (the allocated amount) has not resulted in the Constituent Entities of the MNE Group located in the jurisdiction having an additional cash tax expense equal, in total, to the allocated amount, by:

(i) if the jurisdiction’s Qualified UTPR operates by denying deductions for Tax on income—the end of the second year after the last day on which an assessment in relation to the MNE Group for that Tax in relation to the prior Fiscal Year may be amended; or

(ii) otherwise—the end of the second year after the end of the prior Fiscal Year.

(3) If an MNE Group’s UTPR Percentage for a Fiscal Year for a jurisdiction is zero under subsection (2), disregard the jurisdiction in computing the MNE Group’s UTPR Percentage for the Fiscal Year of another jurisdiction under subsection (1).

(4) Subsection (2) does not apply if, disregarding this subsection, the MNE Group’s UTPR Percentage for the Fiscal Year for each jurisdiction that has a Qualified UTPR in force for the Fiscal Year is zero.

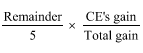

2‑70 Distribution of allocated Total UTPR Top‑Up Tax Amount to Australian Constituent Entity

(1) For the purposes of this instrument, the amount of the Total UTPR Top‑up Tax Amount for an MNE Group for a Fiscal Year that is allocated to Australia under section 2‑60 (the Australian allocated amount) is distributed, in accordance with this section, to the Constituent Entities of the MNE Group that are located in Australia.

(2) The amount of the Australian allocated amount distributed to a Constituent Entity of the MNE Group that is located in Australia is:

(a) the Australian allocated amount;

multiplied by:

(b) the percentage computed under the formula in subsection (3).

(3) The formula is as follows:

where:

Number of employees of all CEs in Australia means the total number of employees of all Constituent Entities of the MNE Group located in Australia.

Number of employees of CE in Australia means the total number of employees of the Constituent Entity located in Australia.

Total value of tangible assets of all CEs in Australia means the sum of the Net Book Value of tangible assets for the Fiscal Year of all Constituent Entities of the MNE Group located in Australia.

Total value of tangible assets of CE in Australia means the sum of the Net Book Value of tangible assets for the Fiscal Year of the Constituent Entity located in Australia.

2‑75 Number of employees in a jurisdiction

For the purposes of sections 2‑65 and 2‑70:

(a) the total number of employees is the total number of employees on a full‑time equivalent basis; and

(b) treat independent contractors participating in the ordinary operating activities of a Constituent Entity as employees of the Constituent Entity.

2‑80 Meaning of Net Book Value of Tangible Assets

(1) The Net Book Value of Tangible Assets for a Fiscal Year of a Constituent Entity of an MNE Group means the average of the beginning and end values for the Fiscal Year of the Constituent Entity’s tangible assets after taking into account accumulated depreciation, depletion, and impairment, as recorded in the financial statements of the Constituent Entity.

(2) For the purposes of subsection (1), tangible assets do not include cash or cash equivalents, intangibles, or financial assets.

(1) For the purposes of section 2‑65, disregard the employees and the Net Book Value of Tangible Assets for a Fiscal Year of any of the following:

(a) an Investment Entity;

(b) an Insurance Investment Entity.

(2) For the purposes of section 2‑70, disregard the employees and the Net Book Value of Tangible Assets for a Fiscal Year of any of the following:

(a) an Investment Entity;

(b) an Insurance Investment Entity;

(c) a Securitisation Entity for the Fiscal Year.

(3) Paragraph (2)(c) does not apply if:

(a) the Securitisation Entity is located in a jurisdiction in which no other Constituent Entities of the MNE Group are located; or

(b) the only Constituent Entities of the MNE Group that are located in that jurisdiction are Securitisation Entities.

2‑90 Employees and the Net Book Value of Tangible Assets allocated to Permanent Establishment

For the purposes of sections 2‑65 and 2‑70, if a Constituent Entity of an MNE Group is a Permanent Establishment:

(a) treat the employees of the Permanent Establishment as being the employees whose payroll costs are included in the separate financial accounts of the Permanent Establishment in accordance with Part 3‑4 (for the purposes of computing the Financial Accounting Net Income or Loss of the Permanent Establishment); and

(b) treat the employees of the Main Entity in respect of the Permanent Establishment as not including the employees mentioned in paragraph (a); and

(c) treat the tangible assets of the Permanent Establishment as being the tangible assets that are included in the separate financial accounts of the Permanent Establishment in accordance with Part 3‑4 (for the purposes of computing the Financial Accounting Net Income or Loss of the Permanent Establishment); and

(d) treat the tangible assets of the Main Entity in respect of the Permanent Establishment as not including the tangible assets mentioned in paragraph (c).

2‑95 Employees and the Net Book Value of Tangible Assets allocated from Flow‑through Entity

(1) For the purposes of sections 2‑65 and 2‑70, if a Constituent Entity of an MNE Group is a Flow‑through Entity that is a Stateless Constituent Entity:

(a) allocate, in accordance with subsection (2), the employees and the Net Book Value of Tangible Assets of the Flow‑through Entity to the Constituent Entities (if any) of the MNE Group that are located in the jurisdiction in which the Flow‑through Entity was created (each of which is a receiving Constituent Entity); and

(b) to the extent that the employees and the Net Book Value of Tangible Assets of the Flow‑through Entity are not allocated under paragraph (a)—disregard the employees and the Net Book Value of Tangible Assets.

(2) The number of employees of the Flow‑through Entity, or the Net Book Value of Tangible Assets of the Flow‑through Entity, that are allocated under paragraph (1)(a) to a receiving Constituent Entity is:

(a) the number of those employees, or that Net Book Value of Tangible Assets;

multiplied by:

(b) the percentage computed under the formula in subsection 2‑70(3) in respect of the receiving Constituent Entity.

(3) If the Flow‑through Entity is a Main Entity in respect of a Permanent Establishment, subsection (1) operates subject to section 2‑90.

Chapter 3—Computation of GloBE Income or Loss

3‑5 Meaning of GloBE Income or Loss

The GloBE Income or Loss of a Constituent Entity of an MNE Group for a Fiscal Year is the Financial Accounting Net Income or Loss for the Constituent Entity for the Fiscal Year, adjusted as provided in this instrument.

3‑10 Meaning of Financial Accounting Net Income or Loss

(1) The Financial Accounting Net Income or Loss for a Constituent Entity of an MNE Group for a Fiscal Year is the net income or loss determined for the Constituent Entity (before any consolidation adjustments eliminating intra‑group transactions) in preparing Consolidated Financial Statements of the Ultimate Parent Entity of the MNE Group for the Fiscal Year.

(2) For the purposes of subsection (1), take into account items of income and expense in the Consolidated Financial Statements only to the extent that those items:

(a) reliably and consistently reflect the affairs of the Constituent Entity; and

(b) are not reflected in the separate financial accounts of the Constituent Entity.

(3) To avoid doubt, the Financial Accounting Net Income or Loss for the Constituent Entity for the Fiscal Year includes income, expenses, gains and losses arising from transactions between the Constituent Entity and any other Constituent Entity of the MNE Group.

Note: Financial Accounting Net Income or Loss may be adjusted to exclude such income, expenses, gains and losses if an election under subsection 3‑200(1) applies.

(4) However, the Financial Accounting Net Income or Loss for the Constituent Entity for a Fiscal Year does not include any amount attributable to any purchase accounting adjustment that:

(a) is reflected in:

(i) the Consolidated Financial Statements of the Ultimate Parent Entity of the MNE Group for the Fiscal Year; or

(ii) the Constituent Entity’s financial accounts for the Fiscal Year; and

(b) arises as a result of an Entity becoming a Constituent Entity of the MNE Group as a result of the acquisition of Ownership Interests in that Entity by an existing Constituent Entity.

(5) Subsection (4) does not apply if:

(a) the acquisition occurred before 1 December 2021; and

(b) it is not reasonably practicable to determine the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year in the absence of the adjustment.

(6) Subsection (7) applies if it is not reasonably practicable to compute the Financial Accounting Net Income or Loss for a Constituent Entity of an MNE Group for a Fiscal Year based on the accounting standard (the UPE accounting standard) used in the preparation of Consolidated Financial Statements of the Ultimate Parent Entity of the MNE Group for the Fiscal Year.

(7) Compute the Financial Accounting Net Income or Loss for the Constituent Entity for the Fiscal Year using another Acceptable Financial Accounting Standard or an Authorised Financial Accounting Standard if:

(a) the financial accounts of the Constituent Entity for the Fiscal Year are maintained based on the other accounting standard; and

(b) the information contained in those financial accounts is reliable; and

(c) in the case of an Authorised Financial Accounting Standard—the financial accounts have been prepared subject to adjustments to prevent any Material Competitive Distortions; and

(d) adjustments are made to eliminate permanent differences that:

(i) arise for the Fiscal Year; and

(ii) are, in the aggregate, in excess of 1 million Euros; and

(iii) arise because of the application of a particular principle or standard under the other accounting standard (instead of the application of the UPE accounting standard) to items of income or expense or transactions; and

(e) it appears from the content of the GloBE Information Return for the MNE Group for the Fiscal Year that the Financial Accounting Net Income or Loss for the Constituent Entity for the Fiscal Year has been computed in accordance with this section.

Part 3‑2—Adjustments to determine GloBE Income or Loss

Division 1—Article 3.2.1 adjustments

3‑15 Adjustment—net taxes expense

In computing a Constituent Entity’s GloBE Income or Loss for a Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to reverse any debits or credits in the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year in respect of the following:

(a) Covered Taxes (including Covered Taxes on income that is excluded in computing the GloBE Income or Loss);

(b) to the extent it is not included in paragraph (a), a deferred tax asset attributable to a loss for the Fiscal Year;

(c) IIR;

(d) Qualified Domestic Minimum Top‑up tax;

(e) UTPR;

(f) Disqualified Refundable Imputation Tax;

(g) Tax paid or accrued by an insurance company in respect of returns to policyholders to the extent that 3‑205 applies in relation to those taxes.

3‑20 Adjustment—Excluded Dividends

(1) In computing a Constituent Entity’s GloBE Income or Loss for a Fiscal Year:

(a) adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to exclude any Excluded Dividends received or accrued by the Constituent Entity in the Fiscal Year; and

(b) if an election under subsection (2) applies to the Constituent Entity and the Fiscal Year—for the purposes of this section and the definition of Excluded Dividends in subsection 3‑25(1), treat a Portfolio Shareholding of the Constituent Entity as a Short‑term Portfolio Shareholding of the Constituent Entity.

Election

(2) A Filing Constituent Entity for an MNE Group may make an election for the MNE Group under this subsection that applies to a specified Constituent Entity of the MNE Group.

(3) An election under subsection (2) is a Five‑Year Election.

3‑25 Meaning of Excluded Dividends, Short‑term Portfolio Shareholding and Portfolio Shareholding

(1) Excluded Dividends means dividends or other distributions received or accrued in respect of an Ownership Interest, except:

(a) where the Ownership Interest is a Short‑term Portfolio Shareholding in respect of the distributions; or

(b) where the Ownership Interest is in an Investment Entity or Insurance Investment Entity, to the extent that the distributions are included under subsection 7‑150(2).

Note: If an election under subsection 3‑20(2) applies to a Constituent Entity, a Portfolio Shareholding of the Constituent Entity is treated as a Short‑term Portfolio Shareholding of the Constituent Entity for the purposes of the definition of Excluded Dividends in this subsection: see paragraph 3‑20(1)(b).

(2) However, if:

(a) dividends or other distributions are received or accrued in respect of an Ownership Interest in an Entity; and

(b) the Ownership Interest is a compound financial instrument having both equity and liability components under the Acceptable Financial Accounting Standard used in the preparation of the financial accounts of the Entity;

the dividends or other distributions are Excluded Dividends under subsection (1) only to the extent that they are received or accrued in respect of the equity component of the Ownership Interest (as determined in accordance with that Acceptable Financial Accounting Standard).

(3) If:

(a) a Constituent Entity of an MNE Group receives or accrues dividends or other distributions as a result of a Portfolio Shareholding of the Constituent Entity in an Entity; and

(b) the Portfolio Shareholding has been economically held by the Constituent Entity for less than one year at the date of the distribution;

the Portfolio Shareholding is a Short‑term Portfolio Shareholding in the Entity, of the Constituent Entity, in respect of the distributions.

(4) If the Direct Ownership Interests in an Entity held by any of the following:

(a) a Constituent Entity of an MNE Group;

(b) any other Constituent Entity of the MNE Group;

together carry rights to less than 10% of the profits, capital, reserves or voting rights of the Entity, the Direct Ownership Interests in the Entity that are held by a Constituent Entity of the MNE Group is a Portfolio Shareholding of that Constituent Entity in the Entity.

3‑30 Adjustment—Excluded Equity Gain or Loss

In computing a Constituent Entity’s GloBE Income or Loss for a Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to exclude any Excluded Equity Gain or Loss of the Constituent Entity for the Fiscal Year.

3‑35 Meaning of Excluded Equity Gain or Loss

(1) Excluded Equity Gain or Loss of a Constituent Entity of an MNE Group for a Fiscal Year means the gain, profit or loss included in the Financial Accounting Net Income or Loss of the Constituent Entity for the Fiscal Year arising from any of the following:

(a) gains and losses from changes in fair value, or from the impairment, of an Ownership Interest, except for a Portfolio Shareholding;

(b) profit or loss in respect of an Ownership Interest included under the equity method of accounting;

(c) gains and losses from disposition of an Ownership Interest, except for a disposition of an Ownership Interest that is a Portfolio Shareholding at the date of the disposition;

(d) if an election under subsection (3) applies to the Constituent Entity and the Fiscal Year—foreign exchange gains and losses, to the extent that they are covered by subsection (2).

Note: See Part 6‑3 for the treatment of gains or losses from the disposition of assets and liabilities.

(2) For the purposes of paragraph (1)(d), this subsection covers a foreign exchange gain or loss to the extent that:

(a) the foreign exchange gain or loss is attributable to hedging instruments that hedge the currency risk in Ownership Interests (other than Portfolio Shareholdings); and

(b) the gain or loss is recognised in Other Comprehensive Income at the level of the Consolidated Financial Statements of the Ultimate Parent Entity of the MNE Group; and

(c) the hedging instrument is considered an effective hedge under the Authorised Financial Accounting Standard used in the preparation of those Consolidated Financial Statements; and

(d) the economic and accounting effect of the hedging instrument:

(i) if the Constituent Entity holds the hedging instrument—has not been transferred to another Entity; or

(ii) otherwise—has been transferred to the Constituent Entity.

(3) A Filing Constituent Entity for an MNE Group may make an election for the MNE Group under this subsection that applies to a specified Constituent Entity of the MNE Group.

(4) An election under subsection (3) is a Five‑Year Election.

3‑40 Adjustment—insurance reserves

(1) Subsection (2) applies if a Constituent Entity is an insurance company.

(2) In computing the Constituent Entity’s GloBE Income or Loss for a Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to exclude any expense in respect of the movement of insurance reserves of the Constituent Entity, to the extent that the movement is economically matched by:

(a) Excluded Dividends, net of any investment management fees, from a security held on behalf of a policyholder; or

(b) Excluded Equity Gain or Loss from a security held on behalf of a policyholder.

3‑45 Adjustment—Included Revaluation Method Gain or Loss

In computing a Constituent Entity’s GloBE Income or Loss for a Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to include any Included Revaluation Method Gain or Loss of the Constituent Entity for the Fiscal Year.

3‑50 Meaning of Included Revaluation Method Gain or Loss and Other Comprehensive Income

(1) Included Revaluation Method Gain or Loss for a Fiscal Year means the net gain or loss, increased or decreased by any associated Covered Taxes, for the Fiscal Year in respect of all property, plant and equipment that arises under an accounting method or practice that:

(a) periodically adjusts the carrying value of such property to its fair value; and

(b) records the changes in value in Other Comprehensive Income; and

(c) does not subsequently report the gains or losses recorded in Other Comprehensive Income through profit and loss.

(2) Other Comprehensive Income means items of income and expense that are recognised, outside of the profit or loss account, in financial statements as required or permitted by the Authorised Financial Accounting Standard used in the Consolidated Financial Statements.

Note: Other Comprehensive Income is usually reported as an adjustment to equity in the statement of financial position (balance sheet).

3‑55 Adjustment—asymmetric foreign currency gains or losses

(1) This section applies if a Constituent Entity’s accounting functional currency for a Fiscal Year is different from its tax functional currency for the Fiscal Year.

(2) In computing the Constituent Entity’s GloBE Income or Loss for the Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to include a particular amount of taxable income or loss to the extent that:

(a) the particular amount is:

(i) attributable to fluctuations in the exchange rate between the accounting functional currency and tax functional currency; and

(ii) included in computing the Constituent Entity’s taxable income or loss; and

(iii) not included in the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year; or

(b) the particular amount is:

(i) attributable to fluctuations in the exchange rate between the tax functional currency and another currency that is not the accounting functional currency; and

(ii) not included in the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year (whether or not the particular amount is included in the Constituent Entity’s taxable income or loss).

(3) In computing the Constituent Entity’s GloBE Income or Loss for the Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to exclude a particular amount of income or loss to the extent that:

(a) the particular amount is:

(i) attributable to fluctuations in the exchange rate between the accounting functional currency and tax functional currency; and

(ii) included in the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year; and

(iii) not included in computing the Constituent Entity’s taxable income or loss; or

(b) the particular amount is:

(i) attributable to fluctuations in the exchange rate between the accounting functional currency and another currency that is not the tax functional currency; and

(ii) included in the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year; and

(iii) not included in computing the Constituent Entity’s taxable income or loss.

(4) To avoid doubt, disregard the operation of subsections (2) and (3) in determining whether the condition in subparagraph (2)(a)(iii) or (b)(ii) or (3)(a)(ii) or (b)(ii) is met.

3‑60 Meaning of tax functional currency and accounting functional currency

(1) A Constituent Entity’s tax functional currency for a Fiscal Year is the functional currency used to compute the Constituent Entity’s taxable income or loss for the Fiscal Year for a Covered Tax:

(a) unless paragraph (b) applies—in the jurisdiction in which it is located; or

(b) if the Constituent Entity is a Stateless Constituent Entity—in the jurisdiction in which it is created.

(2) A Constituent Entity’s accounting functional currency for a Fiscal Year is the functional currency used to compute the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year.

3‑65 Adjustment—policy disallowed expenses

In computing a Constituent Entity’s GloBE Income or Loss for a Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to exclude the following:

(a) expenses accrued by the Constituent Entity for illegal payments, including bribes and kickbacks;

(b) expenses accrued by the Constituent Entity for a fine or penalty that equals or exceeds 50,000 Euros (or an equivalent in the Constituent Entity’s accounting functional currency for the Fiscal Year);

(c) expenses accrued by the Constituent Entity for fines and penalties that are levied in respect of the same activity on a periodic basis (such as daily fines), the total of which equals or exceeds 50,000 Euros (or an equivalent in the Constituent Entity’s accounting functional currency for the Fiscal Year).

3‑70 Adjustment—prior period errors and changes in accounting principles

(1) Subsection (2) applies if there has been a change in the opening equity of a Constituent Entity at the start of a Fiscal Year.

(2) In computing the Constituent Entity’s GloBE Income or Loss for the Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to include the amount of that change to the extent the change is attributable to:

(a) a correction of an error in the financial accounts for a previous Fiscal Year that affected the income or expenses includible in computing the Constituent Entity’s GloBE Income or Loss for the previous Fiscal Year, except to the extent the correction resulted in a material decrease to a liability for Covered Taxes subject to Part 4‑6 (Post‑filing Adjustments and Tax Rate Changes); or

(b) a change in accounting principle or policy that affects income or expenses includible in computing the Constituent Entity’s GloBE Income or Loss for a Fiscal Year.

3‑75 Adjustment—accrued pension expense

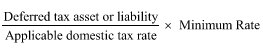

In computing a Constituent Entity’s GloBE Income or Loss for a Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to include the amount computed under the following formula:

![]()

where:

Accrued expense or income is:

(a) the amount (expressed as a negative number) that is accrued, in the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year, as pension liability expense in respect of a Pension Fund; or

(b) the amount that is accrued, in the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year, as income in respect of a Pension Fund.

Pension contributions is the amount of pension contributions made by the Constituent Entity to the Pension Fund in the Fiscal Year.

3‑80 Adjustment—qualified debt release amount

(1) Subsection (2) applies if an election under subsection (3) applies to:

(a) a Constituent Entity of an MNE Group; and

(b) a Fiscal Year.

(2) In computing the Constituent Entity’s GloBE Income or Loss for the Fiscal Year, adjust the Constituent Entity’s Financial Accounting Net Income or Loss for the Fiscal Year so as to exclude each qualified debt release amount of the Constituent Entity for the Fiscal Year.

Election

(3) A Filing Constituent Entity for an MNE Group may make an election for the MNE Group under this subsection that applies to a specified Constituent Entity of the MNE Group.

(4) An election under subsection (3) is an Annual Election.

3‑85 Meaning of qualified debt release amount

(1) The qualified debt release amount for a Fiscal Year, of a Constituent Entity that is a debtor, means an amount in respect of a debt release if:

(a) the debt release is under a statutory insolvency or bankruptcy proceeding:

(i) that is supervised by a court or other judicial body; or

(ii) under which an independent insolvency administrator is appointed; or

(b) the following conditions are met:

(i) the debt release arises under an arrangement with one or more creditors that are not connected with the debtor (each of which is a third‑party creditor);

(ii) it is reasonable to consider that, in the absence of the release of debts owed to one or more third‑party creditors under the arrangement, the debtor would be insolvent within 12 months of the date of the release;

(iii) the debtor obtains an independent expert opinion attesting that the condition in subparagraph (ii) is met; or

(c) if neither paragraph (a) nor (b) applies:

(i) the debt release arises under an arrangement with one or more creditors that are not connected with the debtor (each of which is a third‑party creditor); and

(ii) the amount is in respect of a debt owed to a third‑party creditor; and

(iii) the debtor’s liabilities exceed the fair market value of its assets, determined immediately before the debt release; and

(iv) the amount does not exceed the amount covered under subsection (2).

(2) For the purposes of subparagraph (1)(c)(iv), this subsection covers the amount that is the lesser of the following amounts:

(a) if, as a result of the debt release, the debtor’s assets are greater than or equal to its liabilities—the debtor’s liabilities less the fair market value of its assets, determined immediately before the debt release;

(b) if any amount included, as a result of the debt release, in computing net income or loss is offset by a corresponding reduction in deferred tax assets—the reduction in the debtor’s deferred tax assets resulting from the debt release.

Division 2—Other Article 3.2 adjustments

3‑90 Adjustment—stock‑based compensation expense

(1) Subsection (2) applies if:

(a) an election under subsection (5) for an MNE Group applies to: