Part 1—Preliminary

1 Name

This instrument is the Family Law (Superannuation) Regulations 2025.

2 Commencement

(1) Each provision of this instrument specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information |

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. The whole of this instrument | 1 April 2025. | 1 April 2025 |

Note: This table relates only to the provisions of this instrument as originally made. It will not be amended to deal with any later amendments of this instrument.

(2) Any information in column 3 of the table is not part of this instrument. Information may be inserted in this column, or information in it may be edited, in any published version of this instrument.

3 Authority

This instrument is made under the Family Law Act 1975.

4 Definitions

Note: Expressions used in this instrument have the same meaning as in the Act (see paragraph 13(1)(b) of the Legislation Act 2003). Some examples are the following, which are defined in Part VIIIB or VIIIC of the Act:

(a) eligible superannuation plan;

(b) member spouse;

(c) non‑member spouse;

(d) operative time;

(e) payment flag;

(f) payment split;

(g) superannuation interest.

In this instrument:

accumulation interest means a superannuation interest, or a component of a superannuation interest, that is not a defined benefit interest or a small superannuation accounts interest.

Act means the Family Law Act 1975.

adjusted base amount applicable to the non‑member spouse, for a superannuation interest at a particular date, has the meaning given by section 73.

allocated annuity means an annuity that is paid, within a range of minimum and maximum payments, from an identifiable lump sum and includes an annuity that arises under a contract that meets the standards of subregulation 1.05(4) of the SIS Regulations.

allocated pension means a pension paid, within a range of minimum and maximum payments, from an identifiable lump sum, including:

(a) a pension provided under rules of a superannuation fund that meet the standards of subregulation 1.06(4) of the SIS Regulations; and

(b) a pension provided under terms and conditions of an RSA that meet the standards of subregulation 1.07(2) of the RSA Regulations.

annuity provider means a person, body or organisation that has entered into a contract to provide an annuity.

applicable adjustment period, for a superannuation interest, has the meaning given by section 74 or 75.

base amount, for a superannuation interest, means:

(a) if the interest is identified in a superannuation agreement or flag lifting agreement:

(i) the monetary amount specified in the agreement in relation to the interest for the purposes of subparagraph 90XJ(1)(c)(i) or 90YN(1)(c)(i) of the Act, rounded up or down to the nearest dollar (with 50 cents being rounded up); or

(ii) the monetary amount calculated using a method specified in the agreement for the purposes of subparagraph 90XJ(1)(c)(ii) or 90YN(1)(c)(ii) of the Act, rounded up or down to the nearest dollar (with 50 cents being rounded up); and

(b) if a splitting order applies for the interest—the monetary amount allocated to the non‑member spouse by the court under subsection 90XT(4) or 90YY(5) of the Act, rounded up or down to the nearest dollar (with 50 cents being rounded up).

component of a superannuation interest has the meaning given by section 5.

constitutionally protected fund has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

deferred annuity means an annuity that is not presently payable.

defined benefit interest has the meaning given by section 6.

exempt public sector superannuation scheme has the same meaning as in the SIS Act.

fixed term annuity means an annuity that:

(a) is not a market linked annuity; and

(b) is paid for a fixed period.

growth phase for:

(a) a superannuation interest (other than a small superannuation accounts interest) of a member spouse; or

(b) a component of such an interest;

has the meaning given by section 7 or 8.

innovative superannuation interest means a superannuation interest, or a component of a superannuation interest, if all benefits in respect of the interest or the component of the interest are provided under:

(a) a contract that meets the standards of subregulation 1.06A(2) of the SIS Regulations; or

(b) the governing rules of an eligible superannuation plan where those rules meet the standards of subregulation 1.06A(2) of the SIS Regulations.

Judges’ Pensions Act Scheme means the scheme constituted by the Judges’ Pensions Act 1968 for the provision of retirement and other benefits to and in respect of Judges, within the meaning of that Act.

lifetime pension: a benefit in respect of a superannuation interest, or a component of a superannuation interest, of a member spouse in an eligible superannuation plan is a lifetime pension of the member spouse if the benefit is payable as a pension for the life of the member spouse.

Note: Section 15 also affects the meaning of lifetime pension.

market linked annuity means an annuity, other than an allocated annuity, that:

(a) is paid from an identifiable lump sum; and

(b) arises under a contract that meets the standards of subregulation 1.05(10) of the SIS Regulations.

market linked pension means a pension, other than an allocated pension, paid from an identifiable lump sum that meets the standards of subregulation 1.06(8) of the SIS Regulations or subregulation 1.07(3A) of the RSA Regulations.

member information statement, for a member of an eligible superannuation plan, means a statement issued periodically to the member by the trustee of the plan that sets out information about the value of the member’s superannuation interest in the plan (for example, the member’s account balance, share in the plan or withdrawal benefit) at a particular date.

member’s retirement age, for a member who has a defined benefit interest in an eligible superannuation plan, means:

(a) subject to paragraphs (b) and (c), the latest retirement age for the member specified in the governing rules of the plan; or

(b) if the latest retirement age for the member specified in the governing rules of the plan is more than 65 years, or no retirement age is specified in the governing rules of the plan—65 years; or

(c) if the Minister has, under section 52, approved a retirement age as the retirement age for members of the plan, or an identifiable class of members of the plan that includes the member—the approved age.

Note: Subsection 52(5) authorises the Minister to approve as the retirement age for members, or an identifiable class of members, who hold a defined benefit interest in an eligible superannuation plan, an age other than:

(a) the retirement age specified in the governing rules of the plan; or

(b) the age of 65 years.

net earnings, for a superannuation interest in a regulated superannuation fund, approved deposit fund or RSA to which the financial product disclosure provisions of the Corporations Regulations 2001 (being the provisions in Part 7.9 of those Regulations) apply, has the meaning given by regulation 7.9.01 of those Regulations.

partially vested accumulation interest has the meaning given by section 10.

payment phase for:

(a) a superannuation interest (other than a small superannuation accounts interest) of a member spouse; or

(b) a component of such an interest;

has the meaning given by section 9.

pension means a pension, within the meaning of section 10 of the SIS Act, payable from an eligible superannuation plan (other than an account within the meaning of the Small Superannuation Accounts Act 1995).

percentage‑only interest has the meaning given by section 11.

public sector superannuation scheme has the same meaning as in the SIS Act.

relevant condition of release has the meaning given by section 19.

relevant date, for the purposes of determining under Part 6 an amount for a superannuation interest that is subject to a payment split, means:

(a) in relation to a payment split under a superannuation agreement or flag lifting agreement:

(i) the date agreed on for that purpose by the parties to the agreement; or

(ii) if no date is agreed on by the parties to the agreement and the agreement is dated—the date shown on the agreement; or

(iii) if no date is agreed on by the parties to the agreement and the agreement is not dated—the date when a copy of the agreement is served on the trustee of the relevant eligible superannuation plan; and

(b) in relation to a payment split under a splitting order—the date determined by the court.

Note: While Part 6 does not expressly apply to payment splits under a superannuation agreement or flag lifting agreement, the parties to the agreement may nevertheless agree to use the methods in Part 6 to determine an amount for the superannuation interest. Paragraph (a) of this definition applies for that case.

RSA Regulations means the Retirement Savings Accounts Regulations 1997.

self managed superannuation fund has the same meaning as in the SIS Act.

SIS Regulations means the Superannuation Industry (Supervision) Regulations 1994.

small superannuation accounts interest means a superannuation interest in an account within the meaning of the Small Superannuation Accounts Act 1995.

superannuation annuity has the meaning given by subsection 995‑1(1) of the Income Tax Assessment Act 1997.

superannuation contributions surcharge or surcharge means the tax imposed by the Superannuation Contributions Tax Imposition Act 1997.

superannuation fund has the same meaning as in the SIS Act.

unflaggable interest has the meaning given by section 13.

unsplittable interest has the meaning given by section 14.

value of the non‑member spouse’s entitlement has the meaning given by:

(a) in Subdivision B of Division 3 of Part 3—section 25; or

(b) in Subdivision A of Division 4 of Part 3—section 29; or

(c) in Subdivision B of Division 4 of Part 3—section 32; or

(d) in Subdivision C of Division 4 of Part 3—section 35.

withdrawal benefit:

(a) for a member of a regulated superannuation fund, an exempt public sector superannuation scheme or an approved deposit fund, has the meaning given by subregulation 1.03(1) of the SIS Regulations; and

(b) for a member of an RSA, has the meaning given by subregulation 1.03(1) of the RSA Regulations; and

(c) for a member who has a small superannuation accounts interest, means the balance of the member’s account; and

(d) for a member of any other eligible superannuation plan, means the total amount of benefits that would be payable to the member if the member voluntarily ceased to be a member of the plan.

5 Meaning of component of a superannuation interest

(1) A part of a superannuation interest that a person has as a member of an eligible superannuation plan is a component of the superannuation interest if:

(a) the part has distinct features and characteristics; and

(b) the part has requirements that must be met before a benefit in respect of the part becomes payable to the member; and

(c) the part does not make up the entire superannuation interest.

(2) However, a benefit payable in respect of the superannuation interest or a component of the superannuation interest is not itself a component of the superannuation interest.

Note: A component of a superannuation interest that a member has in an eligible superannuation plan is a constituent part of the superannuation interest that gives rise, or may give rise, to an entitlement to a benefit or benefits. A benefit may:

(a) be paid in a range of different forms (for example, a lump sum or a pension); and

(b) become payable upon satisfying particular conditions of release (for example, retirement, resignation, invalidity or death).

Each benefit payable, or potentially payable, is not itself a component.

Example 1: A person has a superannuation interest as a member of an eligible superannuation plan. Under the plan, if the member permanently retires the member becomes entitled to:

(a) in all cases—benefits based on the member’s account balance at the time of retirement; and

(b) if the retirement is not due to invalidity—benefits in the form of a lump sum, or payments from a lifetime pension, calculated by reference to defined benefit factors; and

(c) if the retirement is due to invalidity—benefits in the form of payments from a lifetime pension, calculated by reference to defined benefit factors.

The part of the member’s superannuation interest that gives rise to their entitlement to the benefits mentioned in paragraph (a) is one component of the interest. The part of the member’s superannuation interest that gives rise to their entitlement to the benefits mentioned in paragraph (b) or (c) is another component of the interest. The benefits are not themselves components.

Example 2: A person who has a superannuation interest as a member of an eligible superannuation plan has retired permanently. As a result, the member is entitled to:

(a) benefits paid in the form of a pension drawn from the member’s account balance and commencing at the time of retirement; and

(b) benefits payable in the form of a lifetime pension only if and when the member reaches 80 years of age.

The part of the member’s superannuation interest that gives rise to their entitlement to the benefits mentioned in paragraph (a) is one component of the interest. The part of the member’s superannuation interest that may give rise to their entitlement to the benefits mentioned in paragraph (b) is another component of the interest. The benefits are not themselves components.

(3) Subsections (1) and (2) apply despite any other law.

6 Meaning of defined benefit interest

(1) A defined benefit interest is:

(a) a superannuation interest that:

(i) a member spouse has in an eligible superannuation plan; and

(ii) is an interest in respect of the whole of which the member spouse is entitled, when benefits in respect of the interest become payable, to be paid a benefit that is, or may be, defined by reference to one or more of the amounts or factors mentioned in subsection (3); or

(b) a component of a superannuation interest that:

(i) a member spouse has in an eligible superannuation plan; and

(ii) is a component in respect of which the member spouse is entitled, when benefits in respect of the interest become payable, to be paid a benefit that is, or may be, defined by reference to one or more of the amounts or factors mentioned in subsection (3); or

(c) a superannuation interest that:

(i) a member spouse has in the scheme provided for by the Australian Defence Force Cover Act 2015; and

(ii) is in the payment phase; or

(d) a superannuation interest that:

(i) a member spouse has in the scheme provided for by Division 3 of Part 1 of Chapter 4 of the Federal Circuit and Family Court of Australia Act 2021; and

(ii) is in the payment phase.

(2) However, a superannuation interest, or a component of a superannuation interest, is not a defined benefit interest because of paragraph (1)(a) or (b) if:

(a) the only benefits payable in respect of the interest or component that are defined by reference to one or more of the amounts or factors mentioned in subsection (3) are benefits payable on death or invalidity; and

(b) there are no other circumstances in which benefits payable in respect of the interest or component are, or could have been, defined by reference to the amounts or factors mentioned in subsection (3).

Note 1: This subsection has the effect that paragraphs (1)(a) and (b) do not apply to a superannuation interest or component if defined benefit factors:

(a) are only used to calculate death or invalidity benefits in respect of the interest or component; and

(b) would not be used to calculate benefits in respect of the interest or component that would become payable in other circumstances, such as on age retirement or the termination of employment.

Note 2: However, this subsection does not prevent a superannuation interest or component mentioned in paragraph (1)(c) or (d) being a defined benefit interest for the purposes of this instrument (even if paragraph (1)(a) or (b) could also apply to the superannuation interest or component).

Example 1: Benefits in respect of a superannuation interest of a member spouse are payable on retirement based on the balance of the member’s account. However, on death or invalidity the benefit is to be defined by reference to amounts or factors mentioned in subsection (3). The member retires on invalidity and the benefits that become payable to the member are then defined by reference to those amounts or factors. The superannuation interest is not a defined benefit interest because defined benefit factors only applied, and could only have applied, in the circumstance of the death or invalidity of the member spouse.

Example 2: Benefits in respect of a component of a superannuation interest of a member spouse are payable in a range of circumstances, including death, invalidity or retirement, and are to be defined by reference to amounts or factors mentioned in subsection (3). The component is a defined benefit interest because death or invalidity are not the only circumstances in which defined benefit factors are, or could be, applied to calculate the benefits in respect of the interest.

(3) For the purposes of subsections (1) and (2), the amounts and factors are as follows:

(a) the amount of:

(i) the member spouse’s salary at the date of the termination of the member spouse’s employment, the date of the member spouse’s retirement, or another date; or

(ii) the member spouse’s salary averaged over a period;

(b) the amount of salary, or allowance in the nature of salary, payable to another person (for example, a judicial officer, a member of the Commonwealth or a State Parliament, or a member of the Legislative Assembly of a Territory);

(c) a specified amount;

(d) specified conversion factors.

7 Meaning of growth phase—superannuation interests in regulated superannuation funds, approved deposit funds and RSAs

(1) This section applies to a superannuation interest of a member spouse in any of the following eligible superannuation plans:

(a) a regulated superannuation fund;

(b) an approved deposit fund;

(c) an RSA.

(2) The superannuation interest, or a component of the interest, is in the growth phase at a particular date if, at that date, the member spouse satisfies the requirements of subsection (3), (4) or (5).

(3) A member spouse satisfies the requirements of this subsection at a particular date if, at that date, the member spouse has not satisfied a relevant condition of release for the superannuation interest or the component of the interest.

Note: For the meaning of satisfies a relevant condition of release, see subsection (6).

(4) A member spouse satisfies the requirements of this subsection at a particular date if, at that date:

(a) the member spouse has satisfied a relevant condition of release for the superannuation interest or the component of the interest; but

(b) no benefit has been paid in respect of the superannuation interest or the component of the interest, and no action has been taken by or for the member spouse under the governing rules of the plan to cash any benefit that the member spouse is entitled to be paid as a result of satisfying the condition of release.

Note: For the meaning of satisfies a relevant condition of release, see subsection (6).

(5) A member spouse satisfies the requirements of this subsection at a particular date if, at that date:

(a) the member spouse has satisfied a relevant condition of release for the superannuation interest or the component of the interest; and

(b) a benefit (other than a benefit that is paid as a pension) has been paid in respect of the superannuation interest or the component of the interest to or for the benefit of:

(i) the member spouse; or

(ii) if the member spouse has died—the member spouse’s legal personal representative;

but no action has been taken by or for the member spouse, or that representative, under the governing rules of the plan to receive any other benefit that the member spouse, or the member spouse’s estate, is entitled to be paid as a result of satisfying the condition of release.

Meaning of satisfies a relevant condition of release

(6) For the purposes of this section, a member spouse satisfies a relevant condition of release at a date for a superannuation interest, or a component of a superannuation interest, if at that date:

(a) if the superannuation interest is in a regulated superannuation fund—a condition of release mentioned in item 101, 102, 102A, 103, 106 or 108 of Schedule 1 to the SIS Regulations is satisfied; or

(b) if the superannuation interest is in an approved deposit fund—a condition of release mentioned in item 201, 202, 202A, 203 or 206 of Schedule 1 to the SIS Regulations is satisfied; or

(c) if the superannuation interest is in an RSA—a condition of release mentioned in item 101, 102, 102A, 103, 106 or 107 of Schedule 2 to the RSA Regulations is satisfied.

8 Meaning of growth phase—superannuation interests in other eligible superannuation plans

(1) This section applies to a superannuation interest of a member spouse in any of the following eligible superannuation plans:

(a) a superannuation annuity;

(b) a superannuation fund other than a regulated superannuation fund.

(2) The superannuation interest, or a component of the interest, is in the growth phase at a particular date if, at that date:

(a) a releasing event has not occurred for the member spouse for the superannuation interest or the component of the interest; or

(b) a releasing event has occurred for the member spouse for the superannuation interest or the component of the interest, but no action has been taken by or for the member spouse under the governing rules of the plan to receive any benefit that the member spouse is entitled to be paid as a result of the occurrence of the releasing event; or

(c) a releasing event has occurred for the member spouse for the superannuation interest or the component of the interest, and a benefit (other than a benefit that is paid as a pension) has been paid to or for the benefit of:

(i) the member spouse; or

(ii) if the member spouse has died—the member spouse’s legal personal representative;

but no action has been taken by or for the member spouse, or that legal personal representative, under the governing rules of the plan to receive any other benefit that the member spouse, or the member spouse’s estate, is entitled to be paid as a result of the occurrence of the releasing event.

Meaning of releasing event

(3) For the purposes of this section, a releasing event has occurred for a member spouse at a particular date for a superannuation interest, or a component of a superannuation interest, if at that date:

(a) the member spouse has retired; or

(b) the member spouse has died; or

(c) the member spouse has a terminal medical condition (as defined in regulation 6.01A of the SIS Regulations); or

(d) as a result of the member spouse’s ill health (whether physical or mental), the member spouse:

(i) has ceased to be gainfully employed (including if the member spouse has ceased temporarily to receive any gain or reward under a continuing arrangement for the member spouse to be gainfully employed); and

(ii) is unlikely, because of the ill health, ever again to engage in gainful employment for which the member spouse is reasonably qualified by education, training or experience; or

(e) the member spouse has turned 65 years; or

(f) in the case of a member spouse for whom:

(i) the member spouse’s employer; or

(ii) one or more associates (within the meaning of section 12 of the SIS Act) of the member spouse’s employer;

has contributed to the member spouse’s eligible superannuation plan in relation to the superannuation interest—the member spouse has ceased the member spouse’s employment with that employer.

9 Meaning of payment phase

Either:

(a) a superannuation interest (other than a small superannuation accounts interest) of a member spouse in an eligible superannuation plan; or

(b) a component of such a superannuation interest;

is in the payment phase at a particular date if it is not in the growth phase at that date.

10 Meaning of partially vested accumulation interest

(1) An accumulation interest that a member spouse has as a member of an eligible superannuation plan is a partially vested accumulation interest if subsection (2) or (3) applies in relation to the interest.

(2) This subsection applies in relation to the superannuation interest if the withdrawal benefit in relation to the member spouse on a particular day is less than the total amount notionally or actually allocated to the member spouse on that day, except if the withdrawal benefit is less than that notional or actual amount because of any of the following reasons:

(a) the trustee of the plan has been assessed to be liable to pay superannuation contributions surcharge in respect of the member spouse, and the trustee has not debited the amount notionally or actually allocated to the member spouse in respect of that liability;

(b) insurance costs have been charged against the member spouse’s benefits in the plan;

(c) any other fees, taxes or charges will be charged against the member spouse’s benefits when the member spouse ceases to be a member of the plan.

(3) This subsection applies in relation to the superannuation interest if the benefits to which the member spouse is or may be entitled, on voluntarily ceasing to be a member of the eligible superannuation plan, may include an additional benefit that is calculated by reference to the amount that has been credited, under the governing rules of the plan, to the member spouse in respect of contributions that have been made by, or in respect of, the member spouse.

11 Meaning of percentage‑only interest

(1) For the purposes of the definitions of percentage‑only interest in sections 90XD and 90YD of the Act, each of the following superannuation interests is prescribed:

(a) a superannuation interest in the scheme constituted by the Judges’ Pensions Act 1953 (NSW);

(b) a superannuation interest in the scheme constituted by the Judges (Pensions and Long Leave) Act 1957 (Qld);

(c) a superannuation interest in the scheme constituted by the Governors (Salary and Pensions) Act 2003 (Qld);

(d) a superannuation interest in the scheme constituted by the Judges’ Contributory Pensions Act 1968 (Tas);

(e) a superannuation interest in a superannuation annuity.

(2) However, the superannuation interest is not prescribed as a percentage‑only interest if it is covered by an item of the following table and immediately before the relevant day mentioned in that item:

(a) either:

(i) the interest is covered by a superannuation agreement or a flag lifting agreement that is in force and provides for a payment split; or

(ii) the interest is an interest to which subsection 90XJ(5) or 90YN(5) of the Act applies; or

(b) the interest is covered by a splitting order; or

(c) the non‑member spouse has served a waiver notice on the trustee under section 90XZA or 90YZQ of the Act in respect of the interest.

When the superannuation interest is not a percentage‑only interest |

Item | If the superannuation interest is covered by: | the relevant day is: |

1 | paragraph (1)(b) of this section | 3 September 2003 |

2 | paragraph (1)(d) of this section | 2 May 2003 |

(3) Subsection (2) applies only in relation to the agreement, order or notice.

(4) A reference in subsection (1) to an Act of a State or Territory is a reference to that Act as in force on 1 April 2025.

12 Meaning of trustee

(1) For the purposes of paragraph (b) of the definitions of trustee in sections 90XD and 90YD of the Act, each of the persons mentioned in an item of the following table is identified as a trustee of the eligible superannuation plan mentioned in that item.

Persons identified as a trustee of an eligible superannuation plan |

Item | Each of these persons is identified as a trustee: | of this plan: |

1 | (a) the General Manager of Fair Work Australia, for a member of the Scheme who is: (i) the President (or a former President) of Fair Work Australia; or (ii) a Deputy President (or a former Deputy President) of Fair Work Australia who was a Presidential Member of the Australian Industrial Relations Commission; or (iii) a former Presidential Member of the Australian Industrial Relations Commission; or (iv) a spouse of a person mentioned in subparagraph (i), (ii), or (iii); (b) for any other member of the Scheme—the Secretary of the Department of Finance | the Judges’ Pensions Act Scheme. |

2 | the Parliamentary Retiring Allowances Trust established under the Parliamentary Contributory Superannuation Act 1948 | the scheme constituted by the Parliamentary Contributory Superannuation Act 1948. |

3 | an RSA provider (within the meaning of the Retirement Savings Accounts Act 1997) that has accepted contributions to an RSA | that RSA. |

4 | the Commissioner of Taxation | an account (within the meaning of the Small Superannuation Accounts Act 1995). |

5 | an annuity provider that has entered into a contract with a person to provide a superannuation annuity to that person | that superannuation annuity. |

6 | CSC (within the meaning of the Governance of Australian Government Superannuation Schemes Act 2011) | the scheme constituted by the Defence Force (Superannuation) (Productivity Benefit) Determination 1988 made under subsection 52(1) of the Defence Act 1903. |

7 | the Secretary of the Department of Finance | (a) the scheme constituted by the Governor‑General Act 1974; or (b) the scheme provided for by Division 3 of Part 1 of Chapter 4 of the Federal Circuit and Family Court of Australia Act 2021. |

(2) In this section:

Department of Finance means the Department administered by the Minister administering the Public Governance, Performance and Accountability Act 2013.

Presidential Member means the President, a Vice President, a Senior Deputy President or a Deputy President of the Australian Industrial Relations Commission.

13 Meaning of unflaggable interest

For the purposes of the definitions of unflaggable interest in sections 90XD and 90YD of the Act, a superannuation interest of a member spouse that is in the payment phase is prescribed.

14 Meaning of unsplittable interest

(1) For the purposes of the definitions of unsplittable interest in sections 90XD and 90YD of the Act, a superannuation interest of a member spouse is prescribed if the superannuation interest:

(a) is covered by subsection (2) or (3) of this section; and

(b) is none of the following:

(i) a superannuation interest in the scheme provided under the Judges’ Pensions Act 1971 (SA) as in force on 1 April 2025;

(ii) a superannuation interest in the scheme constituted by the Parliamentary Contributory Superannuation Act 1948.

Note: Prescribing these superannuation interests makes them unsplittable interests. An unsplittable interest cannot be the subject of a payment split under a superannuation agreement, flag lifting agreement or splitting order (see Part VIIIB or VIIIC of the Act).

(2) This subsection covers a superannuation interest of a member spouse that is an interest in respect of which:

(a) the whole or remaining part of the benefits are being paid to the member spouse as:

(i) a lifetime pension or fixed‑term pension that the member is no longer entitled to commute; or

(ii) a lifetime annuity or fixed term annuity; and

(b) the amount of the annual benefit payable to the member is less than $4,000.

(3) This subsection covers a superannuation interest of a member spouse that:

(a) is not an interest to which paragraph (2)(a) applies; and

(b) is an interest with a withdrawal benefit in relation to the member spouse of less than $10,000.

(4) To avoid doubt, a superannuation interest not covered by this section is not an unsplittable interest only because payments in respect of the interest are not splittable payments.

15 Meaning of lifetime pension etc.

To avoid doubt, a benefit in respect of a superannuation interest, or a component of a superannuation interest, of a member spouse in an eligible superannuation plan that is paid as a pension is not prevented from being a lifetime pension of the member spouse, or a pension payable for the life of a member spouse, merely because:

(a) the benefit is paid upon the retirement of the member spouse (including retirement on the basis of invalidity); and

(b) under the governing rules of the plan, the payments may be varied (including by being reduced to nil), suspended or cancelled.

Part 2—Payments that are not splittable payments: payments of a particular character, or payments after death of member spouse

16 Payments of a particular character that are not splittable payments

(1) Each of the payments mentioned in subsection (2) in respect of a superannuation interest of the member spouse:

(a) is prescribed for the purposes of subsection 90XE(2) and 90YG(2) of the Act; and

(b) as a result, is not a splittable payment for the purposes of all payment splits in respect of the superannuation interest.

Note: The payment will not be a splittable payment generally, rather than only not being a splittable payment for a particular payment split (see subsection 90XE(2) or 90YG(2) of the Act).

(2) The payments are as follows:

(a) a payment of benefits to the member spouse that is made following a determination, under subregulation 6.19A(1) of the SIS Regulations or subregulation 4.22A(1) of the RSA Regulations, that a condition of release of the benefits on a compassionate ground has been satisfied;

(b) a payment to the member spouse that is made because the member spouse is taken to be in severe financial hardship;

(c) a pension payment to the member spouse that is paid on the basis of temporary incapacity (within the meaning of regulation 6.01 of the SIS Regulations), other than a payment that is:

(i) one of a series of payments of that kind that have been paid to the member spouse for a period of at least 2 years and is made more than 2 years after the first such payment of that series; or

(ii) a payment to which paragraph (g) of this subsection applies; or

(iii) a payment from a lifetime pension;

(d) if the superannuation interest is in a superannuation fund that is not a regulated superannuation fund—a payment to the member spouse that is made on compassionate grounds as provided by the governing rules of the plan;

(e) if the superannuation interest is in a superannuation annuity that is a deferred annuity—a payment to the member spouse that is made on compassionate grounds under a term of the annuity;

(f) if the superannuation interest is in the superannuation scheme constituted by the Superannuation Act 1976 or the Superannuation Act 1990—a payment to the member spouse that is made:

(i) during any period in which the member spouse’s health is being assessed for the purpose of determining the member spouse’s eligibility for payment on the ground that the member spouse is totally and permanently incapacitated; or

(ii) because the member spouse’s salary or other remuneration, or hours of employment, have been reduced because of ill health;

(g) if the superannuation interest is in the superannuation scheme continued in existence by the Superannuation (State Public Sector) Act 1990 (Qld)—a pension payment to the member spouse that is:

(i) an income protection benefit paid under section 50 of the Participation Schedule; or

(ii) an incapacity benefit to which the member spouse is entitled under paragraph 136(b) of the Participation Schedule; or

(iii) an incapacity pension to which the member spouse is entitled under paragraph 199(b) of the Participation Schedule;

Note: In 2025, the scheme continued in existence by the Superannuation (State Public Sector) Act 1990 (Qld) was known as the Australian Retirement Trust.

(h) if the superannuation interest is in an account (within the meaning of the Small Superannuation Accounts Act 1995)—a payment to the member spouse from the account, if:

(i) in accordance with a superannuation agreement, flag lifting agreement or splitting order that has been served on the trustee of the account, the trustee has opened a separate account under the Small Superannuation Accounts Act 1995 for the non‑member spouse, and has transferred an amount from the member spouse’s account to that separate account; and

(ii) but for the operation of this paragraph, the non‑member spouse would have been entitled to be paid an amount in respect of the payment.

(3) In this section:

Government Division Rules means the Division Rules:

(a) within the meaning of the trust deed, as existing on 1 April 2025, that governs the scheme continued in existence under section 5 of the Superannuation (State Public Sector) Act 1990 (Qld); and

(b) as in force on 1 April 2025;

that relate to the Government Division referred to in clause 2.1 of that deed.

Participation Schedule means the part of the Government Division Rules known as the Participation Schedule.

severe financial hardship has the meaning given by subregulation 6.01(5) of the SIS Regulations.

17 Payments after death of member spouse that are not splittable payments

(1) Each of the payments mentioned in subsection (2) made after the death of a member spouse in respect of a superannuation interest of the member spouse:

(a) is prescribed for the purposes of subsection 90XE(2) and 90YG(2) of the Act; and

(b) as a result, is not a splittable payment for the purposes of all payment splits in respect of the superannuation interest.

Note: The payment will not be a splittable payment generally, rather than only not being a splittable payment for a particular payment split (see subsection 90XE(2) or 90YG(2) of the Act).

(2) The payments are as follows:

(a) a payment to a reversionary beneficiary who is a child in relation to the member spouse if, at the date of the payment, the child has not turned 18;

(b) a payment to a reversionary beneficiary who is a child in relation to the member spouse if:

(i) immediately before the death of the member spouse, the child was dependent on the member spouse; and

(ii) at the date of the payment, the child has turned 18; and

(iii) the payment is made to enable the child to complete the child’s education or, if the child has special needs because of a physical or intellectual disability, to provide maintenance and meet expenses in respect of those needs;

(c) a payment to a reversionary beneficiary for the benefit of a child in relation to the member spouse, if the requirements of paragraph (a) or (b) are satisfied in relation to the child and the payment.

(3) In this section:

child, in relation to a member spouse who has a superannuation interest in an eligible superannuation plan, means:

(a) a child of the member spouse, within the meaning of section 60F of the Act; or

(b) a child of the member spouse under the governing rules of the plan; or

(c) a child who has been determined by the trustee of the plan, under the governing rules of the plan, to be a child of the member spouse; or

(d) a child for whom the member spouse had, at the time of the member spouse’s death, responsibility for the day‑to‑day care, welfare and development under:

(i) an order under Part VII of the Act; or

(ii) an order under Part 5 of the Family Court Act 1997 (WA) as in force on 1 April 2025; or

(iii) an order under a corresponding law of a foreign country.

Part 3—Payments that are not splittable payments: payments made in particular circumstances

Division 1—Preliminary

18 Simplified outline of this Part

Division 2 provides that a payment in respect of a superannuation interest of a member spouse is not a splittable payment for the purposes of applying Part VIIIB or VIIIC of the Act to a superannuation agreement, flag lifting agreement or splitting order if:

(a) where the interest is not a percentage‑only interest—the requirements of a Subdivision of Division 3 are met; or

(b) where the interest is a percentage‑only interest—the requirements of a Subdivision of Division 4 are met; or

(c) the requirements of Division 5 are met for a payment by the member spouse in satisfaction of the non‑member spouse’s entitlement under the agreement or order.

19 Meaning of relevant condition of release

(1) A relevant condition of release, for a superannuation interest, is:

(a) if the superannuation interest is in a regulated superannuation fund or an exempt public sector superannuation scheme—a condition of release mentioned in item 101, 102, 102A, 103 or 106 of Schedule 1 to the SIS Regulations; and

(b) if the superannuation interest is in an approved deposit fund—a condition of release mentioned in item 201, 202, 202A, 203 or 206 of Schedule 1 to the SIS Regulations; and

(c) if the superannuation interest is in an RSA—a condition of release mentioned in item 101, 102, 102A, 103 or 106 of Schedule 2 to the RSA Regulations; and

(d) if the superannuation interest is in a superannuation annuity—a condition of release mentioned in item 201, 202, 202A, 203 or 206 of Schedule 1 to the SIS Regulations.

(2) For the purposes of this instrument, a non‑member spouse is taken to satisfy a relevant condition of release if the event specified in the condition has occurred in relation to the non‑member spouse.

(3) For the purposes of this instrument, when applying item 101, 103, 201 or 203 of Schedule 1 to the SIS Regulations to a non‑member spouse, a reference in:

(a) the definition of permanent incapacity in regulation 1.03C of the SIS Regulations; and

(b) subregulation 6.01(7) of the SIS Regulations;

to a member is taken to be a reference to the non‑member spouse.

(4) For the purposes of this instrument, when applying item 101 or 103 of Schedule 2 to the RSA Regulations to a non‑member spouse, a reference in:

(a) the definition of permanent incapacity in subregulation 4.01(2) of the RSA Regulations; and

(b) subregulation 4.01(4) of the RSA Regulations;

to an RSA holder is taken to be a reference to the non‑member spouse.

Division 2—Circumstances when payments are not splittable payments

20 Circumstances when payments are not splittable payments

(1) Subsection (2) applies to a payment in respect of a superannuation interest of a member spouse if:

(a) a superannuation agreement, flag lifting agreement or splitting order applies to the superannuation interest; and

(b) the payment is made after the requirements of:

(i) a Subdivision of Division 3 or 4; or

(ii) Division 5;

are met for the non‑member spouse’s entitlement under that agreement or order in respect of the interest.

(2) For the purposes of subsection 90XE(2) or 90YG(2) of the Act, the payment is prescribed for the purposes of applying Part VIIIB or VIIIC of the Act to that agreement or order.

Note: This means the payment is not a splittable payment for those purposes.

Division 3—When the payment relates to a superannuation interest that is not a percentage‑only interest

Subdivision A—New interest created, or amount transferred or rolled over or paid, under SIS Regulations or RSA Regulations, in satisfaction of the non‑member spouse’s entitlement

21 Requirements of this Subdivision

(1) The requirements of this Subdivision are met for a non‑member spouse’s entitlement under a particular superannuation agreement, flag lifting agreement or splitting order in respect of a superannuation interest if:

(a) the interest is not a percentage‑only interest; and

(b) subsection (2) or (3) applies for the interest.

(2) This subsection applies for the superannuation interest if the trustee of the relevant eligible superannuation plan has, under the payment split provisions of the SIS Regulations, done any of the following things:

(a) created a new interest in the plan for the non‑member spouse;

(b) transferred or rolled over an amount equal to the value of the benefit that the non‑member spouse would be required to have if a new interest had been created for the non‑member spouse under the payment split provisions of the SIS Regulations;

(c) paid to the non‑member spouse the amount that the non‑member spouse is entitled in respect of the superannuation interest at the time of the payment.

(3) This subsection applies for the superannuation interest if the trustee of the relevant eligible superannuation plan has, under the payment split provisions of the RSA Regulations, done any of the following things:

(a) opened a new RSA for the non‑member spouse;

(b) transferred or rolled over an amount equal to the value that the non‑member spouse would be required to have if a new RSA had been opened for the non‑member spouse under the payment split provisions of the RSA Regulations;

(c) paid to the non‑member spouse an amount that is at least the amount to which the non‑member spouse is entitled in respect of the superannuation interest at the time of the payment.

(4) In this section:

payment split provisions of the RSA Regulations means the provisions of the RSA Regulations (other than Division 4A.4) dealing with superannuation interests that are subject to a payment split.

payment split provisions of the SIS Regulations means the provisions of the SIS Regulations (other than Division 7A.3) dealing with superannuation interests that are subject to a payment split.

Subdivision B—New interest otherwise created, or amount otherwise transferred or rolled over or paid, by trustee, or separate entitlement arising, in satisfaction of non‑member spouse’s entitlement under agreement or order

22 Requirements of this Subdivision

(1) The requirements of this Subdivision are met for a non‑member spouse’s entitlement under a particular superannuation agreement, flag lifting agreement or splitting order in respect of a superannuation interest if:

(a) the interest:

(i) is not a percentage‑only interest; and

(ii) is in a superannuation fund or an approved deposit fund; and

(b) either of the following sections applies for the interest:

(i) section 23 (main circumstances);

(ii) section 24 (public sector superannuation schemes in which a separate entitlement arises for the non‑member spouse).

Note: Section 23 will apply if any of its subsections applies for the interest.

(2) However, for the purposes of subparagraph (1)(b)(i), section 23 will not apply for the superannuation interest if:

(a) the interest is a defined benefit interest; and

(b) the governing rules of the relevant eligible superannuation plan provide for the reduction of the benefit payable to any other member of the plan (other than the member spouse or a reversionary beneficiary of the member spouse) as a result of:

(i) the creation of a new interest for the non‑member spouse; or

(ii) the transfer or rollover of an amount to be held for the benefit of the non‑member spouse; or

(iii) the payment of an amount to the non‑member spouse.

23 Main circumstances when this Subdivision applies

Not a defined benefit interest in a SMSF—trustee creates new interest, or transfers or rolls over an amount, with a value at least as much as the non‑member spouse’s entitlement

(1) This section applies for the superannuation interest if:

(a) the interest is not a defined benefit interest in a self managed superannuation fund; and

(b) the trustee of the relevant eligible superannuation plan has, in respect of the non‑member spouse’s entitlement under the agreement or order and under the governing rules of the plan, done either of the following things:

(i) created a new interest in the plan for the non‑member spouse with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time the new interest is created;

(ii) transferred or rolled over to another superannuation fund or an RSA an amount, to be held for the benefit of the non‑member spouse, with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time the amount is transferred or rolled over.

Defined benefit interest in a SMSF—trustee transfers or rolls over an amount, with a value at least as much as the non‑member spouse’s entitlement

(2) This section applies for the superannuation interest if:

(a) the interest is a defined benefit interest in a self managed superannuation fund; and

(b) the trustee of the relevant eligible superannuation plan has, in respect of the non‑member spouse’s entitlement under the agreement or order and under the governing rules of the plan, transferred or rolled over to another superannuation fund or an RSA an amount:

(i) to be held for the benefit of the non‑member spouse; and

(ii) with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time the amount is transferred or rolled over.

Non‑member spouse satisfies relevant condition of release and trustee pays that spouse an amount equal to the non‑member spouse’s entitlement

(3) This section applies for the superannuation interest if:

(a) the interest is in a regulated superannuation fund, an exempt public sector superannuation scheme or an approved deposit fund; and

(b) the non‑member spouse has satisfied a relevant condition of release in relation to the interest; and

(c) the trustee of the relevant eligible superannuation plan has, in respect of the non‑member spouse’s entitlement under the agreement or order, paid to the non‑member spouse an amount equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time of the payment.

Member spouse being paid a pension and trustee pays the non‑member spouse an amount equal to the non‑member spouse’s entitlement

(4) This section applies for the superannuation interest if:

(a) the interest is in a regulated superannuation fund, an exempt public sector superannuation scheme or an approved deposit fund; and

(b) at the operative time in relation to the agreement or order, the member spouse was being paid a pension in respect of the interest; and

(c) the trustee of the relevant eligible superannuation plan has, in respect of the non‑member spouse’s entitlement under the agreement or order, paid to the non‑member spouse an amount equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time of the payment.

Trustee pays the non‑member spouse an amount equal to the non‑member spouse’s entitlement

(5) This section applies for the superannuation interest if:

(a) the interest is in a superannuation fund that is neither a regulated superannuation fund nor an exempt public sector superannuation scheme; and

(b) the trustee of the relevant eligible superannuation plan has, in respect of the non‑member spouse’s entitlement under the agreement or order, paid to the non‑member spouse an amount equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time of the payment.

Trustee need not have done anything mentioned in this section

(6) To avoid doubt, nothing in a subsection of this section requires the trustee of the relevant eligible superannuation plan to do something mentioned in that subsection.

24 Other circumstance—public sector superannuation schemes in which a separate entitlement arises for the non‑member spouse

This section applies for the superannuation interest if:

(a) the interest is in a public sector superannuation scheme (the original scheme); and

(b) at or after the operative time in relation to the agreement or order, and under the governing rules of the original scheme or under the governing rules of another public sector superannuation scheme, a separate entitlement to benefits has arisen for the non‑member spouse:

(i) in respect of the non‑member spouse’s entitlement under the agreement or order; and

(ii) with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time the separate entitlement arose; and

(c) where the interest is a defined benefit interest—the governing rules of the original scheme do not provide for the reduction of the benefit payable to any other member of the scheme (other than the member spouse or a reversionary beneficiary of the member spouse) as a result of the non‑member spouse’s separate entitlement.

25 Meaning of value of the non‑member spouse’s entitlement

(1) In this Subdivision, the value of the non‑member spouse’s entitlement for the superannuation interest at the time (the termination time) when the trustee carries out an action described in section 23, or when a separate entitlement arises for the non‑member spouse as described in section 24, is:

(a) if a base amount applies in relation to the interest—the value calculated under subsection (2) or (3) of this section; or

(b) if, under subparagraph 90XJ(1)(c)(iii) or 90YN(1)(c)(iii), or paragraph 90XT(1)(b) or 90YY(1)(b), of the Act, a specified percentage is to apply to all splittable payments in respect of the interest—the value calculated under subsection (4) of this section.

Value—if a base amount applies in relation to the interest

(2) For the purposes of paragraph (1)(a), if:

(a) the termination time occurs before the first payment, that apart from this section would be a splittable payment, becomes payable in respect of the superannuation interest; or

(b) one or more payments, that apart from this section would be splittable payments, become payable in respect of the superannuation interest after the termination time, and the amount of the first such payment exceeds:

(i) if there is an adjusted base amount applicable to the non‑member spouse at the termination time—the sum of the adjusted base amount and the amount of any fees payable by the non‑member spouse under section 98; or

(ii) otherwise—the sum of the base amount applicable to the non‑member spouse at the termination time and the amount of any fees payable by the non‑member spouse under section 98;

the value of the non‑member spouse’s entitlement for the interest at the termination time is, as the case requires:

(c) the base amount specified by, or calculated in accordance with a method specified by, the relevant agreement or order; or

(d) the base amount allocated to the non‑member spouse under subsection 90XT(4) or 90YY(5) of the Act; or

(e) the adjusted base amount applicable to the non‑member spouse at the termination time.

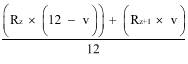

(3) For the purposes of paragraph (1)(a), if neither paragraph (2)(a) nor (b) applies for the superannuation interest, the value of the non‑member spouse’s entitlement for the interest at the termination time is:

where:

proportion of splittable payments means the proportion of each second and subsequent splittable payment that the non‑member spouse would be entitled to be paid under Part 7.

value means:

(a) for a superannuation interest in a self managed superannuation fund—the value of the interest at the termination time, determined by the method the court would consider appropriate if it were determining the value of the interest under paragraph 90XT(2)(b) or 90YY(2)(b) of the Act; or

(b) otherwise—the value of the superannuation interest, being the amount in relation to the interest at the termination time, calculated under Division 2 of Part 6 of this instrument as if references in that Division to “the relevant date” were references to “the termination time”.

fees means the amount of any fees payable by the non‑member spouse under section 98.

Value—specified percentage is to apply to all splittable payments in respect of the interest

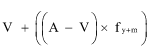

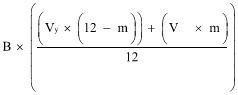

(4) For the purposes of paragraph (1)(b), the value of the non‑member spouse’s entitlement for the interest at the termination time is equal to:

where:

default amount means:

(a) if the entitlement is in respect of an interest that is neither:

(i) an accumulation interest (other than a partially vested accumulation interest); nor

(ii) an interest in a self managed superannuation fund;

the amount in relation to the interest at the termination time that a court would determine under Part 6; or

(b) if the entitlement is in respect of an accumulation interest other than:

(i) a partially vested accumulation interest; or

(ii) an interest in a self managed superannuation fund;

the amount in relation to the interest at the termination time that a court would determine under Part 6 if item 3 of the table in section 51, and subsection 53(2), applied for the interest; or

(c) if the entitlement is in respect of an interest in a self managed superannuation fund—the value of the interest at the termination time, determined by the method that the court would consider appropriate if it were determining the value of the interest under paragraph 90XT(2)(b) or 90YY(2)(b) of the Act.

Division 4—When the payment relates to a superannuation interest that is a percentage‑only interest

Subdivision A—New interest created, or amount transferred or rolled over or paid, by trustee, or separate entitlement arising, in satisfaction of non‑member spouse’s entitlement under agreement or order

26 Requirements of this Subdivision

(1) The requirements of this Subdivision are met for a non‑member spouse’s entitlement under a particular superannuation agreement, flag lifting agreement or splitting order in respect of a superannuation interest if:

(a) the interest:

(i) is a percentage‑only interest; and

(ii) is in a superannuation fund or an approved deposit fund; and

(b) either of the following sections applies for the interest:

(i) section 27 (main circumstances);

(ii) section 28 (public sector superannuation schemes in which a separate entitlement arises for the non‑member spouse).

Note: Section 27 will apply if any of its subsections applies for the interest.

(2) However, for the purposes of subparagraph (1)(b)(i), section 27 will not apply for the superannuation interest if:

(a) the interest is a defined benefit interest; and

(b) the governing rules of the relevant eligible superannuation plan provide for the reduction of the benefit payable to any other member of the plan (other than the member spouse or a reversionary beneficiary of the member spouse) as a result of:

(i) the creation of a new interest for the non‑member spouse; or

(ii) the transfer or rollover of an amount to be held for the benefit of the non‑member spouse; or

(iii) the payment of an amount to the non‑member spouse.

27 Main circumstances when this Subdivision applies

Trustee creates new interest, or transfers or rolls over an amount, with a value at least as much as the non‑member spouse’s entitlement

(1) This section applies for the superannuation interest if:

(a) the trustee of the relevant eligible superannuation plan has, in respect of the non‑member spouse’s entitlement under the agreement or order and under the governing rules of the plan, done either of the following things:

(i) created a new interest in the plan for the non‑member spouse with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time the new interest is created;

(ii) transferred or rolled over to another superannuation fund or an RSA an amount, to be held for the benefit of the non‑member spouse, with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time the amount is transferred or rolled over; and

(b) the interest was in the payment phase at the time the thing was done.

Non‑member spouse satisfies relevant condition of release and trustee pays that spouse an amount at least equal to the non‑member spouse’s entitlement

(2) This section applies for the superannuation interest if:

(a) the interest is in a regulated superannuation fund, an exempt public sector superannuation scheme or an approved deposit fund; and

(b) the non‑member spouse has satisfied a relevant condition of release in relation to the interest; and

(c) the trustee of the relevant eligible superannuation plan has, in respect of the non‑member spouse’s entitlement under the agreement or order, paid to the non‑member spouse an amount with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time of the payment; and

(d) the interest was in the payment phase at the time of the payment.

Member spouse being paid a pension and trustee pays the non‑member spouse an amount at least equal to the non‑member spouse’s entitlement

(3) This section applies for the superannuation interest if:

(a) the interest is in a regulated superannuation fund, an exempt public sector superannuation scheme or an approved deposit fund; and

(b) at the operative time in relation to the agreement or order, the member spouse was being paid a pension in respect of the interest; and

(c) the trustee of the relevant eligible superannuation plan has, in respect of the non‑member spouse’s entitlement under the agreement or order, paid to the non‑member spouse an amount with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time of the payment.

Trustee pays the non‑member spouse an amount equal to the non‑member spouse’s entitlement

(4) This section applies for the superannuation interest if:

(a) the interest is in a superannuation fund that is neither a regulated superannuation fund nor an exempt public sector superannuation scheme; and

(b) the trustee of the relevant eligible superannuation plan has, in respect of the non‑member spouse’s entitlement under the agreement or order, paid to the non‑member spouse an amount with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time of the payment; and

(c) the interest was in the payment phase at the time of the payment.

Trustee need not have done anything mentioned in this section

(5) To avoid doubt, nothing in a subsection of this section requires the trustee of the relevant eligible superannuation plan to do something mentioned in that subsection.

28 Other circumstance—public sector superannuation schemes in which a separate entitlement arises for the non‑member spouse

This section applies for the superannuation interest if:

(a) the interest is in a public sector superannuation scheme (the original scheme); and

(b) at or after the operative time in relation to the agreement or order, and under the governing rules of the original scheme or under the governing rules of another public sector superannuation scheme, a separate entitlement to benefits has arisen for the non‑member spouse:

(i) in respect of the non‑member spouse’s entitlement under the agreement or order; and

(ii) with a value of at least the value of the non‑member spouse’s entitlement for the superannuation interest at the time the separate entitlement arose; and

(c) the interest was in the payment phase at the time the separate entitlement arose; and

(d) where the interest is a defined benefit interest—the governing rules of the original scheme do not provide for the reduction of the benefit payable to any other member of the scheme (other than the member spouse or a reversionary beneficiary of the member spouse) as a result of the non‑member spouse’s separate entitlement.

29 Meaning of value of the non‑member spouse’s entitlement

(1) In this Subdivision, the value of the non‑member spouse’s entitlement for the superannuation interest at a particular time is:

(a) the value at that time calculated in accordance with Part 2 of Schedule 2, if:

(i) the superannuation agreement or flag lifting agreement identified the percentage that was to apply for the purposes of subparagraph 90XJ(1)(b)(i) or 90YN(1)(b)(i) of the Act; and

(ii) the splitting order was made under paragraph 90XT(1)(c) or 90YY(1)(c) of the Act; or

(b) the value at that time calculated in accordance with Part 3 of Schedule 2, if:

(i) the superannuation agreement or flag lifting agreement identified a percentage that was to apply for the purposes of subparagraph 90XJ(1)(b)(ii) or 90YN(1)(b)(ii) of the Act; and

(ii) the splitting order was made under paragraph 90XT(1)(b) or 90YY(1)(b) of the Act.

Subdivision B—New deferred annuity established, or amount transferred or rolled over or paid, by trustee of deferred annuity in satisfaction of non‑member spouse’s entitlement under agreement or order

30 Requirements of this Subdivision

The requirements of this Subdivision are met for a non‑member spouse’s entitlement under a particular superannuation agreement, flag lifting agreement or splitting order in respect of a superannuation interest if:

(a) the interest:

(i) is a percentage‑only interest; and

(ii) is in a superannuation annuity that is a deferred annuity; and

(b) section 31 applies for the interest.

Note: To see if section 31 applies, see subsection 31(1), (2), (3) or (5).

31 Circumstances when this Subdivision applies

Non‑member spouse satisfies relevant condition of release and trustee pays that spouse an amount equal to that spouse’s entitlement

(1) This section applies for the superannuation interest if:

(a) the non‑member spouse has satisfied a relevant condition of release in relation to the interest; and

(b) the trustee of the superannuation annuity has, in respect of the non‑member spouse’s entitlement under the agreement or order, paid to the non‑member spouse an amount equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time of the payment; and

(c) the interest is in the growth phase at the time of the payment.

Trustee transfers or rolls over an amount with a value equal to the non‑member spouse’s entitlement

(2) This section applies for the superannuation interest if:

(a) the trustee of the superannuation annuity has, in respect of the non‑member spouse’s entitlement under the agreement or order, transferred or rolled over to a superannuation fund or an RSA an amount:

(i) to be held for the benefit of the non‑member spouse; and

(ii) with a value equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time the amount is transferred or rolled over; and

(b) the interest is in the growth phase at the time the amount is transferred or rolled over.

Trustee establishes new deferred annuity with a value equal to the non‑member spouse’s entitlement

(3) This section applies for the superannuation interest if:

(a) the trustee of the superannuation annuity has, in respect of the non‑member spouse’s entitlement under the agreement or order, established a new deferred annuity that:

(i) provides for the payment of benefits to the non‑member spouse; and

(ii) commences no earlier than the time when, if the new deferred annuity were taken to be an approved deposit fund for the purposes of Part 6 of the SIS Regulations, that Part would permit or require the payment of benefits from the approved deposit fund; and

(iii) has a value equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time the new deferred annuity is established; and

(b) the interest is in the growth phase at the time the new deferred annuity is established.

(4) For the purposes of (but without limiting) subsection (3):

(a) the trustee of the superannuation annuity is taken to have established a new deferred annuity for the benefit of the non‑member spouse if the trustee has entered into an agreement with the non‑member spouse to provide such an annuity for the non‑member spouse’s benefit; and

(b) the new deferred annuity is taken to have been established on the date that agreement is entered into.

Trustee establishes new annuity, that is a non‑commutable income stream, with a value equal to the non‑member spouse’s entitlement

(5) This section applies for the superannuation interest if:

(a) the trustee of the superannuation annuity has, in respect of the non‑member spouse’s entitlement under the agreement or order, established a new annuity for the benefit of the non‑member spouse that:

(i) is a non‑commutable income stream (within the meaning of the SIS Regulations); and

(ii) has a value equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time the new annuity is established; and

(b) the interest is in the growth phase at the time the new annuity is established.

(6) For the purposes of (but without limiting) subsection (5):

(a) the trustee of the superannuation annuity is taken to have established a new annuity (being an annuity that is a non‑commutable income stream) for the benefit of the non‑member spouse if:

(i) the trustee has entered into an agreement with the non‑member spouse to provide such an annuity for the non‑member spouse’s benefit; or

(ii) the trustee has paid to another annuity provider an amount equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time the payment is made, for the purpose of that annuity provider providing such an annuity for the non‑member spouse’s benefit; and

(b) the new annuity is taken to have been established:

(i) if subparagraph (a)(i) applies—on the date the agreement between the trustee and the non‑member spouse is entered into; or

(ii) if subparagraph (a)(ii) applies—on the date the amount mentioned in that subparagraph is paid to the annuity provider by the trustee.

Trustee need not have done anything mentioned in this section

(7) To avoid doubt, nothing in a subsection of this section requires the trustee of a superannuation annuity to do something mentioned in that subsection.

32 Meaning of value of the non‑member spouse’s entitlement

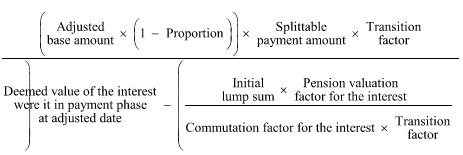

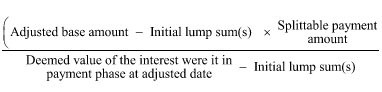

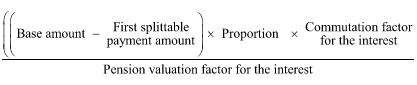

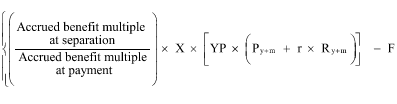

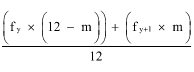

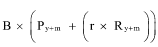

In this Subdivision, the value of the non‑member spouse’s entitlement for the superannuation interest at the time (the termination time) when the trustee carries out an action described in subsection 31(1), (2), (3) or (5) is equal to:

Subdivision C—New annuity established or amount transferred or rolled over or paid by trustee of a superannuation annuity (other than under Subdivision B) in satisfaction of non‑member spouse’s entitlement under agreement or order

33 Requirements of this Subdivision

The requirements of this Subdivision are met for a non‑member spouse’s entitlement under a particular superannuation agreement, flag lifting agreement or splitting order in respect of a superannuation interest if:

(a) the interest is a percentage‑only interest and the interest is in a superannuation annuity that is one of the following:

(i) an allocated annuity;

(ii) a market linked annuity;

(iii) a fixed term annuity;

(iv) a lifetime annuity, including a lifetime annuity that is payable for the lives of more than one person; and

(b) section 34 applies for the interest.

Note: To see if section 34 applies, see subsection 34(1), (2) or (3).

34 Circumstances when this Subdivision applies

Trustee pays non‑member spouse an amount equal to the value of the non‑member spouse’s entitlement

(1) This section applies for the superannuation interest if:

(a) the trustee of the superannuation annuity has, in respect of the non‑member spouse’s entitlement under the agreement or order, paid to the non‑member spouse an amount equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time of the payment; and

(b) the interest:

(i) was in the payment phase at the operative time in relation to the agreement or order; and

(ii) is in the payment phase at the time of the payment.

Trustee transfers or rolls over an amount with a value equal to the non‑member spouse’s entitlement

(2) This section applies for the superannuation interest if:

(a) the trustee of the superannuation annuity has, in respect of the non‑member spouse’s entitlement under the agreement or order, transferred or rolled over to a superannuation fund or an RSA an amount to be held for the benefit of the non‑member spouse; and

(b) the value of that amount is equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time that amount is transferred or rolled over; and

(c) the interest is in the payment phase at the time that amount is transferred or rolled over.

Trustee establishes new annuity with a value equal to the non‑member spouse’s entitlement

(3) This section applies for the superannuation interest if:

(a) the trustee of the superannuation annuity has, in respect of the non‑member spouse’s entitlement under the agreement or order, established any of the following new annuities (an eligible annuity) for the benefit of the non‑member spouse:

(i) an allocated annuity;

(ii) a market linked annuity;

(iii) a fixed term annuity;

(iv) a lifetime annuity; and

(b) the new annuity has a value equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time the new annuity is established; and

(c) the interest is in the payment phase at the time the new annuity is established.

(4) For the purposes of (but without limiting) subsection (3):

(a) the trustee of the superannuation annuity is taken to have established an eligible annuity for the benefit of the non‑member spouse if either of the following things have occurred:

(i) the trustee has entered into an agreement with the non‑member spouse to provide an eligible annuity for the benefit of the non‑member spouse;

(ii) the trustee has paid to another annuity provider an amount equal to the value of the non‑member spouse’s entitlement for the superannuation interest at the time the payment is made, for the purpose of that annuity provider providing an eligible annuity for the benefit of the non‑member spouse; and

(b) the eligible annuity is taken to have been established:

(i) if subparagraph (a)(i) applies—on the date the agreement between the trustee and the non‑member spouse is entered into; or

(ii) if subparagraph (a)(ii) applies—on the date the amount mentioned in subparagraph (a)(ii) is paid to the annuity provider by the trustee.

Trustee need not have done anything mentioned in this section

(5) To avoid doubt, nothing in a subsection of this section requires the trustee of a superannuation annuity to do something mentioned in that subsection.

35 Meaning of value of the non‑member spouse’s entitlement

(1) In this Subdivision, the value of the non‑member spouse’s entitlement for a superannuation interest at the time (the termination time) when the trustee carries out an action described in subsections 34(1), (2) or (3) is as described in subsection (2), (3) or (4) of this section.

Superannuation interest is in an allocated annuity or market linked annuity

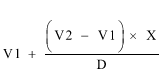

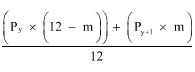

(2) If the superannuation interest is in a superannuation annuity that is an allocated annuity or a market linked annuity, the value of the non‑member spouse’s entitlement for the interest at the termination time is equal to:

Superannuation interest is in a fixed term annuity or a lifetime annuity, and the Minister has not approved a method or factors for the interest

(3) If:

(a) the superannuation interest is in a superannuation annuity that is a fixed term annuity or a lifetime annuity; and

(b) the non‑member spouse’s entitlement arises under a superannuation agreement, a flag lifting agreement or a splitting order; and

(c) the Minister has not approved, under section 70, a method or factors for determining the gross value of the superannuation interest;

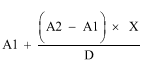

the value of the non‑member spouse’s entitlement for the interest at the termination time is equal to:

where:

applicable Schedule means:

(a) for a fixed term annuity—Schedule 9; or

(b) for a lifetime annuity—Schedule 6.

Superannuation interest is in a fixed term annuity or a lifetime annuity, and the Minister has approved a method or factors for the interest

(4) If:

(a) the superannuation interest is in a superannuation annuity that is a fixed term annuity or a lifetime annuity; and

(b) the non‑member spouse’s entitlement arises under a superannuation agreement, a flag lifting agreement or a splitting order; and

(c) the Minister has approved, under section 70, a method or factors for determining the gross value of the superannuation interest;

the value of the non‑member spouse’s entitlement for the interest at the termination time is equal to:

Division 5—When the payment by the member spouse is in satisfaction of the non‑member spouse’s entitlement under agreement or order

36 Requirements of this Division